Michael Saylor’s Strategy (MSTR) has never been a simple Bitcoin (BTCUSD) proxy. Over the years, the company has turned itself into something closer to a Bitcoin-powered financing machine, constantly rolling out new securities designed to raise fresh capital while giving investors different ways to bet on its long-term crypto strategy. One of its newest offerings, the Variable Rate Series A Perpetual Stretch Preferred Stock (STRC), was introduced as an income-focused security, promising investors a floating dividend while helping Strategy fund even more Bitcoin purchases.

But that strategy is suddenly being put to the test.

As Bitcoin slid toward the $58,000 mark, confidence across Strategy’s expanding capital stack also cracked. STRC tumbled to a fresh all-time low for the third consecutive trading session, finishing the week nearly 26% below its $100 launch price. The pain was not limited to preferred shareholders. MSTR stock also came under heavy selling pressure as investors grew increasingly uneasy over the company’s complicated financing model, more than $13 billion in unrealized fair-value losses tied to its Bitcoin holdings, and a new investigation from Rosen Law Firm examining disclosures related to profitability, risk management, and capital-raising activities.

To his credit, Michael Saylor has remained unwavering, reiterating that Strategy is committed to Bitcoin, disciplined capital allocation, transparency, credit quality, and creating long-term shareholder value despite the recent turbulence.

With preferred shares hitting record lows, common stock under pressure, and Bitcoin once again driving the story, investors are left wondering whether this is simply another painful shakeout, or a warning sign that the risks inside Strategy’s increasingly layered capital structure are beginning to surface. Let’s take a closer look.

About Strategy

Strategy, led by billionaire Michael Saylor, transformed from a slow-growth software company into the world’s largest corporate holder of BTC over the past six years. It has reinvented itself as the ultimate Bitcoin vault on Wall Street. Fueled by equity, debt, and cash flow, the company aggressively stacks Bitcoin, transforming its balance sheet into a crypto-heavy asset play. It’s not just a software firm anymore, it is a high-voltage gateway to institutional Bitcoin exposure. Its market cap currently stands at $28.85 billion.

Powering that playbook is Stretch, Strategy’s perpetual preferred stock. Designed as an income-focused funding vehicle, STRC pays cash dividends twice a month or monthly, with its dividend rate resetting monthly to encourage trading close to its $100 par value while helping reduce price swings. Listed on Nasdaq, STRC has become a key pillar of Strategy’s long-term Bitcoin acquisition strategy.

For much of last year, Strategy looked unstoppable. As Bitcoin soared, MSTR’s momentum was impressive, rewarding shareholders with eye-popping gains and leaving the broader market in its dust. But what goes up fast can come down just as quickly. Once Bitcoin lost momentum, the tide turned, and Strategy found itself caught in a sharp sell-off.

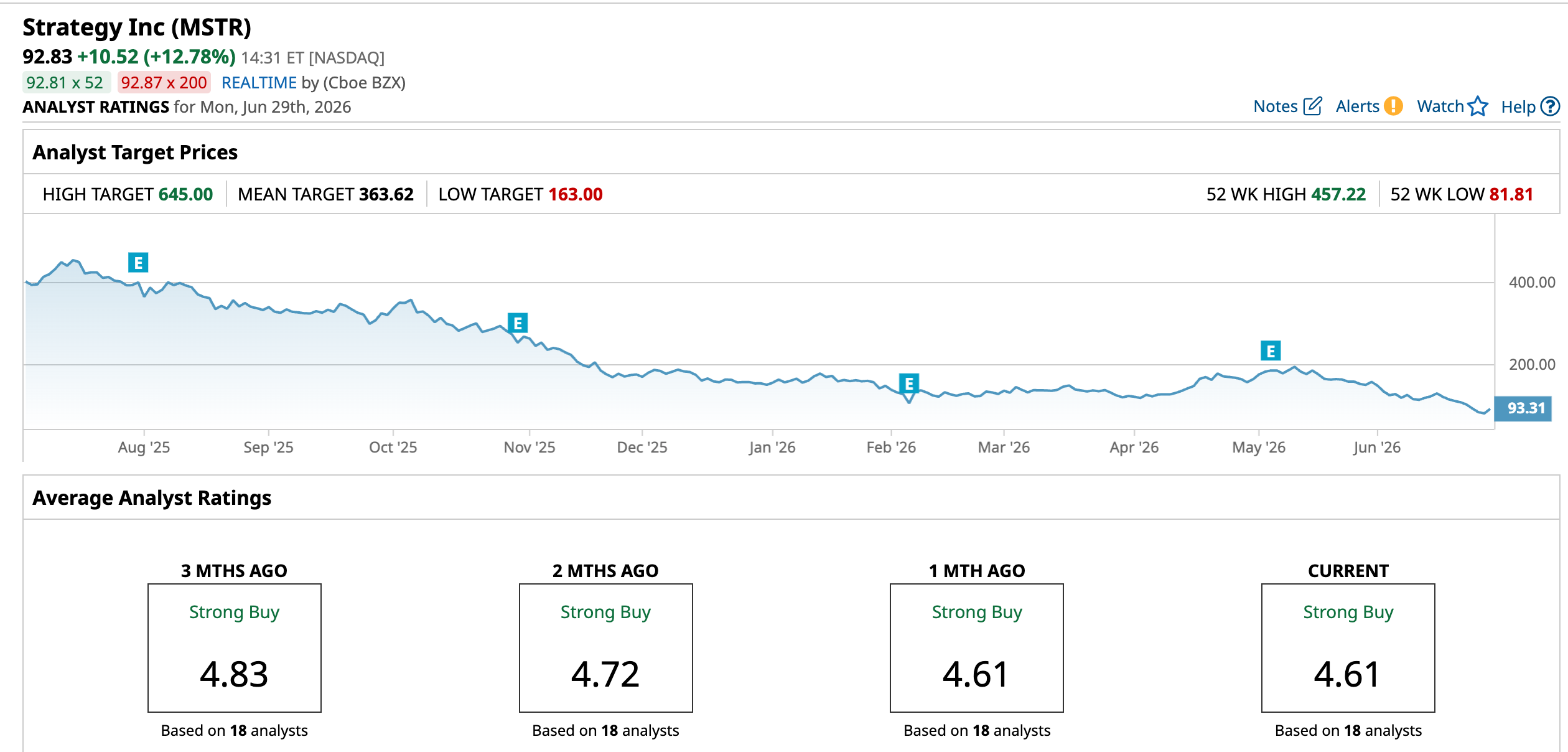

Since hitting a 52-week high of $457.22 last July, MSTR has tumbled 79.7%, touching a 52-week low of $81.81 on June 26. The damage has piled up across every timeframe. The stock is down 75.54% over the past year, has lost 38.2% in 2026 alone, fallen 41% over the last month, and shed another 14.2% in just the past five trading sessions.

The pressure has not stopped with the common shares. STRC, the preferred stock that sits at the heart of Strategy’s Bitcoin funding machine, has become the latest casualty. Designed to trade around its $100 par value, STRC recently plunged to a record low of $71.25. It has dropped 14.8% over the past month and nearly 5% in the last five days, reflecting growing investor unease about Strategy’s ability to keep raising capital on attractive terms.

Still, the story is not over. Strategy has not missed a dividend payment on STRC or any of its preferred securities. With the next payout due in July, investors will be watching closely. If that payment arrives without a hitch, it could ease concerns that the recent sell-off reflects deeper cracks in Strategy’s funding model.

Strategy’s valuation still looks surprisingly modest. The stock trades at a forward non-GAAP price-to-earnings of just 2.65 times, well below both the broader sector average and its own historical norm. Wall Street still seems to be figuring out how to value a company that's part software business, part Bitcoin treasury, and part capital markets machine.

Then there’s STRC. The preferred stock, with a dividend yield of 15.42%, giving income-focused investors something to chew on. Its first semi-monthly dividend of $0.48 per share is scheduled for July 15, a move Strategy hopes will improve liquidity and help steady the stock over time.

Taking A Closer Look At Strategy’s Q1 Earnings Report

Strategy reported its fiscal 2026 first-quarter results on May 5, and both the top and bottom line missed Wall Street’s projections. Revenue rose nearly 12% from a year ago to $124.3 million, but still fell short of expectations. Even more eye-catching was the company’s GAAP loss of $38.25 per share, driven by a staggering $14.46 billion unrealized hit on its Bitcoin portfolio as crypto prices slumped during the quarter.

Here’s the catch, though. Those losses did not come from selling Bitcoin. They were largely accounting adjustments tied to the market value of the company’s holdings. Meanwhile, the business that Strategy originally built its name on – enterprise software – continued to quietly do its job. Gross profit came in at $83.4 million, while gross margin stayed strong at 67.1%, suggesting the operating business remains on solid footing.

Management, meanwhile, showed little interest in changing the playbook. CFO Andrew Kang reiterated that the goal is still the same: raise capital, buy more Bitcoin, and hold it for the long haul.

One of the biggest pieces of that plan is STRC, the company’s income-focused preferred stock. Michael Saylor described it as a scalable funding engine backed by Bitcoin and cash reserves. In less than a year, STRC has already raised about $8.5 billion, making it the world's largest publicly traded preferred stock, and giving Strategy another powerful tool to keep expanding its Bitcoin treasury.

Meanwhile, analysts monitoring Strategy project the company’s bottom line to rise 866.2% YOY and generate a profit of $116.70 per share in fiscal 2026. But in fiscal 2027, EPS is anticipated to decline 36% annually to $74.73.

What Do Analysts Expect for Strategy Stock?

Despite the recent turmoil, not everyone on Wall Street is losing faith in Strategy. On June 22, the company disclosed that it had purchased additional 520 Bitcoin for $35 million, while also selling $335.5 million worth of MSTR shares and boosting its U.S. dollar reserve by $300 million to roughly $1.4 billion. That larger cash cushion is one reason Benchmark analyst Mark Palmer reiterated his “Buy” rating and maintained a $570 price target on the stock.

Palmer also pushed back against comparisons between STRC’s sharp decline and the 2022 TerraUSD-Luna collapse. In his view, the two are fundamentally different. STRC was never designed as a stablecoin or a token pegged to a fixed value, so its recent drop is not a “depeg” but rather the market demanding a higher yield. He argues investors should instead focus on STRC’s variable dividend reset mechanism, Strategy's growing cash reserves, and the flexibility those reserves provide during tougher capital markets.

Perhaps most importantly, Palmer believes the recent sell-off in both STRC and MSTR is better viewed as a stress test of Strategy’s financing model, not evidence that the model itself is breaking down.

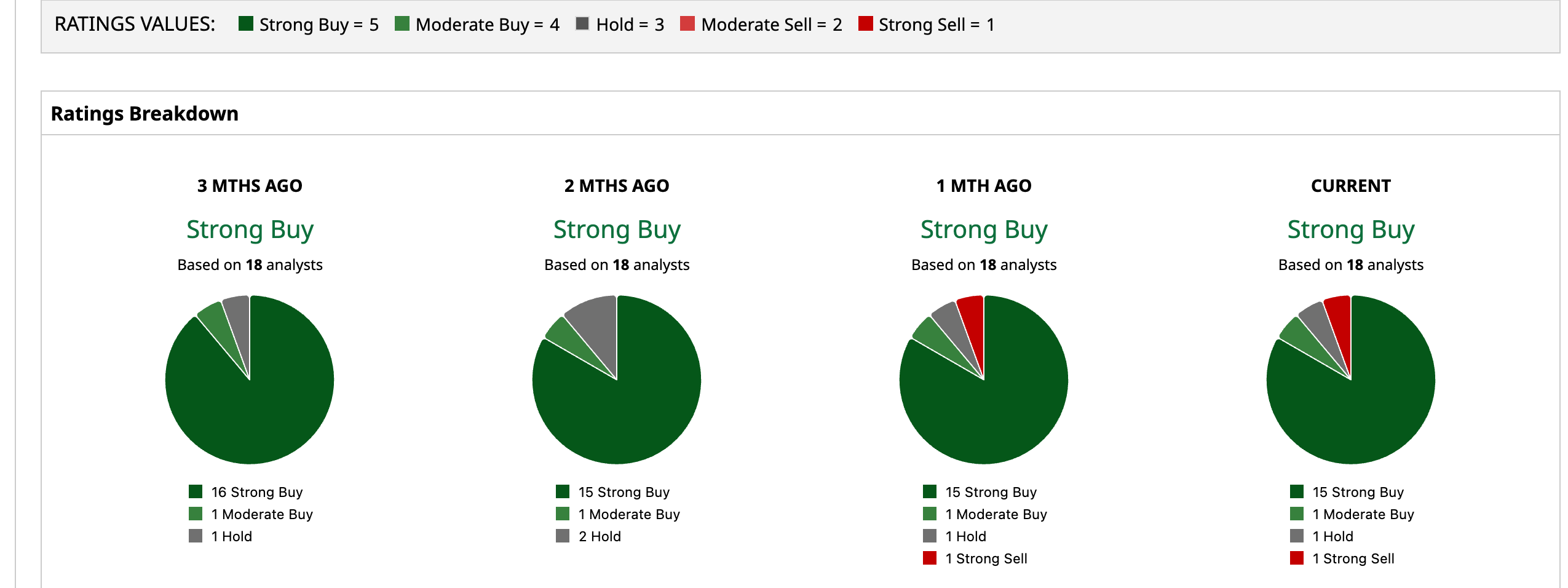

Overall, Wall Street appears to be optimistic about MSTR stock, with a consensus “Strong Buy” rating. Of the 18 analysts offering recommendations, 15 are giving it a solid “Strong Buy,” one suggests a “Moderate Buy,” one is playing it safe with a “Hold” rating, and the remaining one advocates a “Strong Sell.”

The average analyst price target of $363.62 indicates impressive 291.7% rebound potential from the current price levels. The Street-high price target of $645 suggests that MSTR could rally as much as 594.8% from here.

Final Thoughts on MSTR and STRC

Despite the recent sell-off, Michael Saylor is not backing away from his Bitcoin playbook. On Sunday, he shared StrategyTracker data on X showing the company now holds 847,363 Bitcoin, accumulated through 114 separate purchases at an average cost of $75,651 per coin. Saylor even hinted that more purchases could be on the way, posting, “We’re gonna need more charts.”

That is encouraging if you are a long-term Bitcoin bull, but it is also where the debate begins. Critics, including, Ripple CEO Brad Garlinghouse recently argued that while he remains bullish on Bitcoin, Strategy’s debt- and preferred stock-funded buying spree has created unnecessary stress across the broader crypto market. Those concerns have only intensified after STRC’s sharp decline and MSTR’s recent pullback.

Investors are also watching whether the company can comfortably support its growing stack of preferred securities. Strategy reportedly still has about 10 months’ worth of dollar reserves to cover STRC’s dividend obligations, suggesting the company has some breathing room despite the market’s growing skepticism.

Still, MSTR is likely to remain closely tied to Bitcoin’s next move. If the cryptocurrency rebounds, sentiment could quickly improve. If volatility continues, investors should expect plenty more twists before this story plays out.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)