/Phone%20and%20computer%20internet%20network%20by%20Pinkypills%20via%20iStock.jpg)

Palo Alto Networks (PANW) stock has been on a tear. Based on its strong free cash flow and FCF margins, as well as analysts' forecasts, PANW stock could be worth 21% more at over $403 per share. This article will show how this works.

PANW closed up over 9.1% at $332.00 on Monday, June 29. The stock has been on an upward trajectory since its June 2 earnings release for the fiscal Q3 ended April 30, after a brief initial drop.

What PANW Could Be Worth

Based on my new assessment of Palo Alto Networks' fair market value (FMV) it could be worth between $303 billion and $354 billion. This is between 12.1% and 30.7% higher. That sets its price target 21% higher on average, despite its recent up, or $403 per share.

I discussed its valuation in a recent Barchart article on June 8, “Palo Alto Networks Delivers Strong FCF Margins - Is PANW Worth $350?”

My latest FMV analysis builds on that article.

For example, analysts now project revenue for the next FY ending June 30, 2027, will be $13.78 billion. Applying a 38.5% FCF margin, slightly higher than my prior estimate, but equal to its latest fiscal Q3 trailing 12 months (TTM) adjusted FCF margin:

$13.78 billion x 0.385 adj. FCF margin = $5.305 billion FCF

Moreover, using a 1.75% FCF yield metric, Palo Alto Networks would have a fair market value (FMV) of $303 billion:

$5.305b / 0.0175 = $303 billion FMV

And, using a lower 1.50% FCF yield metric, it's worth more:

$5.305b / 0.015 = $353.7 billion FMV

In other words, based on today's market cap of $270.6 billion, PANW's price target (PT) is worth between 12% and 31% more, or:

$332.00 x 1.12 = $371.84 per share PT

$332.00 x 1.307 = $433.92 per share PT

The average price target is therefore 21.4% higher, or $402.88 per share. That rounds out to $403 per share.

However, there's no guarantee that PANW will rise to this PT. It could take some time. As a result, it might make sense to set a lower buy-in point and get paid for it. That can be done by selling short out-of-the-money PANW put options.

Shorting Out-of-the-Money PANW Puts

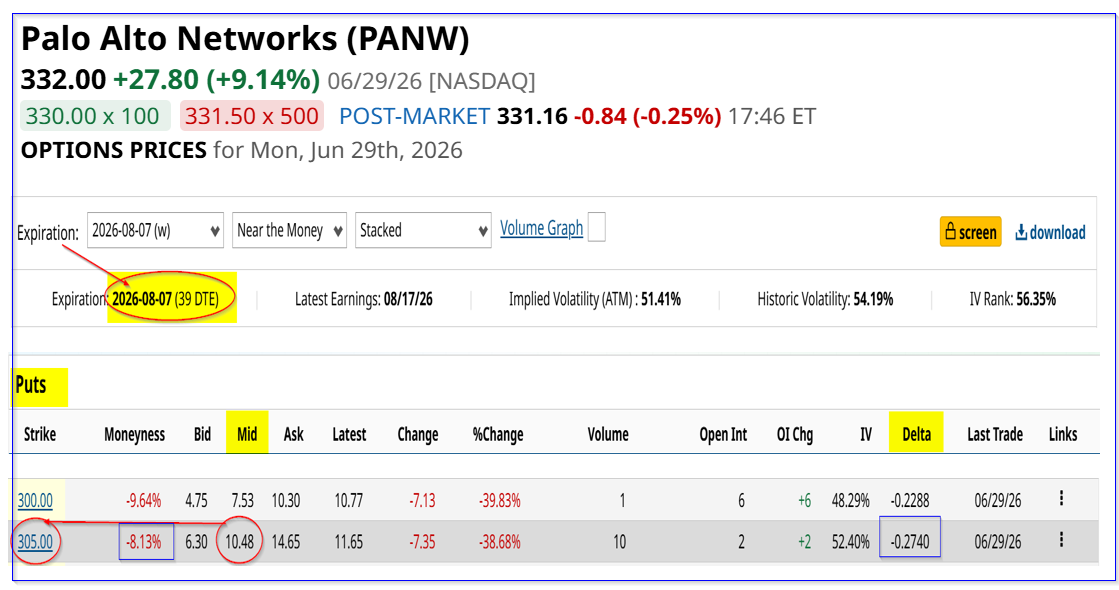

For example, the August 7, 2026, expiry put option chain shows that the $305.00 strike price put option has a high midpoint premium of $10.48.

That means that a short-seller of this put contract can make an immediate yield of 3.436% over the next 39 days (i.e., $10.48/$305.00 = 0.03436 = 3.436%).

Here is how this works. First, the investor posts $30,500 with the brokerage firm where their account is located. That acts as collateral to buy 100 shares at $305.00, if PANW falls over 8% from $332 to $305 on or before Aug. 7.

Then, the investor can enter a trading order to “Sell to Open” 1 put contract at $305.00. The investor's account will then immediately receive $1,048 (i.e., $10.48 x 100 shs per put contract).

So, the $1,048 received lowers the initial cost to just $29,452. That works out to a net put contract cost of $294.52, or 11.3% lower. That lowers the overall potential buy-in cost for investors.

Moreover, investors can take comfort in the delta ratio, which is low at just -0.274. That implies there is just over a 27% chance that PANW will drop 8% to $305 by Aug. 7.

The bottom line is that this is an attractive way for PANW value investors to get paid while also setting a lower potential buy-in point.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/A%20game%20controller%20in%20front%20of%20a%20Roblox%20computer%20screen%20by%20Miguel%20Lagoa%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)