/Dominos%20Pizza%20Inc%20storefront%20by-KathyDewar%20via%20iStock.jpg)

While many of us might crave pizza, the sector has been out of favor with markets for some time now. Yum! Brands (YUM) recently sold Pizza Hut for a total consideration of $2.7 billion, while Papa John's (PZZA) is reportedly weighing a $1.5 billion offer from Qatari royal family-backed Irth Capital Management. Both Pizza Hut and Papa John’s have been on a store-closure spree in the U.S. amid stagnant sales.

Domino’s Pizza (DPZ) has also announced a leadership transition plan, as CEO Russell Weiner is set to retire. Weiner will be succeeded by current Chief Operating Officer Joe Jordan, effective October 1, 2026. DPZ stock has tumbled this past week following the announcement, but the pullback has come amid a broader market selloff, with Papa John’s shares falling almost 6% on June 22.

Notably, even Warren Buffett’s Berkshire Hathaway (BRK.A) lost money on Domino’s Pizza and exited its position in the first quarter of 2026, which was incidentally the first quarter under new CEO Greg Abel. While I have been bearish on DPZ stock all this time, I also previously noted that the stock's risk-reward has started to look attractive. However, DPZ stock has continued its downward trajectory since then.

The fall has pushed the dividend yield up to 2.7% as of this writing. Let’s examine whether it's time to double down on DPZ stock or give up on shares, which hit a 52-week low of $282 on June 23.

The Pizza Industry Is Facing Several Headwinds

The pizza industry is facing several headwinds and has lost out to other cuisines. Pizza restaurants, which were once second in sales in the U.S., dropped to sixth place in 2024. Consumers have been pivoting to healthier options, including high-protein ones. The beverage industry saw the writing on the wall and launched several healthier (or rather less unhealthy) alternative beverages in response. Pizza chains have also tried their hand at healthier alternatives, particularly with tweaks in pizza crusts, but these offerings don’t seem to be having much of an impact.

Moreover, pizza chains have lost some of their moat with the advent of delivery apps like Uber's (UBER) Uber Eats and DoorDash (DASH), which allow smaller restaurants to offer delivery to customers. With nearly every restaurant now offering delivery, buyers have multiple convenient cuisine options to choose from. To make things worse, tepid sales have triggered a pizza price war in the U.S., and players have been offering promotions to lure buyers.

Apart from these deep-rooted issues, soaring gas prices have lowered disposable incomes. Today, many lower- and middle-income families are not spending as much on outside food as before.

The Bull Case for Domino’s Pizza

Meanwhile, the pizza industry should stabilize, as there are signs of consolidation. We can be reasonably sure that Pizza Hut’s new owner will attempt a turnaround, which invariably means store closures. There is the possibility of the company attempting a growth strategy by doubling down on promotions, but I see that as quite remote. As its competitors close stores, Domino’s may be able to increase its market share.

On the macro side, gas prices have dropped, although the truce in Iran looks fragile. However, both sides have incentives to wrap up the war sooner rather than later, and oil markets are pricing an imminent end to the conflict. Easing gas prices should help take some pressure off monthly budgets, which is theoretically positive for the restaurant industry. The leadership transition at Domino's does add an element of uncertainty, but I don’t expect dramatic changes since the company has picked an insider for the job.

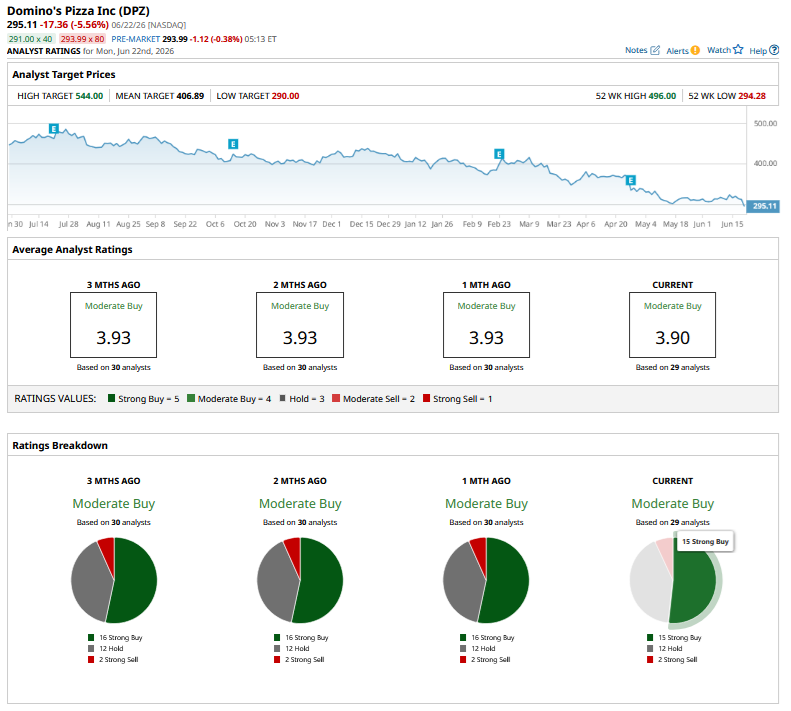

What Do Analysts Think of DPZ Stock?

Brokerages are modestly bullish on Domino’s stock with a consensus “Moderate Buy” rating. Out of 29 analysts with coverage, 15 have a “Strong Buy" rating, 12 analysts rate the stock as a “Hold,” and two analysts have a “Strong Sell.” The mean target price of $404.21 represents potential upside 39% from here. DPZ stock currently trades only slightly above its Street-low price target of $290, which is reflective of the pessimism toward the stock.

Should You Buy Domino’s Pizza Stock?

While Domino’s is not operating in the hottest of industries, I see it as a value play now at a forward price-to-earnings (P/E) multiple of 15.4 times, which is well below where the S&P 500 Index ($SPX) currently trades. Domino’s has a strong brand and has held its ground against competitors, both in the U.S. and other markets.

While one shouldn’t really expect wonders from DPZ stock, it is a decent buy, particularly for investors looking at quality high-dividend plays. The forward dividend yield is 2.7%, which is over twice the average S&P 500 constituent. The dividend has risen at an annualized growth of 20% over the last decade, and the payout ratio is just over 40%, which is quite comfortable.

DPZ stock would not appeal to growth investors. However, it would fit well for conservative investors who are looking for a high-dividend stock and are comfortable holding a name that can deliver double-digit annualized returns over the medium to long term.

On the date of publication, Mohit Oberoi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.