With a market cap of $24.9 billion, VeriSign, Inc. (VRSN) is a global provider of internet infrastructure and domain name registry services that enable reliable navigation across widely used domain names. The company operates critical internet functions, including maintaining two of the thirteen root servers and providing registration and authoritative resolution for .com and .net domains that power global e-commerce.

Companies valued at $10 billion or more are generally considered "large-cap" stocks, and VeriSign fits this criterion perfectly. VeriSign also manages directories such as .name and .cc and supports back-end systems for domains like .edu.

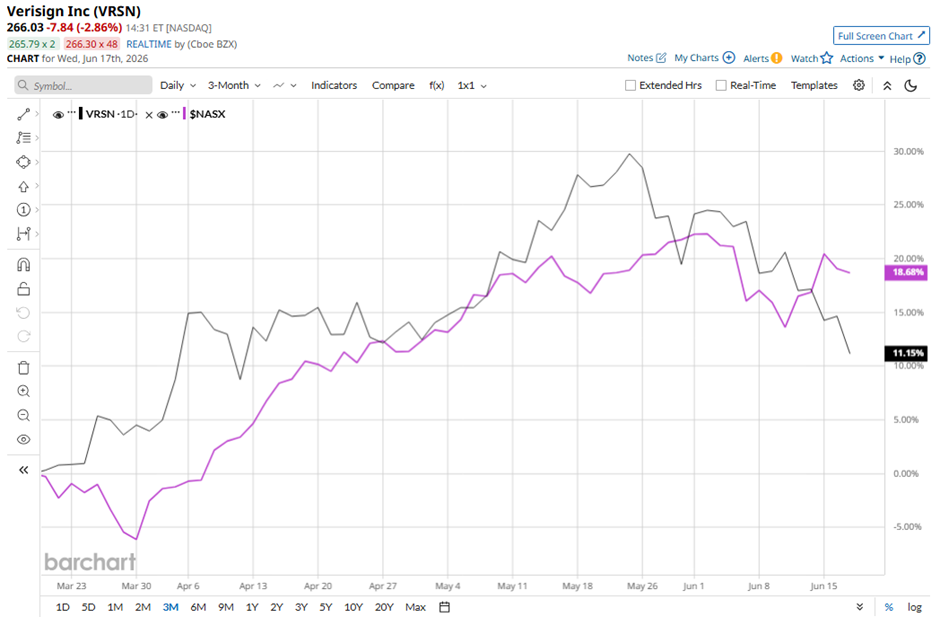

Shares of the Reston, Virginia-based company have fallen 14.8% from its 52-week high of $312.48. Over the past three months, its shares have gained 9.9%, lagging behind the broader Nasdaq Composite’s ($NASX) 17.4% increase during the same period.

VRSN stock is up 9.6% on a YTD basis, underperforming NASX's 13.6% rise. However, shares of VeriSign have declined 6.3% over the past 52 weeks, compared to NASX’s 35.2% return over the same time frame.

The stock has been trading below its 200-day moving average since late July 2025.

VeriSign reported strong Q1 2026 results on Apr. 23 with revenue rising 6.6% year-over-year to $429 million, while net income increased to $215 million and EPS improved to $2.34. The company also delivered solid operational growth, as .com and .net domain registrations increased 3.7% year-over-year to 176.1 million, new registrations climbed to 11.5 million, and the renewal rate improved to 75%. However, the stock fell 2.8% the next day.

In comparison, rival Oracle Corporation (ORCL) has shown a less pronounced decline than VRSN stock on a YTD basis, with ORCL shares decreasing 2.8%. However, ORCL stock has dropped 9% over the past 52 weeks, lagging behind VRSN stock.

Despite the stock’s underperformance relative to the Nasdaq over the past year, analysts remain moderately optimistic about its prospects. VRSN stock has a consensus rating of “Moderate Buy” from four analysts in coverage, and the mean price target of $320 suggests a premium of 20.3% to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Corning%20Incorporated%20on%20screen%20in%20front%20of%20website%20By%20Timon.jpeg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)