/Abstract%20concept%20illustration%20of%20digital%20matrix%20by%20KanawatTH%20via%20Adobe%20Stock_.jpeg)

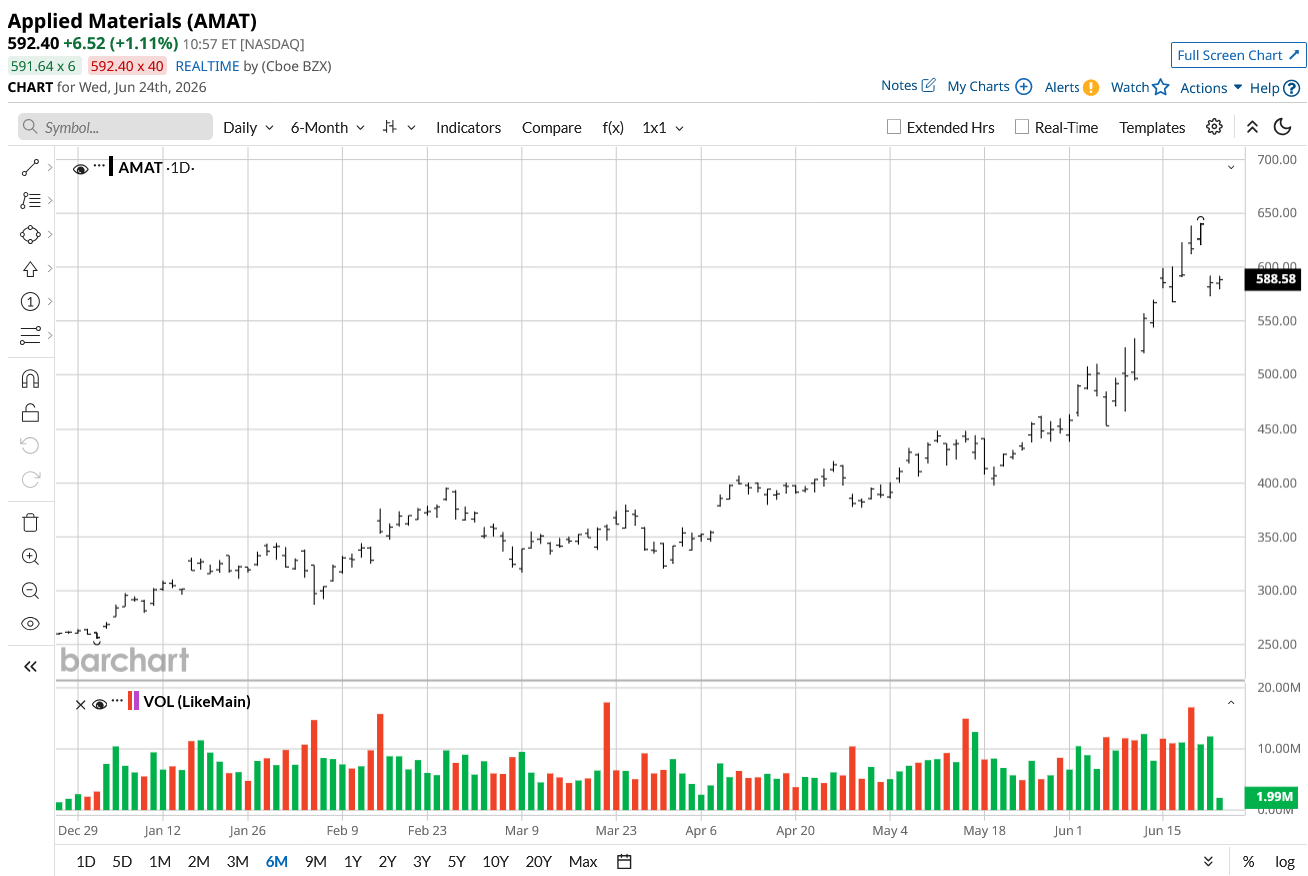

Applied Materials (AMAT) is among the handful of companies that are building the incredibly complex machines that allow foundries to turn bare silicon wafers into advanced processors. It has thus surged massively over the past few years and has a market capitalization close to half a trillion dollars as of this writing. Citi recently doubled down on AMAT stock, plus some competitors that are doing equally as well.

It's worth taking a closer look at these stocks since they are likely to keep surging. Chip demand has shown no sign of slowing down, and analysts are racing to bump price targets. If the rally continues, these AI-adjacent stocks may be the next category to cross the $1 trillion mark and beyond.

A Slew of Price Target Hikes

A wave of aggressive price target hikes for Applied Materials is coming through after a blockbuster Q2 2026 earnings report last month. Analysts are finally warming up to the business due to back-to-back solid earnings reports and what seems to be a very long growth runway.

Applied Materials' guidance suggests more than 30% growth for the broader semiconductor equipment industry this year, and Wall Street is quickly recalibrating.

Citigroup hiked AMAT stock's price target from $550, all the way to $710, with other major institutions doing the same. Bank of America hiked from $540 to $720, and Wells Fargo hiked from $520 to $715. Others are also catching up, albeit more slowly, and are $100-$150 behind on their price targets. Note that the numbers below don't yet capture the BofA's hike due to its recency. The mean price target is likely near $600 now.

More Hikes are Likely—Here's Why

The historical "boom and bust" cycle of the semiconductor equipment industry is being re-evaluated. Analysts increasingly view AI infrastructure build-outs, and the cleanroom expansions required to support them, as a sustained cycle. We are already over three years into the AI hype, and things have only gotten better for AI companies. Hence, the argument that this is a short-lived cyclical pump is waning.

Moreover, Applied Materials is now a high-margin business. A little more than a decade ago, you were looking at net margin in the 1-3% range. Now, it's at 35.5% as of Q1. Wall Street loves a business that has both high sales growth and high margins.

The explosion in demand for High-Bandwidth Memory (HBM) is key for AI GPUs. Applied Materials dominates here, and the barrier to entry is high. As long as AI hardware demand remains strong, AMAT stock can keep rallying.

The Next $1 Trillion Business?

Applied Materials has all the hallmarks of a great business, and the growth could lead it to $1 trillion eventually, though I don't see it happening this year. You are already paying 47 times forward earnings, and that's nearly twice as much as what you pay for Nvidia (NVDA).

Applied Materials is an underdog sub-trillion chip business, and they command higher multiples, but crossing a trillion would require AMAT stock to trade at triple-digit forward earnings multiples. It's difficult to imagine Wall Street paying that much without growth rates of >50%.

As transistors shrink down to the 2-nanometer node and below, chipmakers are changing the physical architecture of the chips themselves (moving to 3D designs). These transitions require exponentially more complex deposition and etching tools. AMAT dominates this specific atomic-level engineering. It's well-positioned to keep growing, so I see $1 trillion as a possibility within 36 months if the rally continues.

Should You Buy AMAT Stock?

I'd buy the dip on AMAT stock before I'd buy the dip on any hyperscaler. This is because the company is on the receiving end of the AI buildout spending and is actively buying back stock, whereas your average Magnificent 7 business with a legacy software arm is now running out of cash trying to build data centers.

In 2014, Applied Materials had 1.2 billion outstanding shares. Today, it has less than 800 million outstanding shares. The higher margins and free cash flow will allow it to double or perhaps triple its buybacks if the AI buildout keeps pace.

Still, I wouldn't buy too heavily into AMAT stock. Most of the rally so far has been forward-looking. The past three years have led to just 6.1% sales growth annually on average. The next three years are expected to bring 20.1% average annual sales growth, which isn't much. You won't outperform the broader market by a wide margin even if Wall Street boosts the premium.

On the date of publication, Omor Ibne Ehsan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.