Marvell (MRVL) has once again earned Wall Street's attention, but this time it's not about its earnings.

Nvidia (NVDA) CEO Jensen Huang just called it the next trillion-dollar company at Computex. That kind of remark gave the stock a powerful new catalyst and put fresh attention on its role in AI networking and connectivity.

For investors looking for a way to play the next phase of AI buildout beyond GPUs, Marvell may be worth a closer look. The company’s position in optical networking, interconnects, and custom AI infrastructure could make it one of the more interesting names in the chip space right now.

Marvell Deepens Its AI Infrastructure Push

Marvell has been making notable moves in the AI infrastructure market. The company recently partnered with Nvidia, with Marvell’s custom chips set to integrate with Nvidia’s NVLink Fusion platform, a key technology designed to connect AI systems more efficiently. Plus, Nvidia even took a $2 billion equity stake in Marvell. Another recent product win: Marvell just announced Teralynx T100, a 102.4 Tbps switch purpose-built for AI data centers. This is the industry’s first switch of that speed, built on 3nm tech for ultra-high bandwidth at much lower power and latency. It’s aimed at hyperscalers chasing efficient AI networking.

The company also acquired two startups, Celestial AI and XConn, in early 2026 to bolster its AI computing and advanced packaging capabilities. And it added an Anthropic partnership to optimize Marvell’s solutions for that AI leader’s cloud hardware. All told, Marvell is positioning itself as a one-stop shop for AI data center infrastructure, from processors to optical I/O.

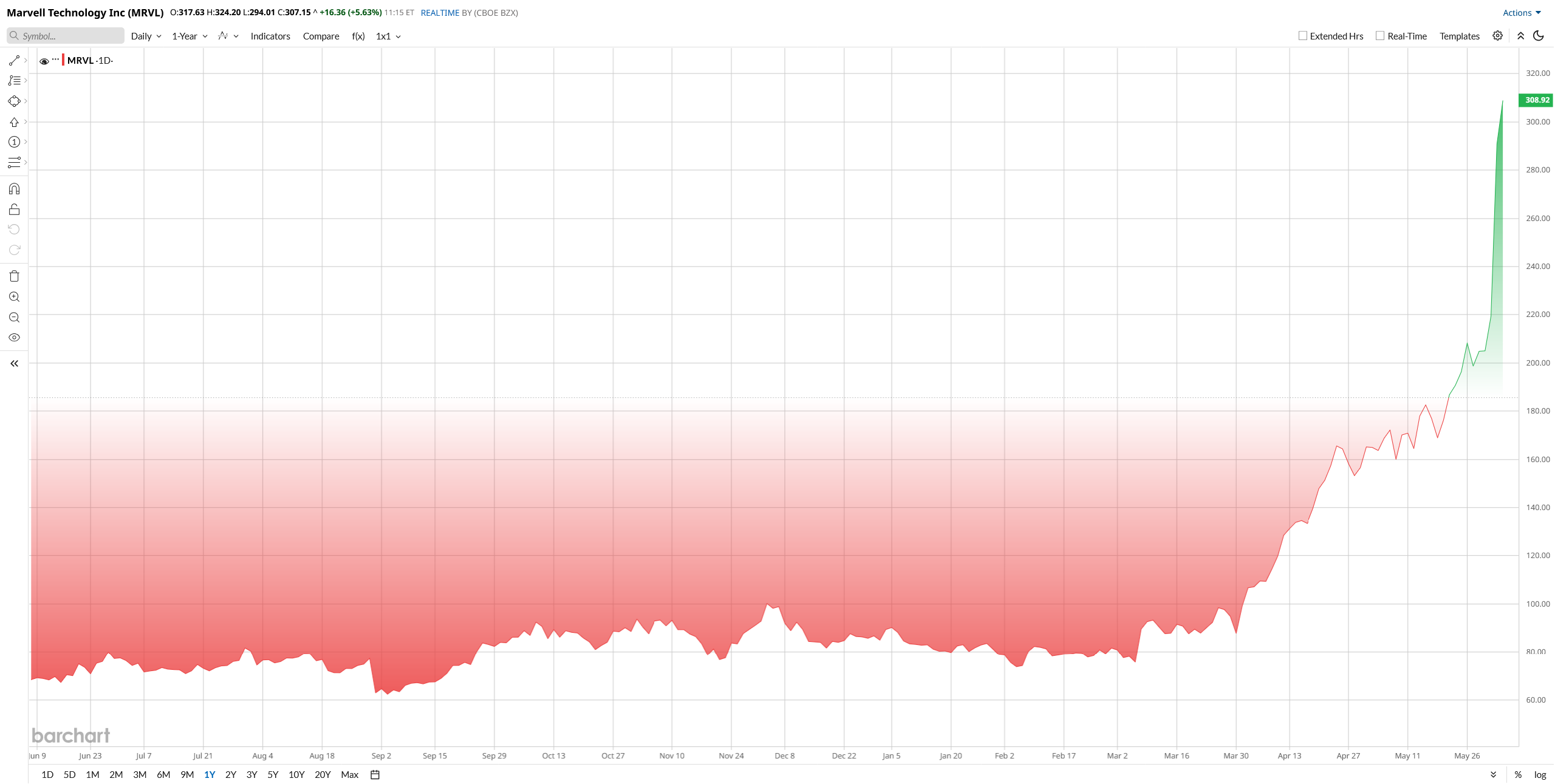

Talking about stock performance, Marvell has crushed the market. Over the past year, its stock has surged over 400%. In 2026 alone, it’s up more than 269% year-to-date (YTD). That huge run means Marvell is well above key moving averages: for example, the 50-day moving average is around $153, while today’s price is near $290. The 200-day average is just $100, so the stock is showing a clear breakout after consolidating gains.

MRVL isn’t trading like a value name. Its multiples are sky-high. Forward EV/sales is roughly 29x and forward P/E near 47x, far above typical chip sector medians. Its PEG ratio is about 1.0, implying investors are banking on massive growth. In other words, you’re paying for a lot of expected future growth here. If data center demand cools, that premium could feel painful.

Nvidia’s “Next Trillion-Dollar” Comment

This week the big news broke at Computex. Nvidia CEO Jensen Huang literally called Marvell the “next trillion-dollar company.” He praised Marvell’s AI and networking role on stage. The market took notice. Marvell’s stock leapt over 30%, closing at a record high around $291.

Traders see that as a major endorsement of Marvell’s AI opportunities. The instant spike erased nearly a quarter of Marvell’s market cap, reflecting renewed confidence and some FOMO. It also means much of the good news is now priced in, which some cautionary analysts note.

Marvell Smashes Q1 Earnings Estimate

Marvell delivered a blockbuster quarter, with revenue rising 28% from a year earlier to $2.418 billion, helped by continued demand from data center customers. Data center sales climbed to $1.83 billion, while communications revenue increased to $585 million, and adjusted earnings came in at 80 cents a share, slightly ahead of company guidance.

Chief Executive Matt Murphy said Marvell delivered record revenue for the quarter and expects second-quarter sales of about $2.7 billion, which would represent 35% growth from a year earlier. He said, “The results reflected accelerating demand from AI-related customers” and added that recent acquisitions, including Celestial AI and XConn, helped broaden the company’s capabilities.

Marvell also reported record operating cash flow of $638.8 million, while net income reached $718 million. The company said its balance sheet remained solid, with cash and equivalents at about $4.39 a share.

For the full fiscal year 2027, Marvell raised its revenue outlook to about $11.5 billion from $11 billion, while management now sees fiscal 2028 revenue around $16.5 billion. The company said networking chips and custom AI silicon are driving a steady stream of bookings.

What Analysts Are Saying About MRVL Stock

Wall Street remains bullish on Marvell’s AI story. Following the company’s Q1 beat and a boost from its Nvidia-related momentum, Stifel raised its price target to $321 from $230 and upgraded MRVL stock to “Buy.” Oppenheimer’s Rick Schafer lifted his target to $200 from $170 and kept an “Outperform” rating, while Bank of America’s Vivek Arya raised his target to $200 from $125 and reiterated “Buy.” Goldman Sachs was more cautious, increasing its target to $180 from $125 and maintaining “Neutral.”

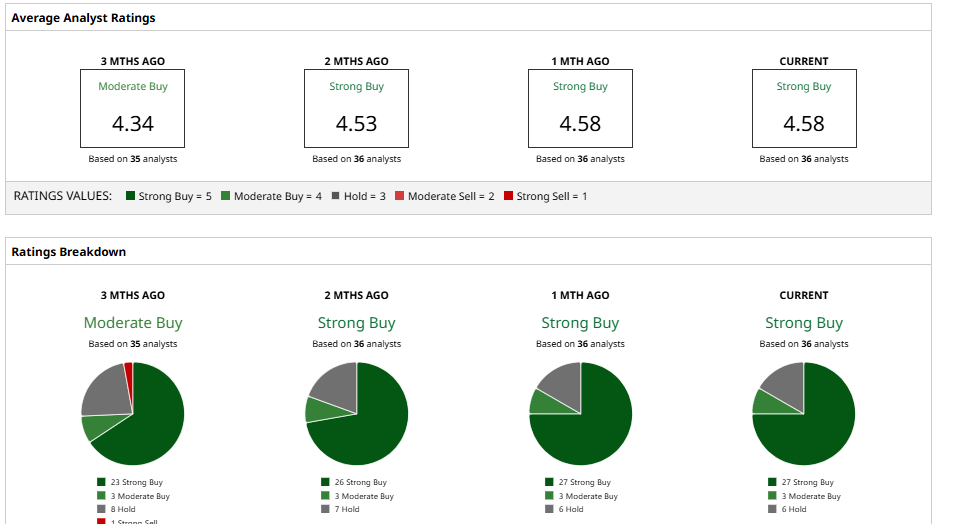

Barchart data shows MRVL stock is rated with a “Moderate Buy” consensus rating. But the average long-term price target for the stock still remains around $224, which is far below recent trading price levels. A re-examination of price targets by analysts is likely soon.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Amazon_com%20Inc_%20%20package%20by%20-%20AdrianHancu%20via%20iStock.jpg)

/Salesforce%20Inc%20HQ%20building-by%20JHVEPhoto%20via%20Shutterstock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Intel%20Corp_%20Santa%20Clara%20campus-by%20jejim%20via%20Shutterstock.jpg)