/Applied%20Materials%20Inc_%20campus%20sign-by%20Sundry%20Photography%20via%20iStock.jpg)

Applied Materials (AMAT) has found itself in Wall Street's sweet spot after Bank of America Corporation turned even more bullish on the semiconductor industry's artificial intelligence (AI) driven future.

The investment firm now believes visibility into AI-related spending extends through 2028, prompting analysts led by Vivek Arya to lift their CY2027 wafer fab equipment forecast by 4% to $190 billion, representing 31% year-over-year (YOY) growth, up from the previous estimate of $183 billion and 27% growth.

BAC also raised its CY2028 forecast by 23% to $250 billion, implying 32% YOY growth, compared with the earlier projection of $203 billion and 11% growth.

The firm attributed the upward revisions to greater cleanroom availability by CY2028, stronger long-term visibility from memory LTAs, and critical technology inflections that typically push wafer fab equipment spending per wafer higher during memory and logic upcycles.

Furthermore, the bank raised its estimate for the semiconductor industry's total addressable market to $2.7 trillion, reflecting a 28% CAGR between 2025 and 2030, up from its previous forecast of $2.3 trillion.

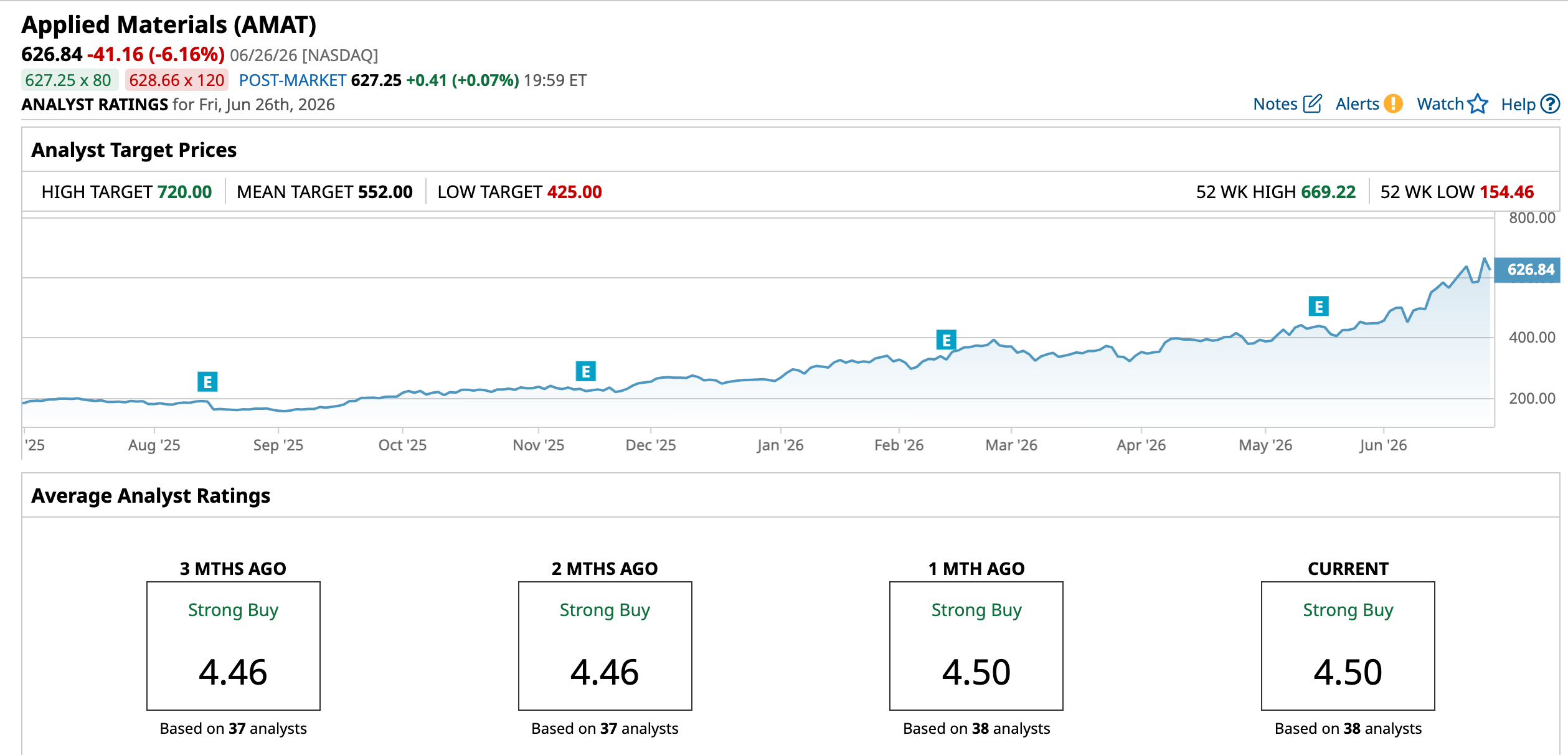

Against that backdrop, Applied Materials emerged as one of the biggest beneficiaries when BoFA raised price targets across several semiconductor names on Tuesday, June 23. The firm boosted its target on AMAT stock to a Street-High of $720 from $540.

Investors wasted little time taking notice. On Thursday, June 25, AMAT stock surged 13.4% during the session, climbing to a new 52-week high of $669.22. With fresh optimism sweeping the semiconductor sector and analysts growing even more bullish, the question is whether Applied Materials still has room to run.

About Applied Materials Stock

Based in Santa Clara, California, Applied Materials builds the tools, software, and services that make modern chip manufacturing possible. With a market cap of $497.7 billion, the company has planted itself at the heart of the semiconductor supply chain through its expertise in materials engineering.

The company also stays deeply involved long after its equipment leaves the factory floor. Its lifecycle solutions help semiconductor manufacturers improve equipment performance, maximize factory efficiency, and keep advanced fabrication facilities operating at peak productivity worldwide.

The leadership has translated into eye-catching returns for investors. AMAT stock has soared 241.56% over the past 52 weeks and has already climbed 143.9% since the beginning of the year. Shares rallied another 85.2% during the past three months and have added 37.8% in the last month.

Such a remarkable run rarely comes cheap. The stock is currently trading at 55.19 times times forward adjusted earnings and 14.91 times sales. Both valuation multiples are above the broader industry and the company's own five-year averages. This shows that investors remain willing to pay a premium for its market leadership, scale, and long-term prospects.

In addition, the company has rewarded shareholders with steadily rising payouts. Applied Materials has increased its dividend for eight consecutive years and now pays $2.12 per share annually, yielding 0.32%. Moreover, on June 9, the board approved a quarterly cash dividend of $0.53 per share, payable on Sept. 10 to shareholders of record as of Aug. 20.

Applied Materials Surpasses Q2 Earnings

Applied Materials kept the good news coming when it reported its Q2 FY2026 results on May 14. Revenue climbed 11.4% YOY to $7.9 billion, beating analysts' estimate of $7.7 billion. Adjusted EPS also came in ahead of expectations, rising 19.7% from the same period last year to $2.86, compared with the Street's forecast of $2.68.

The strength ran much deeper than the headline numbers. Semiconductor Systems turned in another record quarter, generating $5.97 billion in revenue after posting 10.4% YOY growth.

Applied Global Services (AGS) also reached a record, with revenue increasing 17.3% YOY to $1.67 billion, as higher fab utilization provided an additional lift. Meanwhile, Other revenue landed at $280 million, exactly in line with expectations.

Margins told an equally cheering story. Applied Materials delivered its highest gross margin in more than 25 years. Non-GAAP gross margin expanded 80 basis points from a year earlier to reach 50%, driven by value-based pricing across its most differentiated products and continued manufacturing cost innovations.

The company's cash generation remained healthy throughout the quarter. Operating cash flow totaled $845 million, while capital expenditures came in at $635 million, leaving free cash flow at $210 million.

Management believes three powerful forces continue to push the business forward. The rapid global buildout of AI computing infrastructure remains the primary growth engine. The company's leadership in leading-edge foundry logic, DRAM, and advanced packaging keeps it planted in the industry's highest-value markets. Strong execution across its operations and supply chain rounds out the list, helping Applied Materials capitalize on demand.

That momentum has carried straight into management's outlook for the current quarter. The company expects Q3 FY2026 revenue of $8.95 billion, plus or minus $500 million, representing nearly 23% YOY growth. It also forecasts non-GAAP EPS of $3.36, plus or minus $0.20, reflecting nearly 36% YOY growth.

Wall Street appears to share that optimism. Analysts currently expect Q3 FY2026 EPS to climb 35.1% YOY to $3.35. Looking further ahead, they project full-year FY2026 EPS of $12.10, representing 28.5% growth from the previous year. They expect earnings to continue marching higher in FY2027, reaching $15.96 for another 31.9% increase.

What Do Analysts Expect for Applied Materials Stock?

Wall Street has become increasingly upbeat on Applied Materials following the company's strong execution and improving industry outlook. Cantor Fitzgerald analyst C.J. Muse reiterated his “Buy” rating on the stock while raising his price target to $650 from $575.

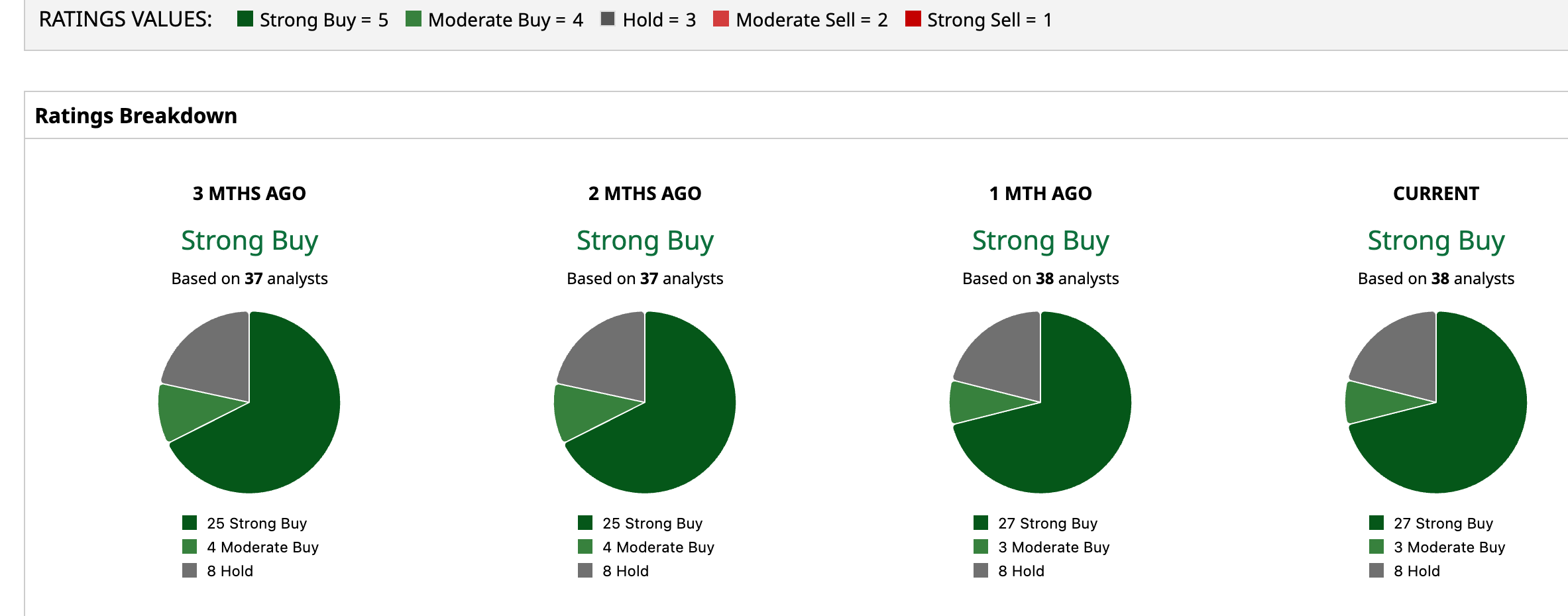

Wells Fargo analyst Joseph Quatrochi also reaffirmed a “Buy” rating and set a price target of $715 on AMAT stock. Analysts have assigned AMAT stock an overall rating of “Strong Buy.” Among 38 analysts covering the stock, 27 maintain a “Strong Buy” rating, three recommend “Moderate Buy,” and eight suggest “Hold.”

Given the stock’s blistering rally, AMAT has already powered past the Street's average price target of $552. Even so, Bank of America's Street-High target of $720 still points to another 14.9% upside from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)