Software and traditional information technology stocks have recovered over the last week amid a realization that fears of an "AI-pocalypse" are a bit overdone. The rally gained traction after Nvidia (NVDA) CEO Jensen Huang dismissed fears of disruption from artificial intelligence (AI) and said it is “actually an incredible time to be a software company.”

“A lot of people have said […] agentic AI is coming, therefore all of the software companies are going out of business,” said Huang at the COMPUTEX 2026 trade show in Taiwan. "I said: it’s exactly the opposite. Because there are going to be so many agents, the world is no longer limited by the number of people. Therefore, those agents are going to use more tools than ever."

Incidentally, Huang’s views chime with what many software leaders have long been saying. For instance, during the second-quarter earnings call earlier this year, Accenture (ACN) CEO Julie Sweet said that the company plays a “critical role in the AI ecosystem," touting AI as a "tailwind" and saying it would “shape our growth over the next few years.” This bullishness failed to cut ice with investors, however, and ACN stock fell after the confessional, in part due to the soft guidance. Other software stocks have also looked weak this year on fears that AI will disrupt their industries.

However, markets seem to have found value in software stocks after Huang talked up the sector. There has been a broad-based recovery in software and traditional IT stocks across major markets after his comments. Specifically, Accenture is up 4% over the last five days, even though shares are still down 31% year-to-date (YTD). I previously noted that the selloff in ACN stock had gone a bit too far, and the stock seems to offer value, particularly for dividend investors. With that said, let’s explore whether Accenture stock can rise further from these levels.

Accenture’s Capital Allocation Policy is Quite Balanced

Accenture currently has a forward dividend yield of 3.4%, which looks quite healthy. It started paying dividends in 2005 and has increased the payout in every year since at an annualized pace of 11.1%. The company’s dividends should continue to rise in the high single digits over the foreseeable future, which is in line with the earnings growth it is expected to post.

Accenture's capital allocation policy is also quite balanced and spread between dividends, share repurchases, and investing for growth. In the most recent quarter, the firm invested $1.6 billion, which was primarily due to three acquisitions it completed. The company plans to spend $5 billion on acquisitions this year, and the number could go even higher if it finds the “right opportunities.” Many of Accenture's upcoming acquisitions should be in AI, which is something we saw in its few previous deals as well.

Accenture Sees AI as an Opportunity

Accenture has been trying to make AI an opportunity rather than a threat. Apart from acquisitions to enhance its capabilities and help expand its target market, the company has been training its workforce in AI. In Q2, the firm had 85,000 AI and data professionals, which was ahead of the 80,000 it was targeting for the entire fiscal year. Accenture's early leadership in AI has helped it gain market share from competitors. AI has also been a catalyst for its cybersecurity business.

Notably, companies adopting AI also need consulting and professional services companies to implement these projects. Unlike consumer AI, where adoption can be instant and seamless, companies in enterprise AI must consider several factors, including the safety of the massive data they handle and the long-term payoffs. This is where Accenture can fit in with its AI-trained workforce. For instance, Accenture has partnered with OpenAI to help federal agencies “rapidly adopt, migrate, and scale advanced AI.”

Accenture Stock Forecast

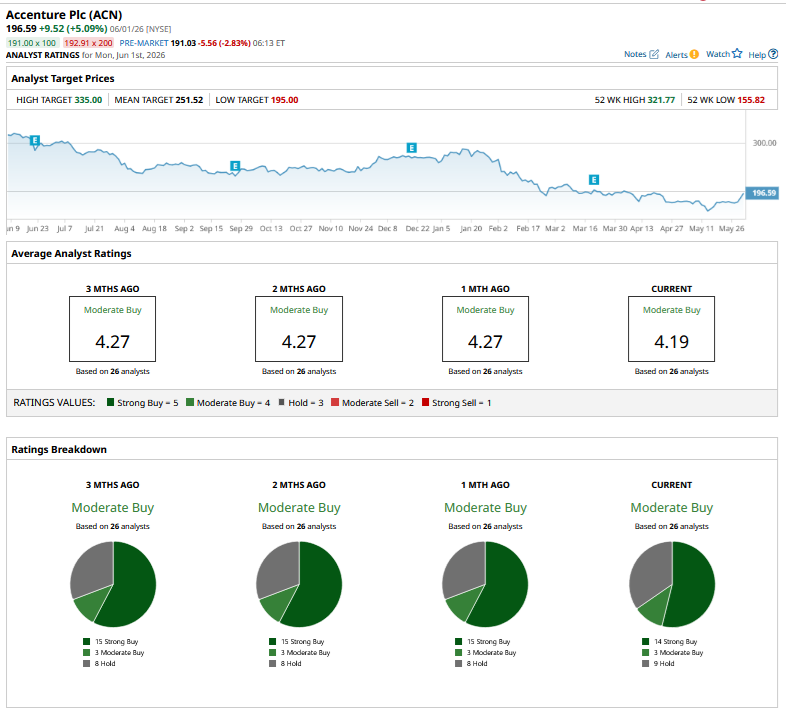

Meanwhile, analysts are not too sold on Accenture’s outlook and have been gradually lowering their target prices on ACN stock. Several brokerages lowered their price targets following the company’s Q2 earnings in March. Most recently, Citigroup lowered its target from $215 to $195, while Truist went a step further and downgraded the stock from a “Buy” to a “Hold” rating while trimming its price target from $260 to $210.

ACN stock has a “Moderate Buy” consensus rating with a mean target price of $251.52, which implies potential upside of 36% from current levels.

Should You Buy Accenture Stock?

I continue to remain constructive on ACN stock and find it reasonably priced at a forward price-to-earnings (P/E) multiple of 13.4 times. The company’s EPS is expected to rise by 7% in fiscal 2026 and 8% in fiscal 2027, and I believe there is scope for next year's estimates to rise further as Accenture's AI business scales up. Overall, the stock's risk-reward looks quite attractive at current prices, and the valuation multiples might expand further as “AI-pocalypse” fears further mellow.

On the date of publication, Mohit Oberoi had a position in: ACN , NVDA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)