/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

Advanced Micro Devices (AMD) stock climbed almost 5% on June 12 and nearly 7% on June 15 after a major Wall Street firm made a bold call on AMD stock. Specifically, Citi analyst Atif Malik raised his rating on AMD from “Neutral” to “Buy” and lifted his price target to $575 from $460, according to a note to clients. Valued at a market capitalization of $827 billion, AMD currently trades near $523 per share.

The Citi upgrade points to two big things happening at AMD right now. For one, the company is gaining serious ground in the graphics processing unit (GPU) market. Meanwhile, its central processing unit (CPU) business is among the most important growth stories in tech.

Why AMD's GPU Business Is Finally Getting the Credit It Deserves

For a long time, most investors looked at AMD as a CPU company with a GPU business on the side. However, in an investor note, Malik explained that AMD is now emerging as a credible second source in the GPU market. The analyst added that the company is on track to capture the “lion's share” of GPU sales at Meta Platforms (META), which represents a potentially massive revenue stream.

In May, AMD CEO Lisa Su confirmed on the first-quarter 2026 earnings call that the chipmaker has an expanded strategic partnership with Meta to deploy up to 6 gigawatts of Instinct GPUs across multiple product generations. A custom GPU accelerator built on the MI450 architecture is also being co-designed for Meta's next-generation AI workloads. Shipments are expected to begin in the second half of 2026.

Moreover, AMD has a partnership with OpenAI. Together, both customers are tracking above AMD's original plan for 2027, as CFO Jean Hu noted at the Bank of America Global Technology Conference on June 2. "Both are coming higher than our original plan," Hu said.

The Helios rack-scale platform, which pairs AMD's Instinct GPUs with its EPYC Venice CPUs, is the delivery vehicle for these deployments. AMD says it has already sampled the MI450 GPU to lead customers and has full Helios racks running in some customer data centers today.

AMD's CPU Boom Is Rewriting the Playbook for AI Infrastructure

The CPU side of AMD's business is where Malik's upgrade gets especially interesting. Citi raised its forecast for the server CPU total addressable market (TAM) to $137 billion by 2030, up from its previous $132 billion estimate. That lines up closely with what AMD management said publicly on its earnings call. In May, AMD raised its own server CPU TAM forecast to more than $120 billion by 2030.

The key driver of this growth is agentic artificial intelligence. When AI stops just answering questions and starts performing tasks autonomously, it requires much more CPU power. Every step an AI agent takes — whether it is pulling from a database, coordinating with another agent, or post-processing a result — requires CPU compute. That is driving demand for AMD's EPYC server chips at a pace almost nobody anticipated.

AMD reported that server CPU revenue grew more than 50% year-over-year (YOY) in Q1 2026. The company also guided for more than 70% YOY growth in Q2. Much of that growth is coming from selling more units. "What we are seeing is very significant and incremental demand for our CPU platforms," Hu said at the BofA conference. "That has been really exciting."

AMD's sixth-generation EPYC Venice processor, built on 2-nanometer technology, is designed to extend the lead. It includes a CPU purpose-built for AI infrastructure for the first time, and AMD says more customers are validating Venice at this stage than “any prior EPYC generation.”

Malik noted that AMD benefits from its performance leadership, higher core counts, the x86 instruction set architecture, a broader range of product configurations, and support for both multithreaded and single-threaded workloads. Those advantages make AMD well-positioned to stay ahead as the CPU market scales.

What the AMD Upgrade Means for Investors

Citi's price target of $575 implies meaningful potential upside from current levels. Malik's view is that most investors are still undervaluing AMD's GPU potential. The analyst estimates the market is pricing in roughly a 60% probability that AMD hits more than $50 billion in GPU revenue by 2028. If the company executes on the Meta deal and continues to broaden its customer base, that probability could rise quickly.

AMD's free cash flow tripled YOY to a record $2.6 billion in Q1 2026. The data center segment, which covers both EPYC and Instinct products, generated $5.8 billion in revenue in the quarter, up 57% YOY.

Analysts tracking AMD stock forecast revenue to increase from $34.6 billion in 2025 to $117 billion in 2029. In the same period, adjusted earnings are projected to expand from $4.17 per share to more than $20 per share.

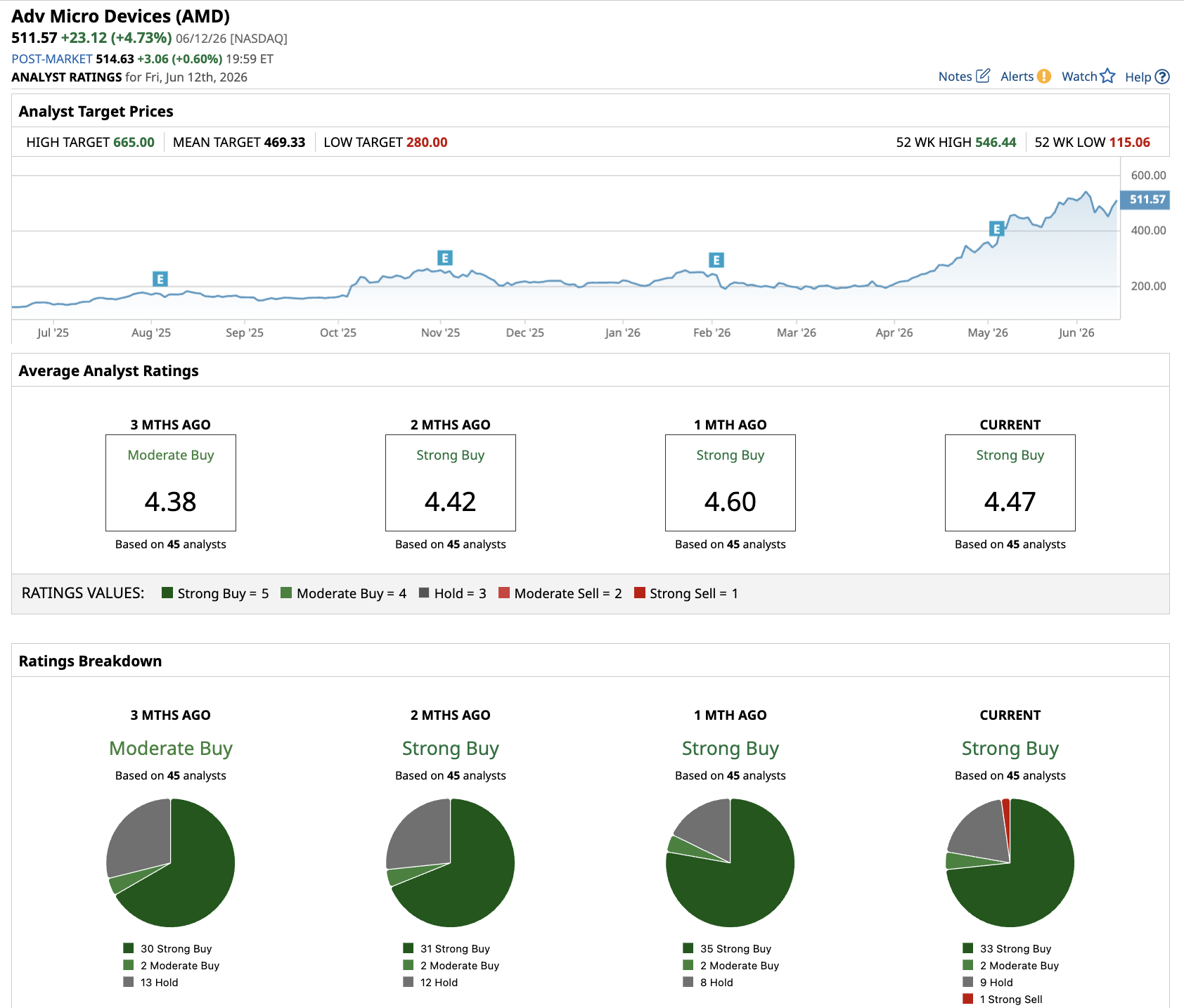

Out of the 45 analysts covering AMD stock, 34 recommend a “Strong Buy” rating, two recommend a “Moderate Buy,” eight recommend a “Hold” rating, and one analyst recommends a “Strong Sell." The average price target of $472.07 has already been surpassed by shares, while the highest price target of $665 suggests potential upside of 27% from here.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)