/A%20concept%20image%20of%20space_%20Image%20by%20Canities%20via%20Shutterstock_.jpg)

Hydrogen stocks have been frustrating investors over the past few years as the once-in-demand group has struggled with execution issues and other headwinds since its rise in the clean energy boom cycle. Plug Power (PLUG), however, recently got a boost when it announced first-quarter results that show the company has made significant strides towards profitability.

While Plug remains unprofitable, it has shown signs of progress with margin improvement, better hydrogen economics, and improved liquidity. Investors have taken notice of a stock that remains about 38% off its 52-week highs thanks to these developments. Now, it's a matter of seeing if Plug can convert operational improvements into profitability.

About Plug Power Stock

Plug Power provides hydrogen fuel cell systems, electrolyzers, hydrogen production, storage, and distribution solutions. The company, headquartered in Slingerlands, New York, runs arguably one of the most well-integrated hydrogen platforms within the industry. With a market cap of roughly $3.9 billion, Plug is a prominent name in the pure-play hydrogen space.

Over the last year, shares of PLUG have seen wild swings as the stock is up nearly 175% from its 52-week lows around $1.03 yet off over 38% from its 52-week highs near $4.58. Even with the rally, the stock is still far underperforming broader market measures despite recent news from the company.

At the current price levels, valuation is up for debate as PLUG stock trades at about 5.5x sales and 5x book. While that seems relatively high for a company posting significant losses, investors are valuing the company for its platform and future growth potential in hydrogen projects. Currently, metrics like profitability are weak with a return on equity of negative 49.3% and a profit margin of negative 229.8%.

Plug Power Beats on Earnings

For the first quarter, Plug delivered better-than-expected performance with revenues increasing 22% from the prior year quarter to $163.5 million. During the period, Plug beat its revenue guidance and achieved its margin and adjusted EPS goals.

One of the most positive developments from Plug was the significant improvements in its profit metrics. Plug's GAAP gross margin was negative 13%, which was down from negative 55% for the prior year quarter. This 42 percentage point improvement was due to strong sales volumes, cost savings, better execution in servicing, and fuel savings. The company's adjusted EPS decreased to a loss of $0.08 per share compared to a loss of $0.17 per share from the year-ago quarter.

Going forward, management is focused on hitting its goal of achieving positive EBITDAS in the fourth quarter of 2026. In terms of operations, Plug continues to make progress in its material handling, electrolyzers, and hydrogen production segments. Notably, the company continues to expand its customer base with companies such as Amazon and Walmart. Service costs per GenDrive unit were down more than 30% year-over-year (YoY) as well.

Electrolyzer capacity is continuing to grow for the company, with Plug deploying over 320 megawatts of electrolyzer capacity globally. Additionally, Plug estimates that its opportunity pipeline stands at greater than $8 billion. Some recent highlights for Plug's electrolyzer platform included deployments such as 100 MW to Galp Energia in Portugal, 25 MW to Iberdrola and BP in Spain, and a 275 MW front-end engineering design award to Hy2gen in Canada.

In terms of liquidity, PLUG saw a significant boost in this area as the company finished the first quarter with greater than $802 million in total cash. Looking forward, management says the company will generate additional cash from asset monetization projects worth around $275 million related to hydrogen project activity. In addition, management believes cash usage will trend modestly ahead of expectations.

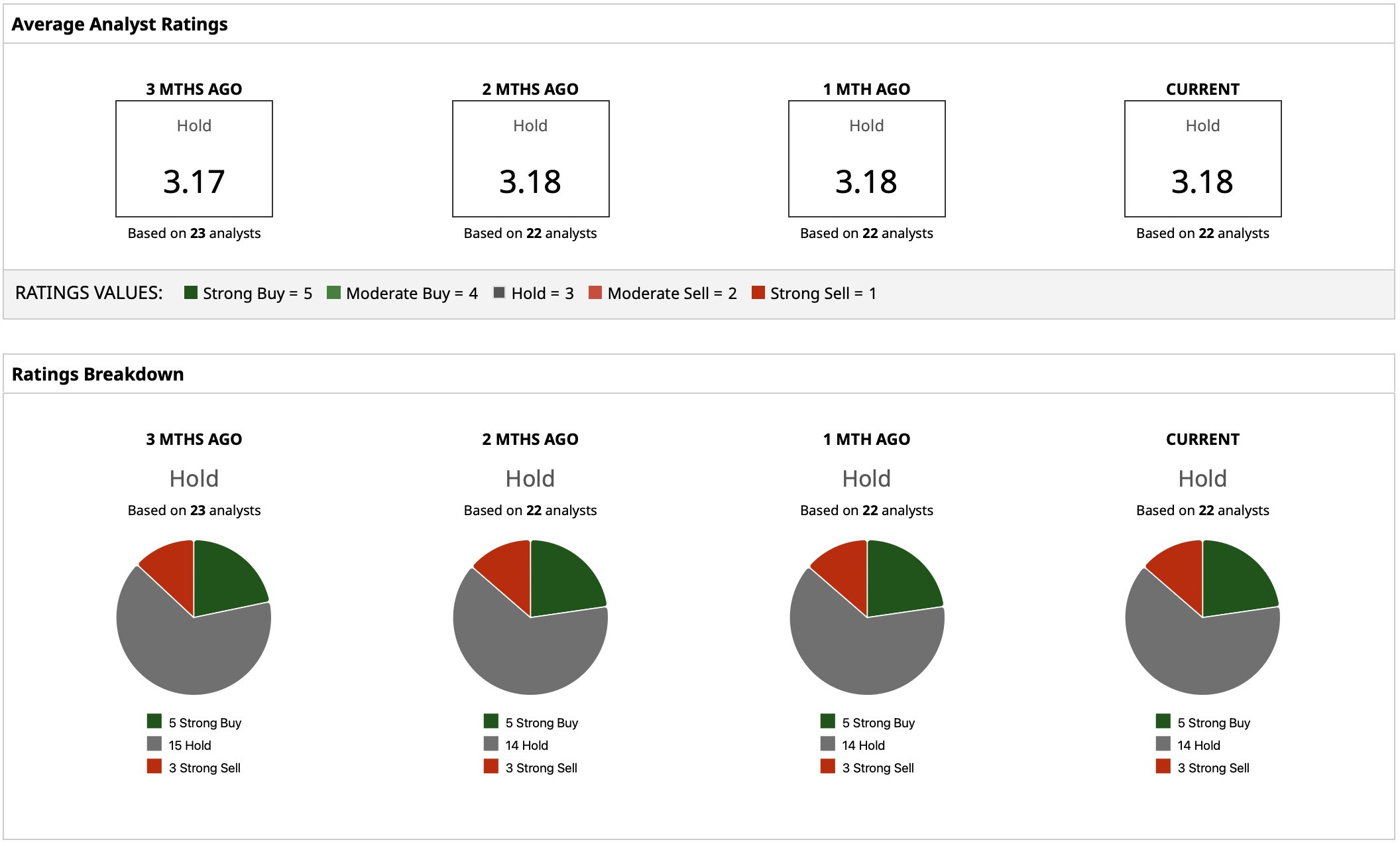

What Do Analysts Say About PLUG Stock?

Analysts are neutral about PLUG stock with a "Hold" rating consensus. The mean target of $3.52 represents a potential upside of roughly 22%. Additionally, some analysts see upside of more than 140% with a Street-high target of $7. Meanwhile, the lowest analyst target of $0.75 indicates how much uncertainty there remains over Plug's ability to turn a profit. Plug has shown margin improvements, improved hydrogen economics, and an expanding opportunity pipeline as reasons for optimism going forward. The focus going forward remains on hitting its goal of positive EBITDAS in the fourth quarter of 2026.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.