/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

Palantir Technologies (PLTR) has come a long way from its roots as a post-9/11 intelligence software provider. Today, the company sits at the center of the artificial intelligence (AI) boom, helping governments and businesses use data to make faster, smarter decisions through its Artificial Intelligence Platform (AIP). That transformation turned Palantir into one of Wall Street’s hottest AI stocks and fueled a massive rally in 2025.

But 2026 has been a different story.

Despite reporting record revenues, raising guidance for the year, and telling investors that demand remains stronger than the company can currently handle, PLTR stock has fallen 24.44% this year. The disconnect comes down largely to valuation. After last year’s explosive run, expectations became sky-high, leaving little room for anything short of exceptional execution.

Investors are also watching for potential cracks, including slower international growth, uncertainty around some government contracts, and the challenge of maintaining rapid expansion as the company gets larger. Even after the sell-off, many believe the stock still reflects years of near-perfect growth.

So, with the business still growing at a remarkable pace but the stock moving in the opposite direction, what will it take for Palantir’s shares to regain their momentum?

About Palantir Stock

Denver-based Palantir Technologies, founded in 2003, began to support national security through smarter data. Fast forward, and it now powers decision-making across governments and industries through Gotham, Foundry, and its newest force multiplier, the AIP, launched in 2023. This is not just software, but strategic infrastructure. Palantir enables institutions across four continents to transform fragmented data into operational clarity and action. With a market cap of $306.8 billion, it is a software titan in the large-cap arena.

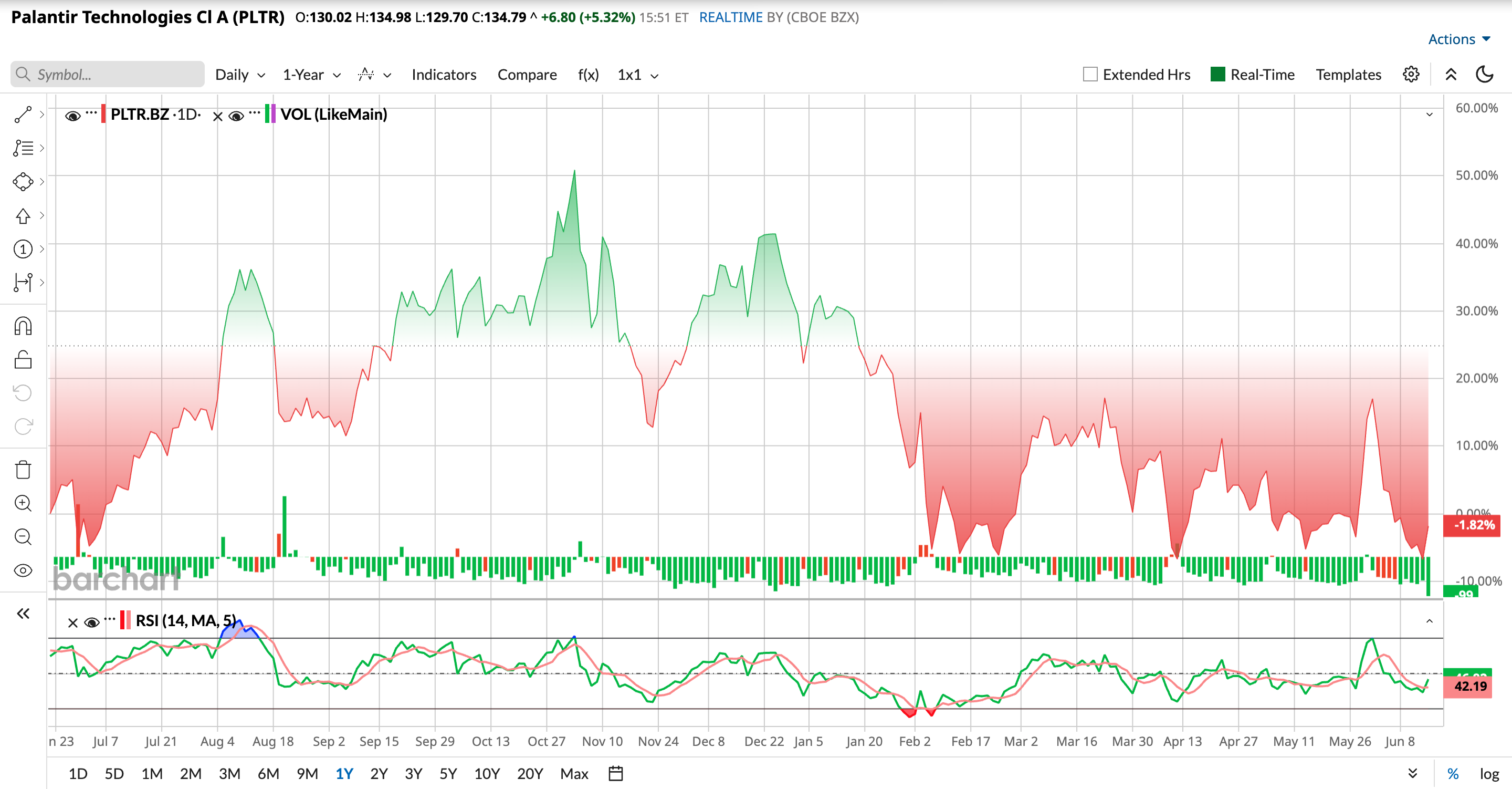

Palantir shareholders have experienced a very different ride in 2026 than they did in 2025. After soaring to a 52-week high of $207.52 last November as enthusiasm around AI reached a fever pitch, the stock has steadily lost altitude. Shares are now down 35.18% from that peak and touched a 52-week low of $122.68 in April.

The recent trend hasn't been much better. PLTR has fallen 10.97% over the past three months and another 1.53% over the last five trading sessions, reflecting growing investor caution. The irony is that the sell-off hasn't been driven by weak business performance. Palantir continues to post record revenue growth and raise guidance. Instead, investors are questioning whether the company's premium valuation can be justified over the long run.

Concerns about slowing international growth, uncertainty surrounding the renewal of its U.K. National Health Service contract, and the challenge of maintaining extraordinary growth rates as the business scales have weighed on sentiment. Add in concerns about inflation, geopolitical tensions, and a more cautious market environment, and it is easier to understand the reasons that investors have taken some money off the table.

Technically, the 14-day RSI sits at 46.41, suggesting the stock is nearing oversold territory, a level where selling pressure often begins to ease, and buyers start looking for opportunities.

Palantir’s rally has been remarkable, but the stock still carries a hefty price tag. Even after its recent pullback, PLTR trades at 86.91 times forward earnings and 39.74 times sales, well above most software peers. In other words, investors are betting on years of strong AI-driven growth.

Palantir’s government relationships, growing commercial business, and strong balance sheet support that optimism, but the valuation leaves little room for any slowdown or misstep.

A Snapshot of Palantir’s Q1 Numbers

Palantir started 2026 with another blockbuster quarter, showing that demand for its AI software remains stronger than ever. The company reported first-quarter results on May 4, beating Wall Street’s expectations and continuing a growth streak that has been building momentum for the past couple of years.

Revenue climbed to a record $1.63 billion, up 85% year-over-year (YOY). Even more impressive, this marked Palantir's eleventh straight quarter of accelerating revenue growth, a rare achievement for a company of its size. The main driver continues to be its Artificial Intelligence Platform (AIP), which is attracting both government agencies and corporate customers looking to deploy AI at scale.

The U.S. business was the standout performer. Revenue from the U.S. jumped 104% YOY, as more organizations turned to Palantir’s software to improve operations and decision-making. The commercial segment was particularly strong, with revenue surging 133% annually. At the same time, Palantir’s government business continued firing on all cylinders, with U.S. government revenue rising 84% YOY to $687 million thanks to new contracts and expanding relationships.

The company’s customer base is also growing rapidly. Total customers increased 31% YOY to 1,007. Existing clients are spending more as well. Palantir’s top 20 customers generated an average of $108 million per customer in trailing 12-month revenue, up 55% annually. Meanwhile, net dollar retention reached 150%, showing that customers are significantly expanding their use of the platform after signing up. Meanwhile, total contract value bookings soared 135% YOY, providing strong visibility into future revenue growth.

Profitability remained another bright spot. Adjusted EPS came in at $0.33, ahead of analyst estimates. Operating cash flow nearly tripled from a year ago to $899 million, while the company ended the quarter with $2.3 billion in cash and no short-term debt. Those numbers highlight not only strong growth but also a business that is generating substantial cash.

Looking ahead, management clearly sees the momentum continuing. Q2 revenue is expected to be between $1.797 billion and $1.801 billion. Full-year 2026 revenue guidance was raised and expected to range from $7.65 billion to $7.662 billion – $7.656 billion at midpoint – up from its previous outlook, implying roughly 71% annual growth.

Furthermore, the company boosted its forecast for U.S. commercial revenue to more than $3.224 billion, representing growth of at least 120%. Adjusted operating income is now expected to be between $4.44 billion and $4.452 billion, while adjusted FCF is projected between $4.2 billion and $4.4 billion.

Overall, Palantir’s accelerating growth, expanding customer base, rising spending from existing clients, strong cash generation, and higher guidance all point to the fact that demand for its AI platform remains exceptionally strong, helping support the premium valuation investors continue to assign to the stock.

Meanwhile, analysts tracking Palantir expect the company’s fiscal 2026 EPS to be around $1.18, up 87.3% annually, and rise by another 42.4% YOY to $1.68 in fiscal 2027.

What Do Analysts Expect for Palantir Stock?

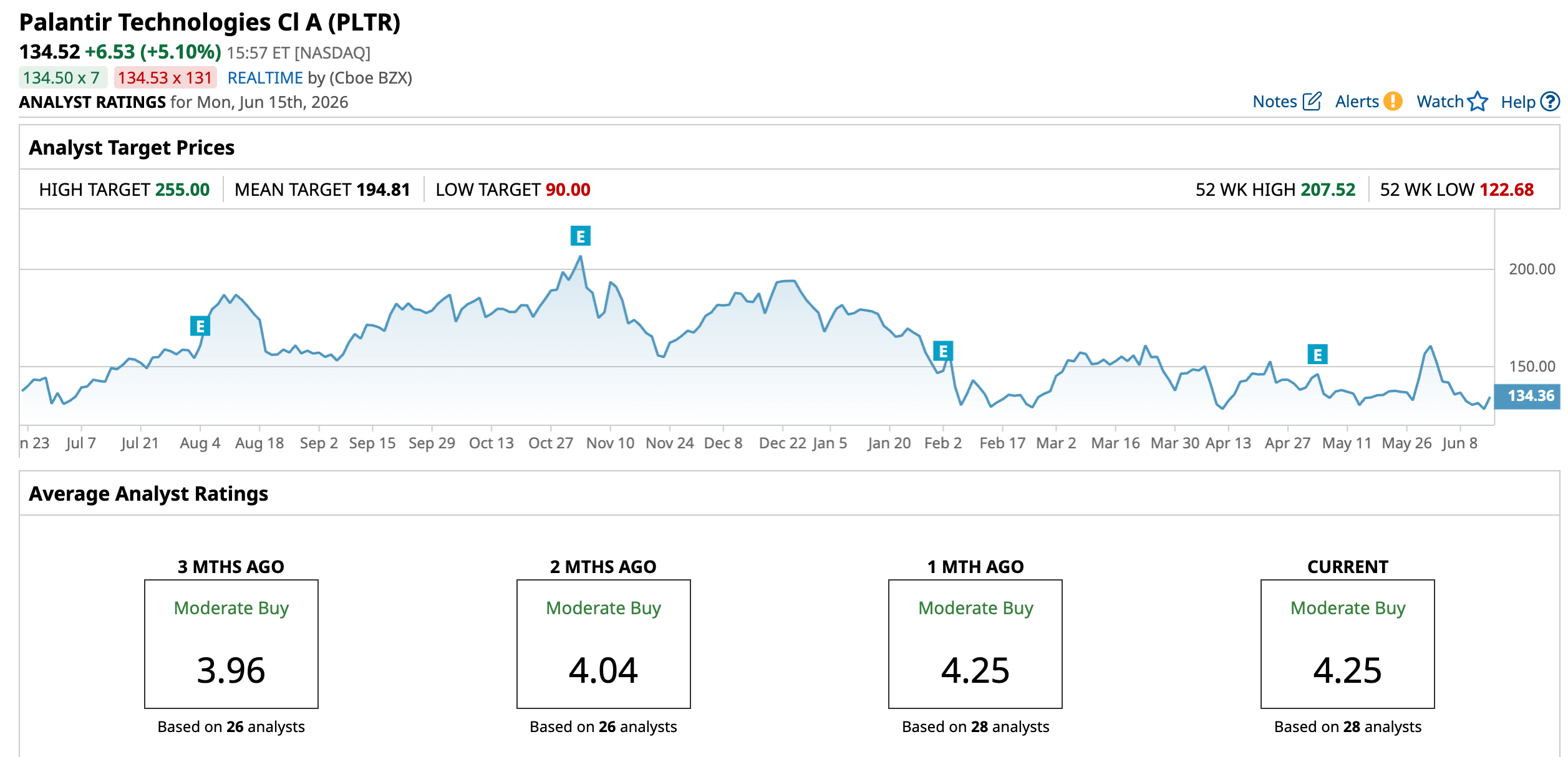

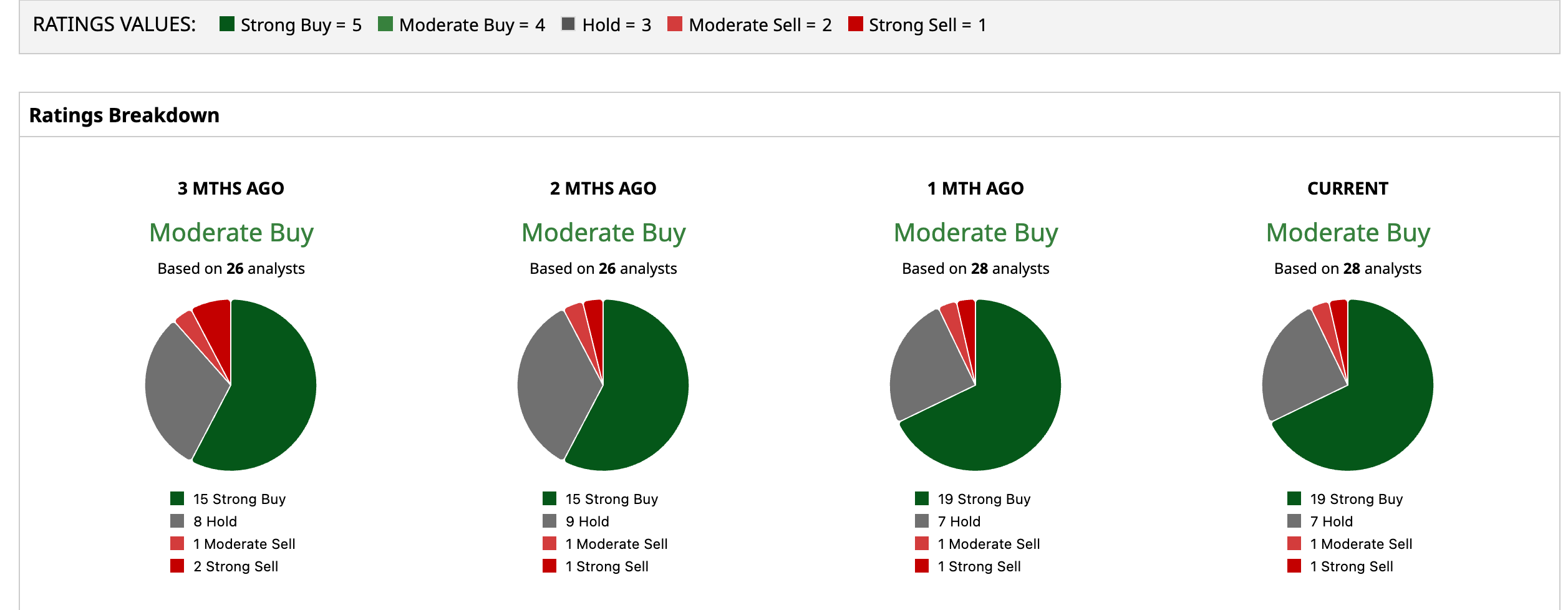

Wall Street remains split on Palantir, though optimism still has the upper hand. Bulls point to the company’s growing AI momentum, while skeptics warn about valuation concerns. Overall, analysts rate PLTR a “Moderate Buy.” Of the 28 analysts offering recommendations, 19 advise a “Strong Buy,” seven analysts play it safe with a “Hold,” one leans slightly bearish with a “Moderate Sell,” while the remaining one goes fully pessimistic with a firm “Strong Sell.”

PLTR’s average analyst price target of $194.81 implies the tech stock has an upside potential of 44.8%. The Street-high target of $255 signals that PLTR can still rise as much as 89.6% from current levels.

Conclusion

So, what does Palantir need to turn things around? In many ways, the answer is to keep doing what it is already doing. The company continues to grow at an exceptional pace, demand for its AI platform remains strong, and its financial results keep exceeding Street’s expectations. The bigger challenge is convincing investors that the stock’s valuation can still be justified as the company gets larger.

The good news is that much of the excess optimism has already been wrung out of the shares. If confidence returns to growth stocks and Palantir continues delivering beat-and-raise quarters, the stock could regain its footing. But even if the recovery takes time, the long-term story remains intact. For now, investors will be watching closely to see whether Palantir's powerful business momentum can once again outweigh concerns about valuation and market sentiment.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)