T-Mobile US (TMUS) is a wireless communications powerhouse that has spent the past decade relentlessly dismantling the wireless status quo — and winning. Operating under the T-Mobile, Metro by T-Mobile, and Mint Mobile brands, the company serves approximately 86 million postpaid and 26 million prepaid phone customers, commanding roughly 30% of the U.S. retail wireless market following its landmark 2020 merger with Sprint and 2025 acquisition of UScellular.

Under CEO Srini Gopalan, T-Mobile is accelerating far beyond wireless, expanding aggressively into fiber through joint venture acquisitions of GoNetspeed and Greenlight Networks as well as i3 Broadband.

T-Mobile Stock Shows Weakness

T-Mobile has fallen approximately 25% over the past 12 months as well as 14% year-to-date (YTD), a divergence that highlights a stock recovering from a brutal peak-to-trough drawdown triggered by UScellular integration costs and broader telecom sector headwinds. TMUS stock's 52-week range spans from a recent low of $169.14 to a high of $261.56, with shares currently trading approximately 33% below the 52-week peak.

Against the S&P 500 Communication Services Index's ($SRTS) modest gains in 2026, TMUS has underperformed the broader telecom sector, although the company's raised full-year guidance and accelerating broadband strategy signal a meaningful recovery in the making.

T-Mobile Surpasses Estimates

T-Mobile delivered first-quarter 2026 results on April 28. Total revenue of $23.1 billion was up about 11% year-over-year (YOY), with core service revenue growing 11% to $18.8 billion, significantly outpacing competitors. Adjusted EPS of $2.27 surpassed the $2.03 consensus estimate by approximately 12%, marking the strongest earnings performance in recent quarters and extending T-Mobile's streak of consecutive EPS beats.

The company added 217,000 postpaid net accounts, up 6% YOY, and more than 500,000 total broadband net subscribers, with 5G home internet net adds accelerating YOY. More than 60% of new account lines took premium-tier rate plans.

Core adjusted EBITDA rose 12% YOY, underscoring disciplined operational efficiency despite elevated integration costs from the UScellular acquisition, while average revenue per account rose almost 4%, signaling T-Mobile is deepening customer relationships and driving higher CLVs rather than simply adding lines. Net income declined 15% YOY to $2.5 billion, primarily driven by $476 million in UScellular-related accelerated depreciation, a non-recurring charge that obscures the company's underlying earnings power.

Following the Q1 beat, management raised full-year 2026 guidance across multiple metrics, lifting postpaid net account additions guidance to 950,000 to 1.05 million, core adjusted EBITDA to a range of $37.1 billion to $37.5 billion, and adjusted free cash flow to $18.1 billion to $18.7 billion.

Will T-Mobile Be Acquired by SpaceX?

TD Cowen analyst Gregory Williams recently raised the prospect of SpaceX (SPCX) potentially acquiring T-Mobile as part of an ambitious strategy to transform Starlink into a fully integrated global connectivity platform. Williams identified T-Mobile as the clear acquisition target, citing its operational momentum, “maverick culture,” pure-play wireless positioning, and existing Starlink partnership as ideal attributes for a combined entity.

While Starlink is already exploring wholesale network agreements with AT&T (T), Verizon (VZ), and T-Mobile to pool spectrum and develop direct-to-device satellite technology, Williams noted that SpaceX may prefer outright ownership economics over a leasing arrangement. Intriguingly, the analyst also suggested that SpaceX acquisition speculation may itself be driving T-Mobile's parent, Deutsche Telekom (DTEGY), to pursue full ownership of its highly profitable U.S. subsidiary, adding a compelling M&A premium layer to the TMUS stock investment thesis.

Should You Bet on TMUS Stock?

With the SpaceX acquisition thesis adding a compelling M&A premium to T-Mobile's already strong fundamental story, and Deutsche Telekom potentially accelerating its own buyout plans in response, TMUS stock carries a rare combination of organic growth, broadband expansion, and takeover optionality.

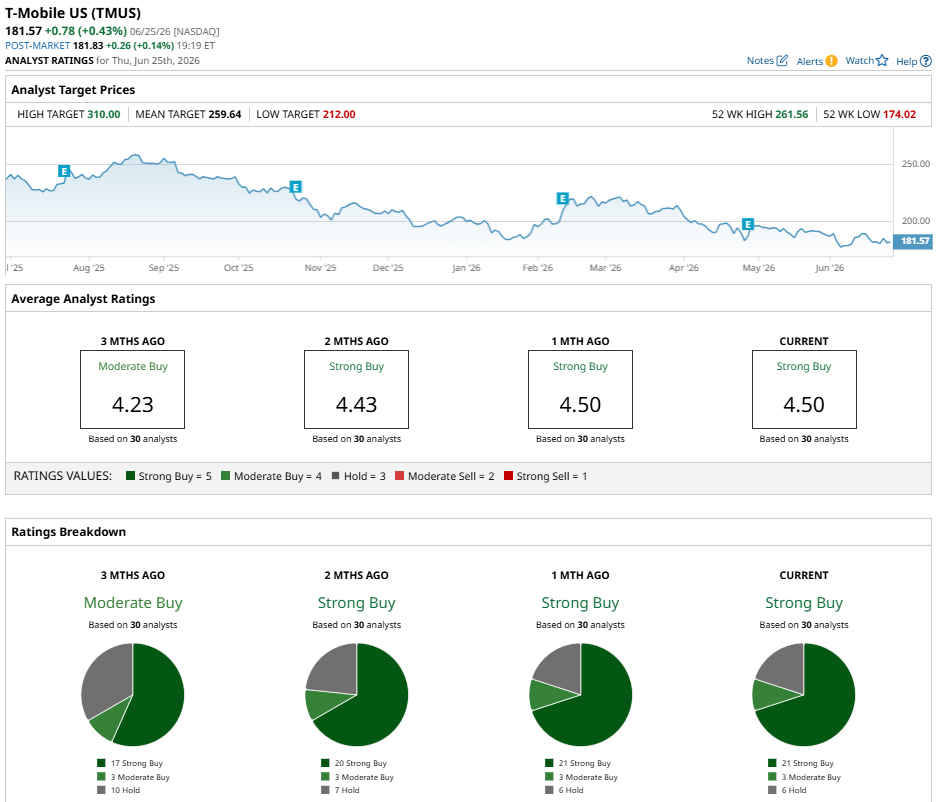

Wall Street is firmly bullish, as TMUS stock carries a consensus “Strong Buy” rating across 30 analysts with coverage. That breaks down to 21 "Strong Buy" ratings, three “Moderate Buy” ratings, and six "Hold" ratings. The mean price target of $257.45 implies approximately 47% potential upside from current levels.

For investors seeking a high-quality telecom compounder trading at a significant discount to fair value, TMUS presents one of the most compelling risk-reward setups in the communication services sector today.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)