/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

The artificial intelligence (AI) boom is opening new doors for Arm Holdings plc (ARM), turning what was once a pure Intellectual Property (IP) licensing powerhouse into an increasingly important player in the chip market. Arm appears poised to cash in sooner than expected as technology giants continue to pour billions into data centers and AI infrastructure.

Chief Executive Officer Rene Haas recently suggested that Arm could reach its $15 billion target for in-house chip sales ahead of schedule. The forecast reflects stronger-than-anticipated demand from companies racing to secure the computing power needed to support the next wave of AI applications.

Haas said he remains "very confident" that Arm can achieve the goal by the end of the decade. Speaking on Tuesday, June 2, he noted that current industry trends point to an even faster path. A fierce scramble to build AI services and expand data center capacity has created a demand environment that continues to exceed expectations.

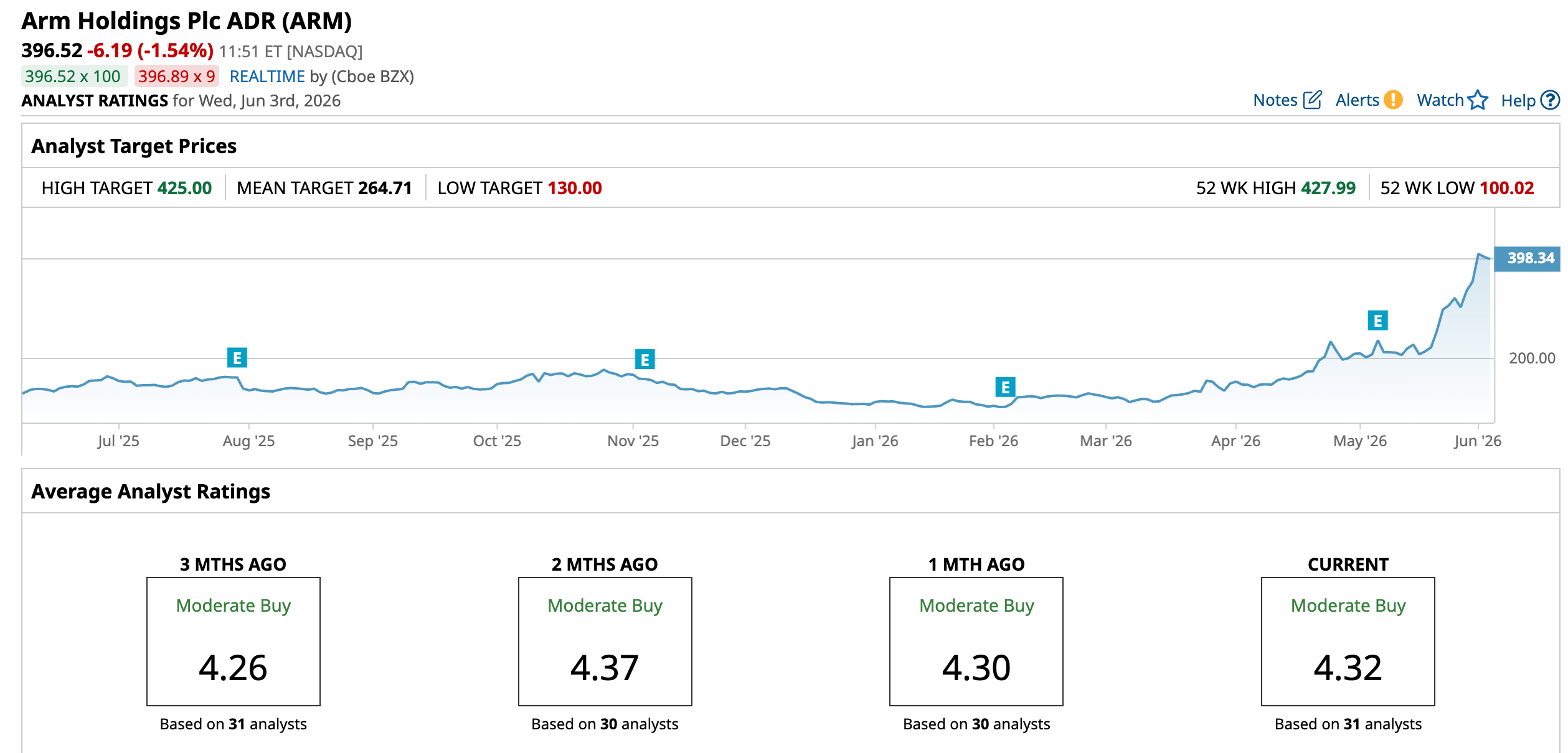

On this account, ARM stock, which had already gained 264.13% year-to-date (YTD), climbed to a new 52-week high of $427.99 on June 2 after the comments surfaced. With AI demand running hotter than expected, that destination may now be much closer than it first appeared.

About Arm Stock

Based in Cambridge, United Kingdom, Arm Holdings develops and licenses processor architectures and related IP, enabling chips used in smartphones, cloud computing, automotive systems, and industrial devices.

Commanding a market cap of nearly $425.5 billion, it supplies compute platforms, system designs, and development tools that semiconductor firms and technology manufacturers use to build energy-efficient, high-performance hardware across global markets.

ARM stock has put up a gain of 209.1% in the past 52 weeks, which would already be enough to make most stocks blush. What is even more impressive is that the shares gained 227% in the last three months alone.

Zooming in further, the stock has skyrocketed 31.49% across just the past five trading sessions, showing that the momentum here is not cooling off but actively picking up speed with every passing week.

The valuation reflects the amount of conviction the market has poured into this name. ARM stock is currently trading at 185.81 times forward adjusted earnings and 72.09 times sales, with both figures sitting well above industry averages and signaling that investors are paying a serious premium to own it.

A Closer Look at Arm’s Q4 Earnings

Arm Holdings stepped up to the plate on May 6 and delivered Q4 FY2026 results that set the highest quarterly revenue record in the company's history. The top line grew 20.1% year-over-year (YOY) to $1.49 billion.

Licensing revenue surged 29.2% YOY to $819 million, fueled by strong platform demand. Royalty revenue climbed 10.5% to $671 million, drawing on momentum across Edge AI, physical AI, and cloud AI, with data center royalties more than doubling YOY in that window.

The results pushed non-GAAP EPS to a record $0.60, all while the company continued to pump up its R&D investment. On to the balance sheet, Arm closed the quarter with $2.8 billion in cash and cash equivalents as of March 31.

Looking forward, Arm has set Q1 FY2027 revenue guidance at $1.26 billion, plus or minus $50 million, which at the midpoint works out to revenue growth of about 20% YOY. Both royalty revenue and license and other revenue should each post growth of around 20% YOY, and non-GAAP EPS guidance sits at $0.4, plus or minus $0.04.

Arm is also painting the full picture for investors willing to look further down the road. By FY2031, the company projects $15 billion in AGI CPU revenue running alongside $10 billion in IP revenue, stacking up to $25 billion in total annual revenue.

Analyst forecasts are pointing in the same direction. The Street expects Q1 FY2027 EPS to grow 12.5% YOY to $0.18. For the full FY2027, analysts project bottom line growth of 30.2% YOY to $1.12, and FY2028 projections push the number further, calling for EPS growth of 77.7% all the way up to $1.99.

What Do Analysts Expect for Arm Stock?

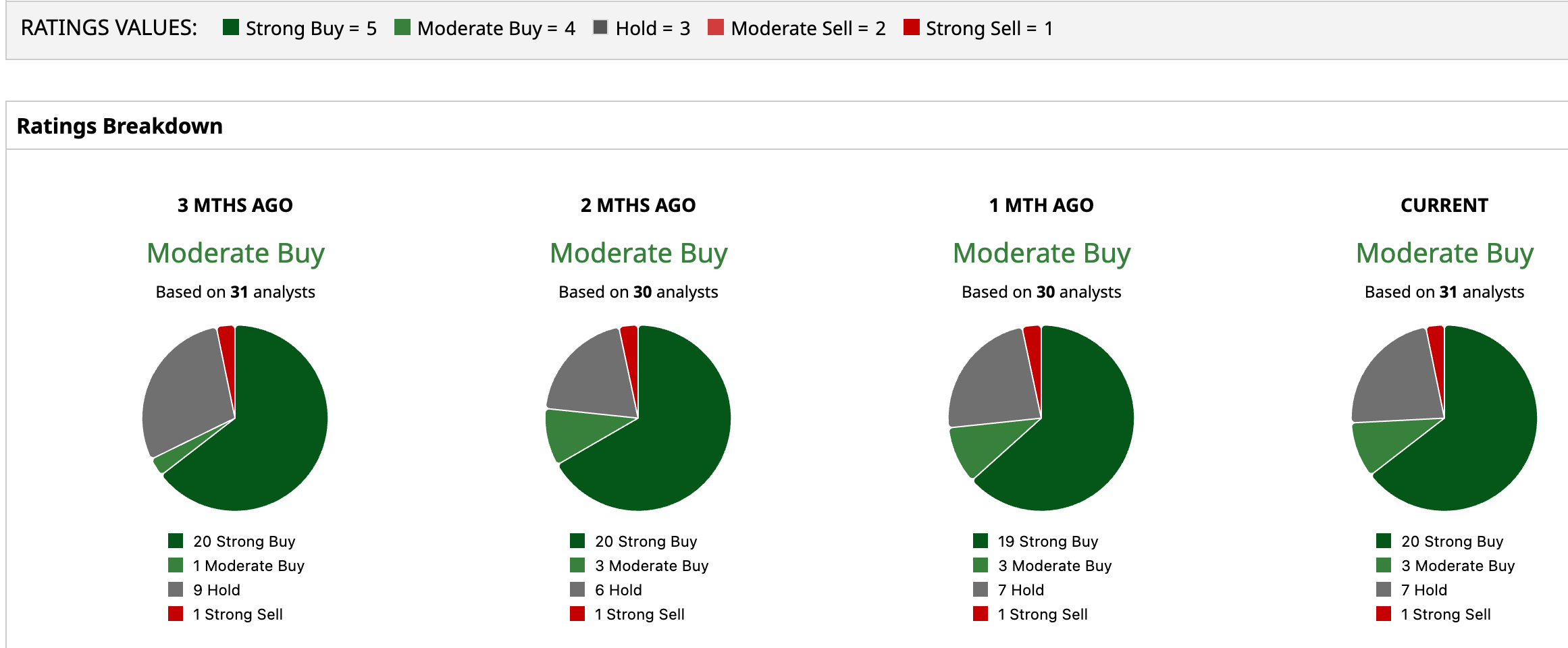

Wall Street has settled on an overall "Moderate Buy" rating for ARM stock. Out of 31 analysts covering the name, 20 are pounding the table with a "Strong Buy," three are calling it a "Moderate Buy," seven are sitting on "Hold," and one lone holdout is waving a "Strong Sell" flag.

ARM stock is already trading above the average price target of $264.71, but the Street-High target of $425 suggest a gain of 7.18% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)