Jack Henry & Associates, Inc. (JKHY) is a leading financial technology company headquartered in Monett, Missouri, providing core banking software, payment processing, digital banking solutions, and technology services to banks, credit unions, and financial institutions across the United States. With a focus on recurring software revenue, cloud modernization, and digital transformation, Jack Henry has built a strong position in the community banking and credit union technology market. The company has a market cap of around $9 billion.

Companies worth between $2 billion and $10 billion are generally classified as “mid-cap stocks,” and Jack Henry & Associates fits this criterion perfectly. The company is evolving constantly to help financial institutions manage transactions, lending, deposits, and customer engagement.

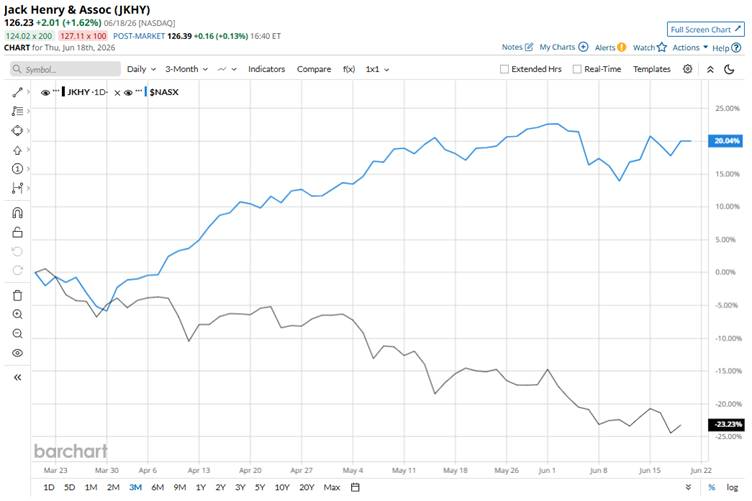

The company dipped 34.7% from its 52-week high of $193.39 recorded on Jan. 15. In addition, JKHY stock has declined 23.6% over the past three months, underperforming the broader Nasdaq Composite ($NASX), which gained 20% over the same period.

In the longer term, JKHY is down 30.8% on a YTD basis, lagging behind NASX’s 14.1% rise. Also, shares of Jack Henry & Associates have declined 30.4% over the past 52 weeks, whereas the NASDAQ has climbed 35.7% in the same period.

Moreover, the stock has been trading below the 50-day and 200-day moving averages since early February.

Jack Henry & Associates stock has declined in 2026 as investors have focused on slower long-term growth expectations and valuation compression despite continued operational strength. The company reported its fiscal Q3 2026 results on May 5, showing revenue growth of 8.7% year-over-year to $636.2 million and EPS growth of 12.2% to $1.71 compared with the prior-year quarter. However, market sentiment has weakened as investors remain cautious about future growth acceleration, margin expansion, and competition in the financial technology market.

In comparison, its rival, PayPal Holdings, Inc. (PYPL) has lagged JKHY over the past year with a 38% decline but performed better this year, with a 27.2% dip.

Among the 15 analysts covering the stock, there is a consensus rating of “Moderate Buy,” and its mean price target of $183.25 reflects an upside potential of 45.2%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)