Shares of Strategy (MSTR), the firm formerly known as MicroStrategy, are worth a serious look for investors right now. Why? The company's relentless Bitcoin (BTCUSD) accumulation strategy — now supercharged by a fast-growing credit product — is building a flywheel that could reward long-term shareholders.

Despite a rough first quarter, Strategy wasted no time getting back to business. According to reports, just days after the Q1 earnings call, the company quietly snapped up 535 more BTC between May 4 and May 10, spending roughly $43 million at an average price of around $80,300 per coin. That has lifted Strategy's total holdings to approximately 818,900 BTC, accumulated for nearly $62 billion at an average cost of around $75,500 per coin.

Why Strategy's Q1 Loss Shouldn't Scare You Off

Yes, Strategy posted a GAAP loss per share of $38.25 in Q1, compared to consensus estimates for a loss per share of $19. Revenue climbed 12% year-over-year (YOY) to $124.3 million, below estimates of $125 million.

The company's operating loss of $14.5 billion was almost entirely driven by a non-cash decline in the fair value of its BTC holdings. Bitcoin's price dropped sharply during Q1, pushing Strategy's reserve value lower on paper.

CFO Andrew Kang put it plainly on the earnings call: the underlying strategy is unchanged. The company is still raising capital, buying Bitcoin, holding it for the long term, and growing Bitcoin per share. Since May 2025, Bitcoin per share has grown 18% YOY. Year-to-date (YTD), Strategy has already generated a 9.4% BTC yield in 2026, putting it ahead of the same point last year.

Michael Saylor's New Favorite Tool: Stretch Preferred Stock

At the heart of Strategy's capital markets push is Stretch, or Series A Perpetual Stretch Preferred Stock (STRC). Chairman Michael Saylor spent a significant portion of the Q1 earnings call making the case for it.

Stretch is a variable-rate preferred stock currently paying an annual dividend yield of 11.5%. It's backed by Bitcoin and U.S. dollar reserves. Saylor described it as “credit engineered,” designed for income, stability, liquidity, and long-term scalability.

The numbers behind its growth are hard to ignore. In roughly nine months, Strategy raised $8.5 billion through Stretch. It's now the largest tradable preferred stock in the world, nearly double the size of Wells Fargo's (WFC) preferred equity. Daily trading volume recently hit $375 million, making it 25 times more liquid than the market's “second-largest preferred.”

Saylor was blunt about his ambitions: he wants Stretch to become the deepest, most liquid credit instrument in the world.

What This Means for Strategy Shareholders

Strategy said that it was pausing Bitcoin purchases after Q1 results. Then, within days, it bought more. According to Saylor, the company now has more tools than ever to grow Bitcoin per share, including selling Bitcoin itself when it makes strategic sense.

President and CEO Phong Le outlined an expanding set of capital levers — selling equity, selling Stretch, and even selling Bitcoin to fund dividends or pay down convertible debt. The goal in every case is the same: increase the amount of Bitcoin held per share of MSTR stock.

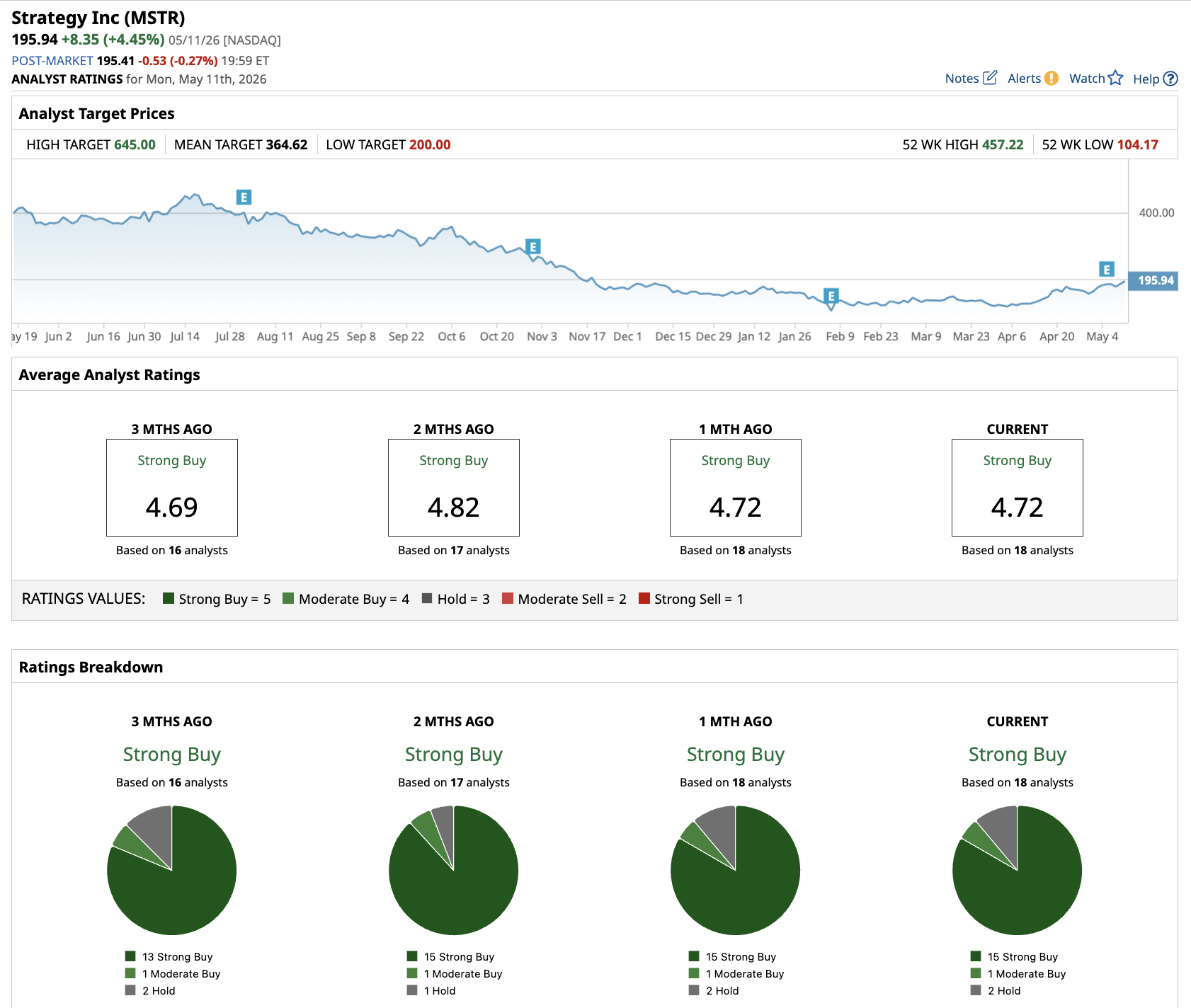

What Do Analysts Think of MSTR Stock?

Wall Street analysts covering Strategy have an average price target of around $365.25, which implies 105% potential upside from current levels. Out of the 18 analysts covering MSTR stock, 15 recommend a “Strong Buy,” one recommends a “Moderate Buy” rating, and two recommend a “Hold” rating.

For investors looking for Bitcoin exposure without holding the asset directly, MSTR stock offers a compelling, if volatile, proxy. The company controls nearly 4% of all Bitcoin that will ever exist, and its balance sheet carries just 9% net leverage against its Bitcoin reserve. Even in a worst-case scenario in which Bitcoin crashes by 90%, the Bitcoin reserve would still cover Strategy's net debt.

MSTR stock is a high-risk, high-conviction bet on Bitcoin's long-term trajectory. If you believe BTC has room to run, Strategy's combination of scale, capital markets sophistication, and growing credit products makes it one of the most interesting ways to play that thesis.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)