/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

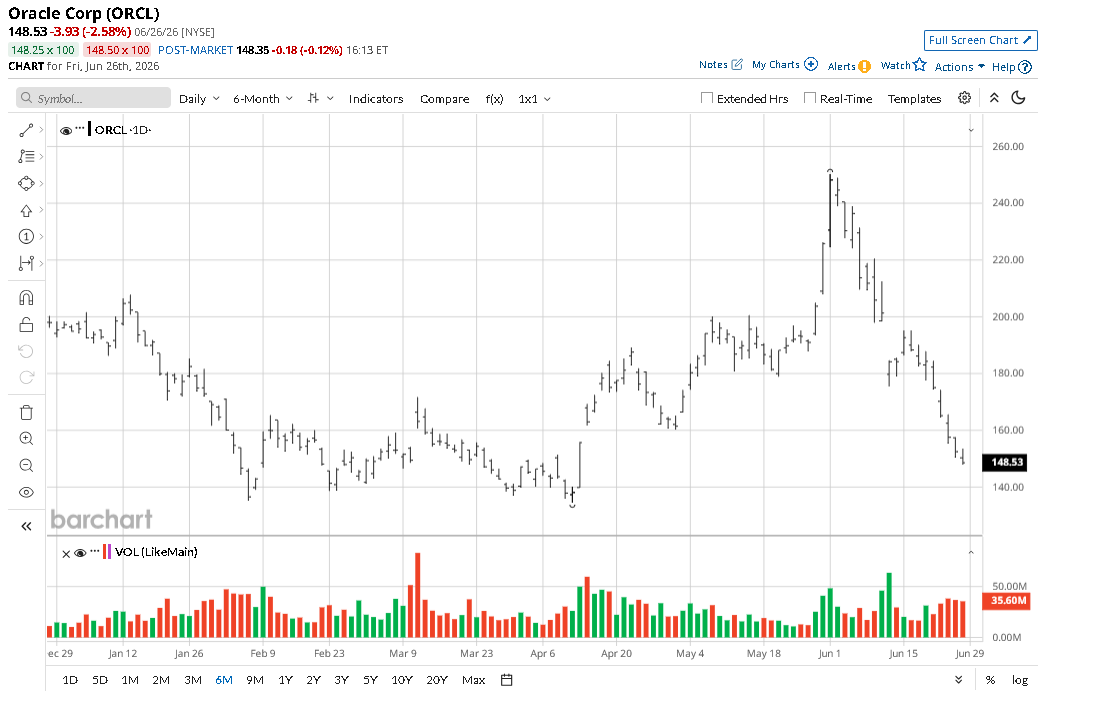

Oracle (ORCL) stock closed down 2.58% on June 26 following a New York Times report that OpenAI is considering postponing its blockbuster initial public offering (IPO) until 2027.

Investors are heavily penalizing ORCL primarily because of its deep infrastructural ties and over-concentration in the frontier artificial intelligence (AI) model developer.

Following today’s decline, Oracle shares are down more than 40% versus their year-to-date high.

What OpenAI’s Delayed IPO Would Mean for Oracle Stock

Oracle has staked much of its modern growth narrative on being the cloud infrastructure backbone for premier AI entities, particularly OpenAI.

However, this hyper-concentration is now exposing the company to extreme capex vulnerabilities. Building out massive AI data centers to support OpenAI’s computing needs requires an exorbitant amount of upfront cash and debt financing.

With OpenAI delaying its liquidity event to 2027 to protect CEO Sam Altman’s strict $1 trillion valuation floor, Oracle investors are getting frustrated over debt-funded AI spending.

ORCL shares ended in the red mostly because if OpenAI remains private for longer to absorb high operational burn rate, it will be forced to carry massive, unmonetized infrastructure outlays on its balance sheet without the clean exit valve or immediate commercial windfall an IPO would provide.

Investors Are Preemptively Selling ORCL Shares

The deferred IPO timeline signals broader friction within the artificial intelligence landscape, compounding fears that enterprise demand may not scale fast enough to justify the pace of Oracle’s buildout.

While the giant boasts an impressive backlog of $553 billion, an extended stay in the private market for OpenAI could decelerate the speed at which these multibillion-dollar contracts translate into “recognized” revenue.

Plus, if market volatility or government oversight slows down major AI deployments – such as the reported staggered rollout of GPT 5.6 model – ORCL faces acute threat of immediate infrastructure overcapacity.

Investors are preemptively selling off Oracle shares out of fear that the company is “overbuilding” complex cloud systems for an AI sector whose ultimate profitability runway has just been pushed further into the future.

How Wall Street Recommends Playing Oracle

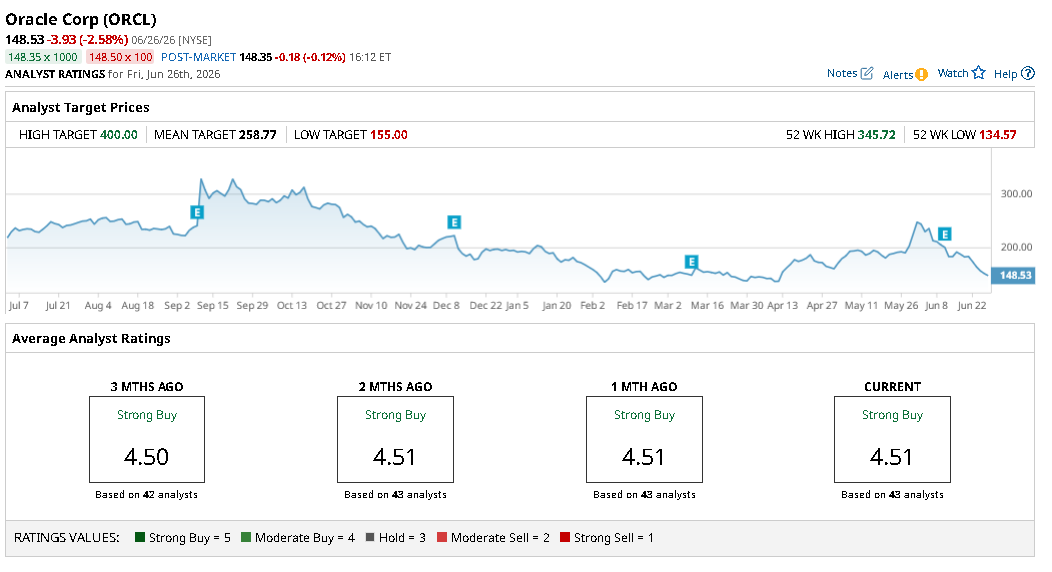

Despite recent weakness, however, Wall Street remains bullish on ORCL stock for the next 12 months.

The consensus rating on Oracle Corp sits at “Strong Buy” currently, with the mean price target of about $259 indicating potential upside of nearly 75% from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)