Last week, Delta Air Lines, Inc. (DAL) stated that its board of directors had announced an increase in its quarterly dividend payout, reflectingthe company’s commitment to boosting shareholder value, apart from underlining confidence in its business.

Dividend-paying stocks provide a solid income stream and have fewer chances of experiencing wild price swings. Dividend stocks are safe bets for creating wealth, as the payouts generally act as a hedge against economic uncertainty, like the current scenario.

Given this backdrop, the question that naturally arises is: Should investors buy, hold, or sell DAL stock now? A more in-depth analysis is needed to make that determination. Before diving into DAL’s investment prospects, let’s take a glance at its financial numbers.

DAL’s Recent Dividend Increase of 15%

In a shareholder-friendly move, Delta Air Lines’ board of directors approved a dividend hike of 15%, thereby raising its quarterly cash dividend to 21.50 cents per share (86 cents annualized) from 18.75 cents (75 cents annualized). The raised dividend will be paid on July 30, 2026, to stockholders of record at the close of business on June 9, 2026. The move underscores DAL's strong financial position and robust cash-flow generation, highlighting its commitment to delivering value to shareholders.

Delta Air Lines, Inc. Dividend Yield (TTM)

Delta Air Lines, Inc. dividend-yield-ttm | Delta Air Lines, Inc. Quote

Delta Air Lines has consistently increased its dividend since reinstating shareholder payouts in 2023, raising its quarterly dividend by 50% to 15 cents per share in 2024, followed by a 25% increase to 18.75 cents per share in 2025 and a further 15% hike to 21.50 cents per share in 2026. Overall, the quarterly dividend has more than doubled from its 2023 level, reflecting Delta Air Lines' strengthening financial position, robust cash-flow generation and commitment to enhancing shareholder returns. Such shareholder-friendly initiatives should boost investor confidence and positively impact the bottom line.

Apart from being shareholder-friendly, Delta Air Lines is benefiting from resilient travel demand, particularly in premium and international markets, which continues to support its revenue growth and cash generation. Delta Air Lines continues to invest in AI and data-driven tools to improve retailing and the customer experience. Delta Sync now supports logged-in experiences across onboard channels. Backed by a strong financial position, the airline remains well-positioned to continue rewarding shareholders through dividend growth and other capital-return initiatives.

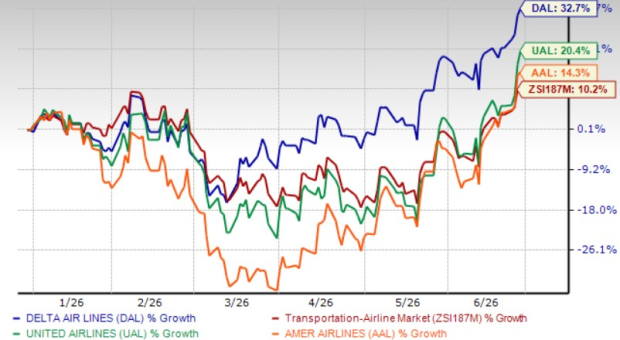

DAL Stock’s Price Performance

Shares of DAL have gained 32.7% so far this year, outperforming the Zacks Airline industry’s 10.2% growth, as well as that of other industry players, American Airlines Group Inc. (AAL) and United Airlines Holdings, Inc. (UAL), within the same time frame.

DAL Stock's YTD Price Comparison

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Headwinds Weighing on DAL Stock

The ongoing conflict in the Middle East has led to a rise in oil prices, and airlines remain exposed because most U.S. carriers have abandoned broad fuel-hedging strategies. Delta Air Lines' June-quarter outlook assumes a fuel price of approximately $4.30 per gallon at the forward curve as of April 2, 2026. Management said that this adds more than $2 billion of additional fuel expense compared to the start of the year, partially offset by an expected refinery benefit of about $300 million.

Higher labor and recovery costs continue to bother airlines. Delta Air Lines' non-fuel cost base continues to move higher, led by wages and crew-related items. Salaries and related costs increased 8% in 2025 to $17.5 billion, reflecting wage increases, including for pilots. In the March quarter, non-fuel CASM (CASM-Ex) increased 6% year over year to 15.13 cents, with management citing higher recovery costs and the continuation of higher crew-related costs. These cost pressures are likely to hurt margin expansion, even when demand looks healthy.

Airline stocks’ market volatility continues to remain a concern. Management highlighted heightened volatility in fuel markets and is adjusting capacity with a downward bias until the fuel environment improves. With earnings sensitive to these external variables, DAL may not fit investors who are uncomfortable with sharp day-to-day swings in airline shares.

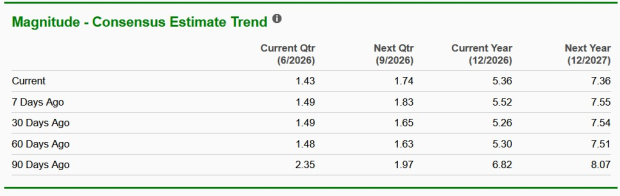

What Do Earnings Estimates Say for DAL?

The negative sentiment surrounding DAL stock is evident from the fact that the Zacks Consensus Estimate for the second quarter of 2026 and the third quarter of 2026 earnings has been revised downward in the past 90 days. The consensus mark for 2026 and 2027 earnings has also been projected southward in the past 90 days.

The unfavorable estimate revisions indicate brokers’ lack of confidence in the stock.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Unattractive Valuation Picture for DAL Stock

Delta Air Lines looks expensive from a valuation standpoint. Considering the forward 12-month price-to-sales ratio (P/S-F12M), DAL is trading at a premium compared to the industry.

The stock has a forward 12-month P/S-F12M of 0.92X compared with 0.63X for the industry over the past five years. The company’s forward 12-month P/S-F12M ratio is also above the median level of 0.53X over the past five years. These factors indicate that the stock’s valuation is unattractive.

DAL's P/S Ratio (Forward 12 Months) Vs. Industry

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Not an Opportune Time to Buy DAL Stock

Delta Air Lines benefits from resilient demand for travel and a revenue mix that leans increasingly toward premium, loyalty and other higher-margin streams. Resilient travel demand, premium mix, loyalty partnerships, and technology-led personalization support revenue durability, cash generation, and strategic flexibility over cycles. Backed by a strong financial position, the airline remains well-positioned to continue rewarding shareholders through dividend growth and other capital-return initiatives.

Despite these positives, we advise investors not to buy DAL stock now due to the headwinds it continues to face, such as fuel price volatility, rising labor and recovery costs and macro uncertainty, which can pressure margins and amplify near-term earnings swings for shareholders. Share price volatility and unattractive valuation are concerning.

We, therefore, advise investors to wait for a better entry point. For those who already own the stock, it will be prudent to stay invested. The company’s current Zacks Rank #3 (Hold) justifies our analysis. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)