Aerospace and defense companies have been raising dividends across the board in 2026. In May alone, several names in the sector announced notable dividend hikes. Northrop Grumman (NOC) raised its payout by 7%, RTX (RTX) also lifted its dividend by 7%, and Curtiss-Wright (CW) increased its payout by 8%, even as their shares swung sharply amid geopolitical tension tied to the Iran war.

That tells you big aerospace and defense companies are still putting real money behind shareholder returns, even in a shaky backdrop. The private aerospace and defense sector now generates nearly $1 trillion in annual revenue, and with the U.S. government pointing to a $1.5 trillion defense budget for 2027, the spending backdrop remains supportive.

Against that, on June 15, HEICO (HEI) announced that it was raising its semiannual cash dividend by 8% to $0.13 per share from $0.12. The dividend will be paid on July 15 to shareholders of record as of July 1. The increase marks HEICO’s 96th-straight semiannual cash dividend since 1979, a payout streak that now stretches close to five decades. This move also came right after record fiscal second-quarter 2026 results, with net income up 49% year-over-year (YOY).

So, with record results, a favorable defense spending backdrop, and a dividend streak that is still going strong, is this latest 8% raise the start of more upside for HEI stock shareholders? Let’s find out.

The Financial Performance Behind the HEICO Story

HEICO runs a focused business, making Federal Aviation Administration (FAA)-approved replacement parts and critical electronic components used across commercial aviation and defense, mostly in the aftermarket where demand tends to stay steady.

HEI stock itself has been steady, up about 5% over the past year and roughly 3% so far this year.

That steadiness comes at a premium, though. HEI stock trades at a forward price-to-earnings (P/E) multiple of 58.2 times, which is well above the industrials average of 21 times.

On the dividend front, the company just raised its payout by more than 8%, adding to its streak of dividend increases. Even so, the yield is still low at about 0.07%, with a forward payout ratio of just 4.23%, leaving plenty of room for future hikes. The most recent dividend was $0.12 per share, paid twice per year.

Q2 net income came in at a record $233.8 million, up 49% from last year, while EPS rose to $1.66 from $1.12. Revenue grew 25% YOY while operating income climbed 41% YOY, both hitting new highs. Cash flow was also strong, with operating cash flow up 43% YOY to $292 million and EBITDA rising 37% to $408.3 million. The Flight Support Group led the way, with revenue up 21% YOY to $929.4 million and operating income up 31%, while margins improved to 26.2%. Debt levels moved slightly higher to 1.74 times EBITDA due to acquisitions, but still remain at a manageable level.

Core Drivers Fueling Momentum

HEICO is still using acquisitions to grow. In April, its Flight Support Group bought an 80% stake in Sherwood Avionics and Accessories, a repair company that handles complex components for defense and some commercial aircraft. Around the same time, the Electronic Technologies Group picked up a 90% stake in Southwest Antennas, which makes rugged antennas used in defense and law enforcement. Management expects both deals to start adding to earnings within a year, and says there are still more acquisition opportunities in the pipeline.

On the product side, HEICO is also expanding into space-focused electronics through its VPT unit. One of the latest products, the VSCPL1210SG, is a power converter designed for smaller satellites. It delivers up to 10A of output with a peak efficiency of 95%, works across a wide temperature range, and has been tested for radiation, making it suitable for demanding space missions.

The company also introduced the VXR125-27000S, a higher-voltage DC-DC converter that delivers 125W of power with up to 89% efficiency. It is built to handle tough environments, with better heat management, improved shielding, and a simpler design that reduces the need for extra components. Each unit goes through a 96-hour burn-in process to ensure it can perform reliably in critical aerospace and defense systems.

Market Expectations and Forward View

HEICO is set to report its next earnings on August 24. Analysts expect $1.46 per share for the July quarter, up from $1.26 last year, marking about 16% YOY growth. That pace is expected to continue into the October quarter, with estimates at $1.52 versus $1.33 a year ago, a 14% YOY increase. For the full fiscal year ending October 2026, earnings are projected at $5.78, up from $4.90 per share and representing 18% growth.

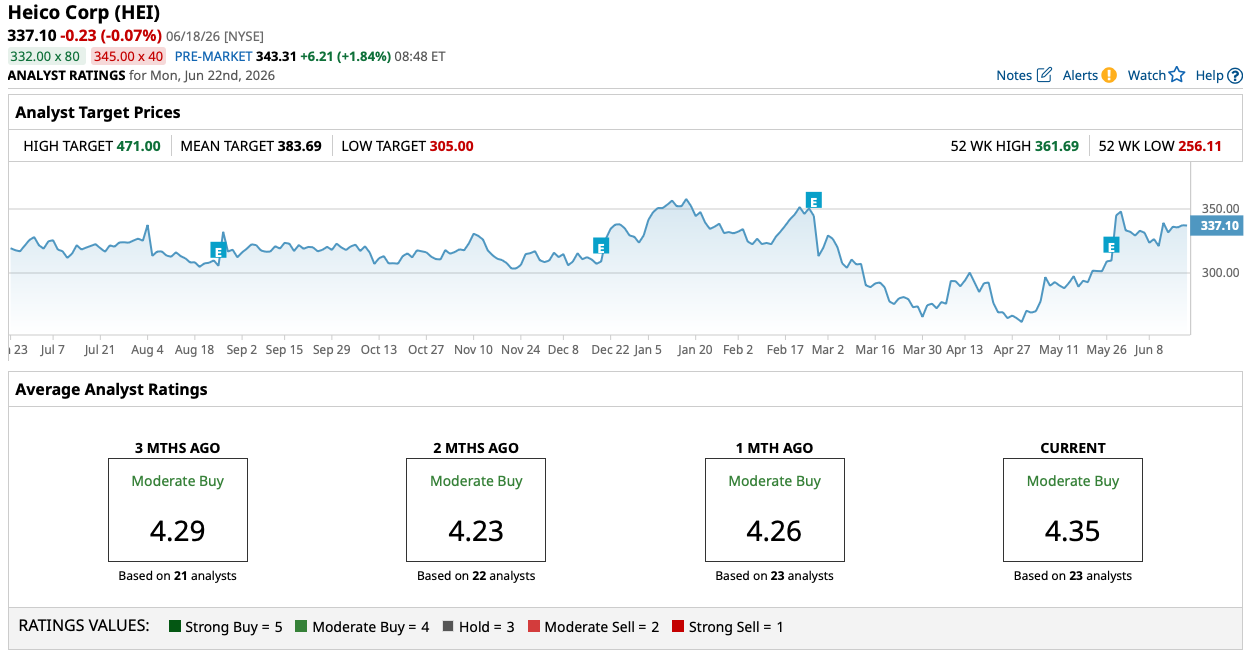

After strong Q2 results, Jefferies analyst Sheila Kahyaoglu raised her price target on HEI stock to $410 from $375 and kept a “Buy” rating, pointing to strong margins and steady execution. UBS also raised its target to $390 from $371 but kept a “Neutral” rating, taking a more cautious view that much of the good news is already reflected in HEI stock’s high valuation.

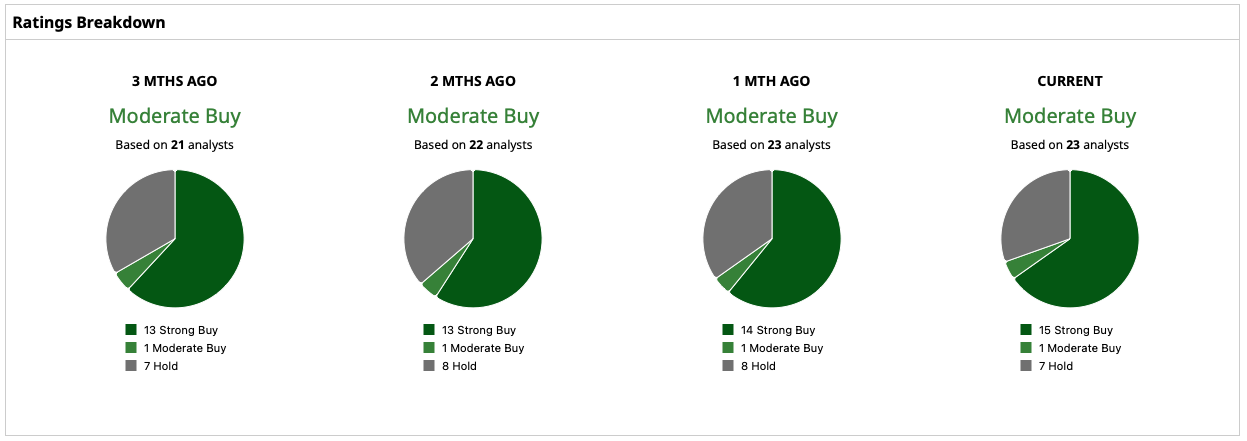

Overall, sentiment remains positive. Based on 23 analysts with coverage, HEICO has a consensus “Moderate Buy” rating with an average price target of $383.69. That suggests about 15% potential upside from current levels.

Conclusion

HEICO looks like a company that can keep rewarding shareholders, but probably not in a straight line. The business is executing at a high level, earnings are still growing at a healthy clip, and management has room to keep lifting the dividend given the very low payout ratio. That said, a lot of that strength is already reflected in the valuation, so this does not look like a clear bargain here. HEI stock will most likely trend higher over time if execution remains strong, but gains may be more measured in the near term as investors weigh premium pricing against continued growth.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)