Oklo (OKLO) is still a stock built more on promise than profits. That is the appeal. The company is trying to build advanced fast-fission reactors, recycle nuclear fuel, and create a domestic isotope supply chain. That is a big idea — and exactly why OKLO stock keeps getting attention even while the business is still early.

Recently, the company got a major breakthrough related to the U.S. Department of Energy (DOE), which could be its next catalyst.

Over the past year, the move in OKLO stock has been wild. Despite a bull run in the second half of 2025, shares have plunged throughout 2026 and are now down 15% on a year-to-date (YTD) basis.

The pullback makes sense. Investors are digesting a huge 2025 run, a pre-revenue business model, and a lot of cash burn. The chart still looks tired after that reset, so the stock does not have the feel of a clean technical breakout right now.

Why the DOE Milestone Matters for Oklo Stock

The big news on June 11 was simple but important: The U.S. Department of Energy’s Idaho Operations Office approved the Preliminary Documented Safety Analysis (PDSA) for Oklo’s Aurora powerhouse at the Idaho National Laboratory. That is another real step forward for a company that still needs to turn licensing wins into operating assets.

The market liked the news. Oklo shares rose in premarket trading and ended the day up by 7%.

This news matters because a safety review is one of the gates that can slow down a nuclear startup for years. Every approval chips away at the “someday” label. Oklo CEO Jacob DeWitte called the approval an “important milestone” and noted that it ”helps establish a foundation for future Aurora deployments." That is the real story here. Investors are not buying current earnings. They are buying lower risk on a path to commercialization.

The Numbers Still Tell a Very Early-Stage Story

Oklo still looked like a company in build mode in its latest quarter. For the first quarter of 2026, the company reported no revenue. Net loss widened to $33.1 million, or $0.19 per share, from $9.8 million, or $0.07 per share, a year earlier. Oklo also said that cash used in operating activities was $17.9 million, while it spent $32.8 million on property and equipment. That makes free cash flow deeply negative, though the company still had a strong balance sheet.

The cash picture is the part that keeps people interested. Oklo finished the quarter with $1.59 billion in cash and cash equivalents and $614.5 million in marketable debt securities. Management also expects to use $80 million to $100 million in operating cash this year and invest $350 million to $450 million in property, plant and equipment. In other words, the company is spending aggressively to get ready for the future. Analysts expect loss per share to widen to about $0.19 in the June quarter and widen to about $0.78 for full-year fiscal 2026.

Valuation is where the story gets uncomfortable. On EV to EBITDA, Oklo is still negative, so the multiple is not very helpful in a normal way. Meanwhile, the sector median is about 12.5 times. With the company still pre-revenue, OKLO is not cheap, sporting the kind of valuation that assumes a long runway and a lot of execution.

What Oklo Is Doing Next, and What Analysts Think

Oklo is trying to turn momentum into something bigger in 2026. The company is still aiming to bring Aurora online around late 2027 or early 2028. It has also won its first Nuclear Regulatory Commission (NRC) license for Atomic Alchemy, which could open a separate isotope revenue stream. Oklo has major partnerships hanging over the story as well, including a Meta Platforms (META) agreement to prepay for nuclear power at a planned Ohio site plus a collaboration with Nvidia (NVDA) and the Los Alamos National Laboratory. That gives Oklo more than one shot at becoming a real business.

Wall Street is still constructive, even if it is not blindly bullish. Earlier this year, Citi cut its target to $73.50 and kept a “Neutral” rating. BofA has been more upbeat at points, currently offering an $80 price target and “Buy” rating. Meanwhile, Seaport set a $150 target in December 2025.

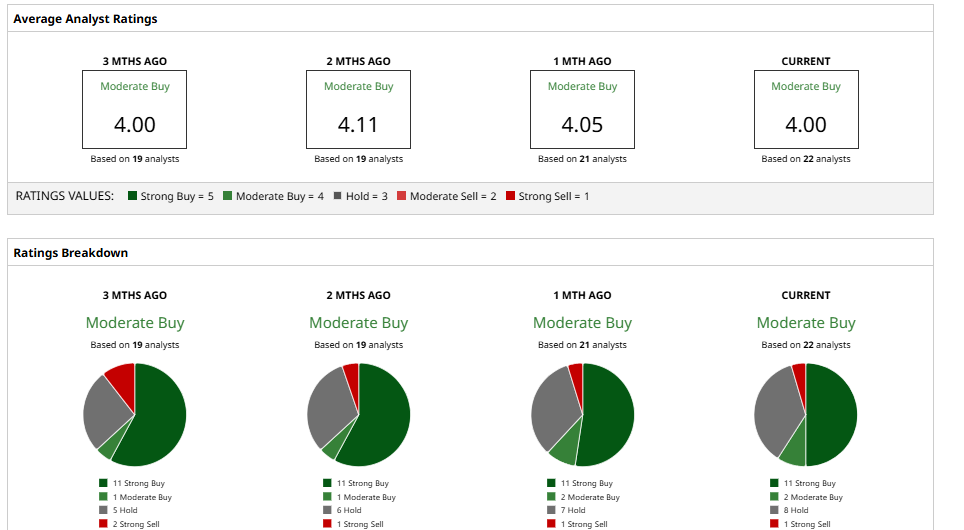

Across the Street, analysts still lean optimistic. Based on 22 analysts with coverage, OKLO stock has a consensus “Moderate Buy” rating. The average price target of $85.42 suggests potential upside of about 40% from current levels. That says the market still sees upside but that OKLO also has plenty to prove.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)