The Williams Companies, Inc. (WMB), headquartered in Tulsa, Oklahoma, operates as an energy infrastructure company focused on connecting North America's hydrocarbon resource plays to growing markets for natural gas, natural gas liquids (NGLs), and olefins. With a market cap of $87.5 billion, the company owns and operates midstream gathering and processing assets, and interstate natural gas pipelines.

Companies worth $10 billion or more are generally described as “large-cap stocks,” and WMB perfectly fits that description, with its market cap exceeding this mark, underscoring its size, influence, and dominance within the oil & gas midstream industry. WMB’s strategic strength stems from its robust asset portfolio, featuring key pipeline systems like Transco and Northwest. Strategic acquisitions have expanded its capacity and reach, solidifying its position as a leading midstream player.

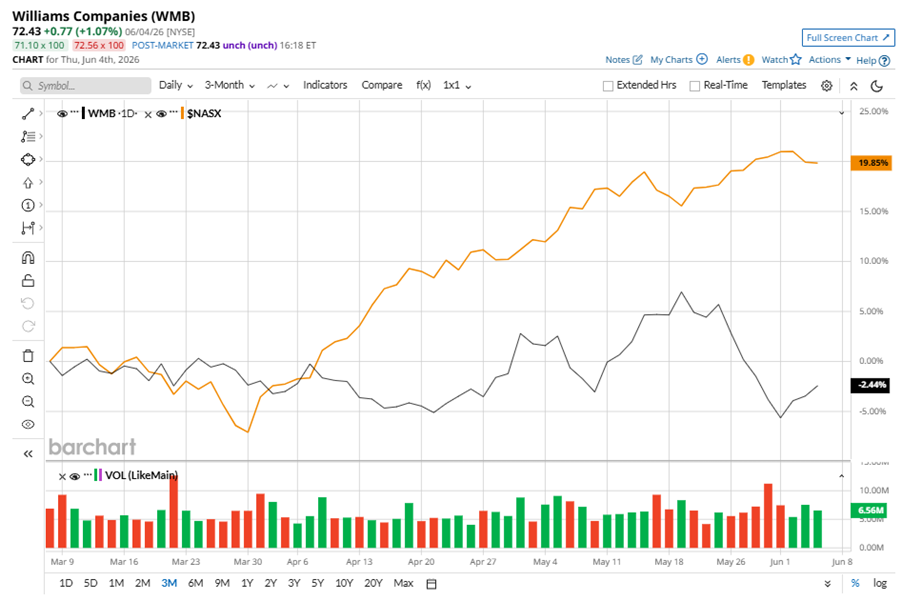

Despite its notable strength, WMB slipped 9.6% from its 52-week high of $80.08, achieved on May 20. Over the past three months, WMB stock declined 4.4%, underperforming the Nasdaq Composite’s ($NASX) 17.6% gains during the same time frame.

Shares of WMB have climbed 20.5% on a YTD basis, outperforming NASX’s YTD gains of 15.4%. However, in the longer term, the stock rose 20.5% over the past 52 weeks, underperforming NASX’s 37.9% returns over the same time frame.

To confirm the bullish trend, WMB has been trading above its 200-day moving average over the past year, with some fluctuations. However, the stock is trading below its 50-day moving average since late May.

On May 4, WMB shares closed down marginally after reporting its Q1 results. Its adjusted EPS of $0.73 beat Wall Street expectations of $0.65. The company’s revenue was $3 billion, falling short of Wall Street forecasts of $3.3 billion. WMB expects full-year adjusted EPS in the range of $2.20 to $2.38.

WMB’s rival, Kinder Morgan, Inc. (KMI) shares lagged behind the stock, with a 15.3% uptick on a YTD basis and 13.1% gains over the past 52 weeks.

Wall Street analysts are bullish on WMB’s prospects. The stock has a consensus “Strong Buy” rating from the 23 analysts covering it, and the mean price target of $84.14 suggests a potential upside of 16.2% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.