GE Vernova (GEV) stock has delivered solid gains, rising 67% year-to-date (YTD) and 117% in the past 12 months. Despite more than doubling over the past year, its accelerating order growth, expanding backlog, and favorable industry tailwinds indicate that GEV stock isn’t done climbing and could sustain the upward trajectory.

GE Vernova provides power-generation equipment, grid technologies, and energy storage systems, and is currently benefitting from surging electricity demand. Global electricity demand continues to rise as industrial activity expands, advanced manufacturing facilities are built, artificial intelligence (AI) drives a wave of data-center investment, and economies increasingly electrify transportation and buildings. These structural trends are creating sustained demand for the infrastructure required to generate, transmit, and manage power.

Record Orders Highlight Strong Demand Environment

GE Vernova's first-quarter 2026 results highlighted the strength of this demand environment. The company reported $18.3 billion in orders during the quarter, representing a 71% year-over-year (YOY) increase. This surge reflects broad-based customer demand across its portfolio.

The company's backlog also expanded significantly, increasing by $13 billion sequentially. The growth was supported by both equipment and service orders.

Revenue increased 7% YOY in Q1, driven by growth in both equipment sales and service offerings. At the same time, GE Vernova improved its adjusted EBITDA margin by 390 basis points.

Looking ahead, strong orders, a rapidly expanding backlog, and favorable secular demand drivers position GE Vernova for continued growth.

Power Demand Is Accelerating — And GE Vernova Is Benefiting

The company’s Power segment continues to be a major growth driver, delivering another exceptionally strong quarter characterized by robust demand, accelerating revenue growth, and meaningful margin expansion. Orders rose sharply, with total Power orders up 59% YOY. Growth was driven by Gas Power equipment orders, which more than doubled as turbine demand strengthened and pricing improved. Power services orders also remained robust, increasing 29%, supported by Nuclear Power upgrades and expanding Gas Power service activity.

Power segment revenue grew 10%, reflecting the effective conversion of GE Vernova's growing backlog into sales. Equipment revenue benefited from higher volumes and better pricing, while gas turbine shipments increased 32% to 25 units. Services revenue also expanded, aided by stronger nuclear activity.

Profitability remained strong, with EBITDA margin expanding 500 basis points to 16.3%. The margin gains were primarily driven by pricing and operating leverage, indicating that incremental demand is translating into disproportionately higher earnings.

The outlook remains highly constructive. Management noted that April equipment orders alone exceeded total Q1 orders, while pricing for first-half 2026 bookings is expected to be “10 to 20 points higher” than late-2025 levels. Beyond near-term growth, the expanding turbine installed base should drive a larger, recurring, and higher-margin services business over the coming decade, strengthening the segment’s long-term earnings profile.

Grid Modernization Is Creating a Second Growth Engine

While the Power segment continues to thrive, the Electrification business has been another major growth driver. Orders surged 86% YOY to approximately $7.1 billion and remained at an exceptional 2.5 times quarterly revenue, indicating demand is substantially exceeding current sales levels.

The growth was driven by rising investment in grid infrastructure as utilities and governments work to modernize aging power networks and support growing electricity consumption. Demand was particularly strong for substations, high-voltage direct current (HVDC) systems, transformers, and switchgear.

Geographically, North America and Asia delivered impressive results, with equipment orders nearly tripling YOY.

Importantly, order growth continues to outpace revenue recognition, leading to substantial backlog expansion. Including Prolec's contribution, the Electrification equipment backlog reached $39 billion, up roughly 75% YOY. This record backlog provides a strong foundation for future revenue growth and enhances visibility into the segment's long-term performance.

Execution was equally impressive. Segment EBITDA “more than doubled,” while EBITDA margin expanded 590 basis points to 17.8%. Higher volumes, productivity gains, and favorable pricing all contributed to the margin improvement, demonstrating both operational discipline and strong market conditions.

Looking ahead, the combination of a record backlog, sustained order momentum, and improving operational efficiency suggests the segment remains well-positioned for continued revenue growth and healthy margin expansion.

Why GE Vernova Stock Could Continue Climbing

GE Vernova’s record backlog, sustained order momentum, pricing power, and improving operational efficiency suggest it remains well-positioned for continued revenue growth and margin expansion. With both the Power and Electrification segments benefiting from long-term electrification trends, data-center growth, and grid-modernization spending, the company's earnings outlook remains favorable. These factors support the view that GE Vernova's rally may still have further room to run.

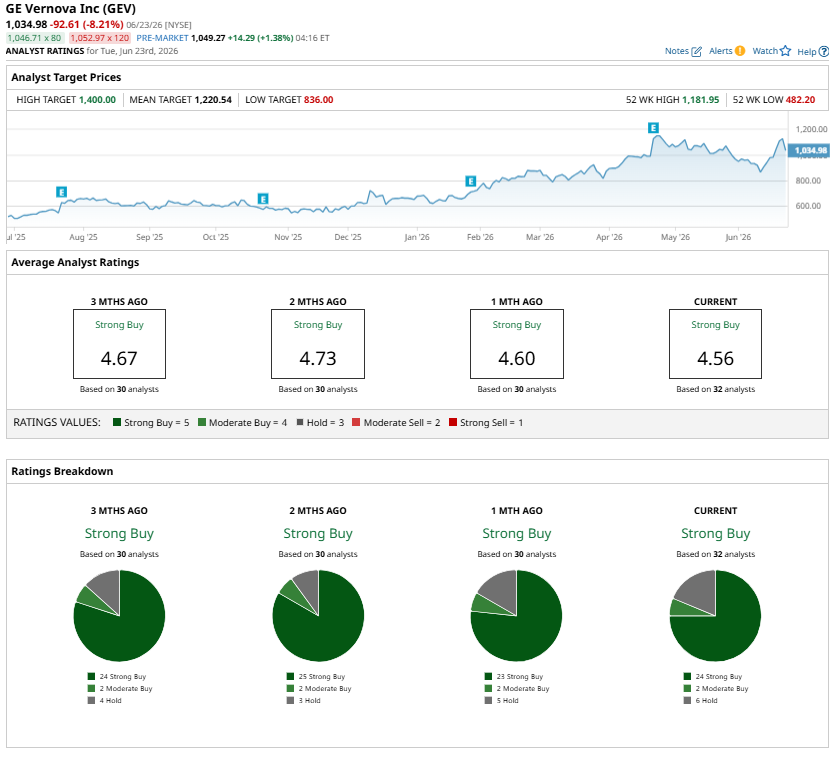

Wall Street remains optimistic on the stock. Analysts maintain a “Strong Buy” consensus rating on GEV stock with an average price target of $1,220.54 per share.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)