/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

When investors discuss artificial intelligence (AI), the spotlight usually falls on chipmakers and power infrastructure companies. However, another critical piece of the AI ecosystem that is quietly experiencing explosive growth is networking technology. That's where Credo Technology (CRDO) comes in.

Shares of Credo Technology have surged about 164% over the past three months as demand for its high-speed connectivity solutions continues to accelerate. As AI data centers become larger and more complex, the need to move massive amounts of data efficiently between chips, servers, racks, and entire facilities has become increasingly important.

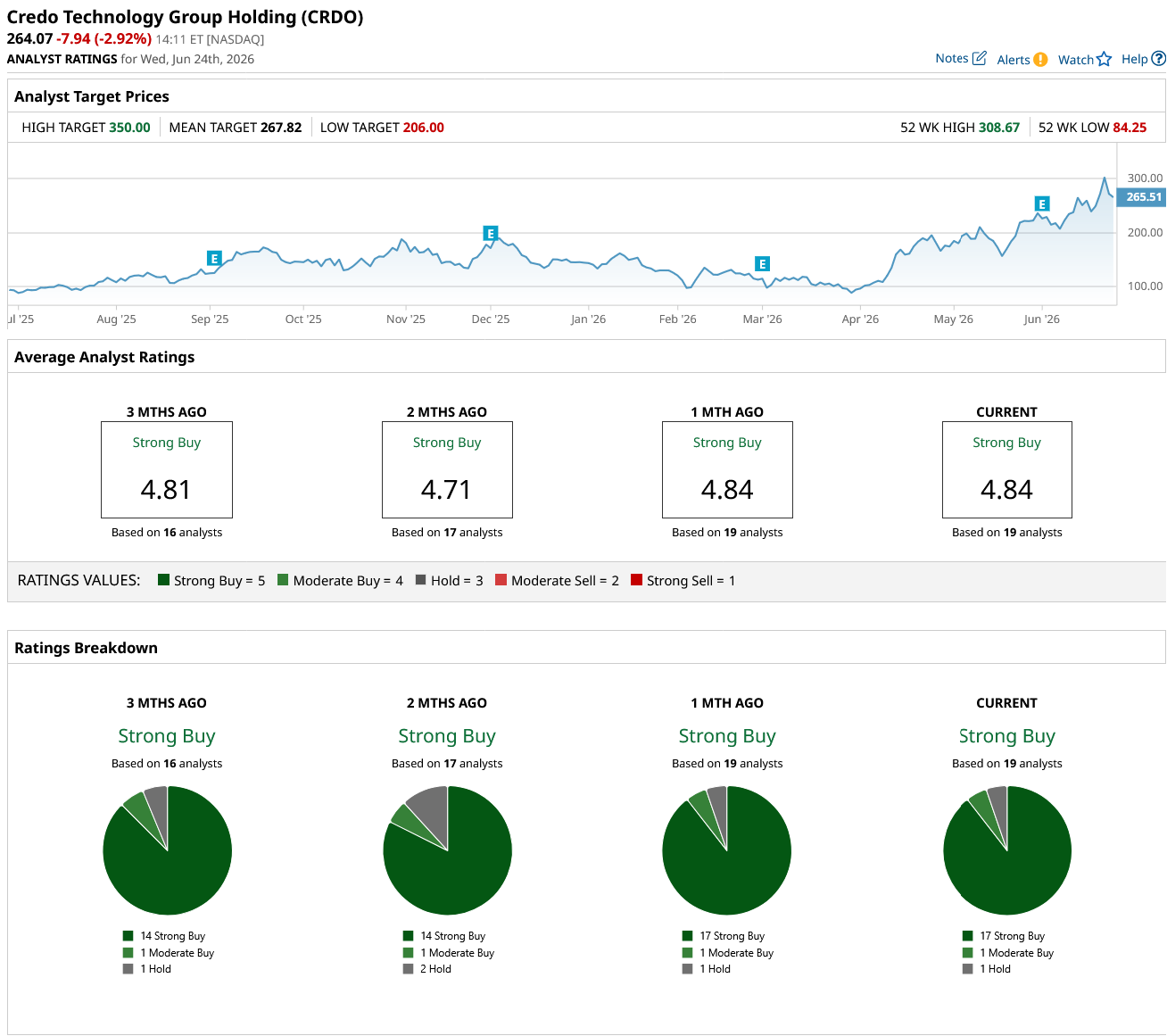

Credo is positioned to benefit from this trend. It provides high-performance copper and optical interconnect solutions across the full spectrum of AI infrastructure. Thanks to strong demand, CRDO stock has already risen significantly in value. However, at least one Wall Street analyst expects CRDO to hit $350—the highest price target currently on the Street. Based on the stock's closing price yesterday of $272.01, that forecast implies approximately 29% additional upside over the next 12 months.

Credo to Sustain Growth Momentum

Credo continues to execute exceptionally well, and the growth momentum in its business will likely sustain. As AI models grow larger and workloads increasingly transition from training to large-scale inference, data center operators are facing mounting challenges related to network bandwidth demands and power efficiency. These trends are driving strong demand for advanced connectivity solutions, creating a favorable backdrop for Credo's product portfolio.

The strength of this demand is evident in the company’s recent financial performance. In fiscal 2026, Credo’s top line exceeded $1.3 billion, representing more than 200% year-over-year (YoY) growth. Profitability expanded even faster, with adjusted net income increasing more than fivefold to $662 million.

Credo also benefits from the ability to deliver multiple generations of connectivity technologies while maintaining deep system-level integration. This positioning allows Credo to address evolving customer requirements as AI clusters become larger, faster, and more complex.

Active Electrical Cables (AECs) remain the company’s primary growth driver. AECs have become a preferred connectivity solution inside AI data centers because they deliver high performance while consuming less power than many alternatives. Adoption has expanded from traditional in-rack deployments to larger multi-rack AI systems, where performance requirements continue to increase.

Management has reported strong demand from hyperscale cloud providers and new AI-focused cloud operators, providing a significant runway for future growth.

Beyond AECs, fiscal 2027 could mark a significant expansion in Credo's optical networking business. The company is seeing increasing adoption across several optical product categories, positioning optics as its next major growth engine. Management expects each of its key optical product lines to generate more than $100 million in revenue during fiscal 2027. Collectively, the optical portfolio is projected to contribute more than $600 million in annual revenue, transforming the business into a meaningful driver of overall growth.

Looking ahead, Credo expects mid-single-digit sequential revenue growth during the first half of fiscal 2027, followed by a stronger acceleration in the second half. This outlook is likely to be supported by the scaling of optical products and continued AI infrastructure deployments. Overall, the company forecasts YoY revenue growth of more than 80% in fiscal 2027.

Valuation Still Attractive

While Credo Technology's stock has delivered impressive gains, its valuation suggests the rally may not be over. CRDO currently trades at a forward price-to-earnings (P/E) ratio of 56.2, a premium that appears justified given the company's robust earnings growth prospects.

Wall Street expects Credo's earnings momentum to remain exceptionally strong, with earnings per share (EPS) projected to surge more than 89% in fiscal 2027, followed by another 50.6% increase in fiscal 2028.

Reflecting confidence in the company's long-term outlook, analysts remain bullish on CRDO. The stock currently carries a "Strong Buy" consensus rating.

The Bottom Line on CRDO Stock

Credo Technology is set to benefit from surging demand for high-speed networking and connectivity solutions. With rapid revenue growth, expanding profitability, and significant opportunities across AECs and optical networking, the company appears well-positioned to sustain its momentum. As a result, CRDO stock could potentially reach $350 over the next 12 months.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)