With a market cap of $100.4 billion, The Southern Company (SO) is a leading energy provider that supplies electricity to both retail and wholesale customers across the United States. Through its subsidiaries, the company develops, owns, and operates power generation facilities, battery energy storage projects, microgrids, and natural gas distribution networks serving several states.

Companies worth more than $10 billion are generally labeled as “large-cap” stocks and Southern Company fits this criterion perfectly. Headquartered in Atlanta, Georgia, Southern Company also invests in energy-related services, resilience solutions, and telecommunications infrastructure.

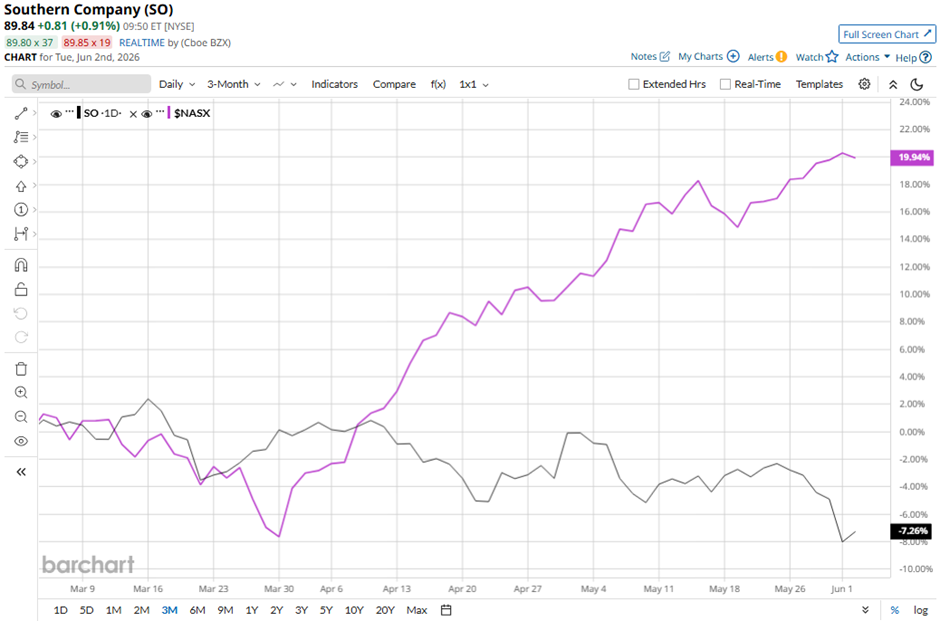

Shares of Southern Company have dipped 11.6% from its 52-week high of $100.83. The stock has declined 7.7% over the past three months, lagging behind the Nasdaq Composite’s ($NASX) 18.8% increase over the same time frame.

SO stock is up 3.3% on a YTD basis, underperforming NASX’s 16.2% gain. In the longer term, shares of the company have decreased marginally over the past 52 weeks, compared to NASX’s 40.4% return over the same time frame.

Despite recent fluctuations, the stock has been trading above its 50-day moving average since early January.

Shares of The Southern Company rose 3.4% on Apr. 30 after the utility reported Q1 2026 adjusted EPS of $1.32, significantly above analysts’ expectations. The earnings beat was supported by strong electricity demand, with commercial kilowatt-hour sales increasing 4.2% and industrial sales rising 1.5%, reflecting growing power consumption from businesses and energy-intensive customers.

Investors were also encouraged by the company’s 7.9% revenue growth to $8.4 billion and its expanding exposure to large data-center customers, having contracted 10 gigawatts of load demand from major clients such as Google, Meta, Microsoft, and Compass Datacenters.

In comparison, rival NextEra Energy, Inc. (NEE) has outpaced SO stock. Shares of NextEra Energy have risen 5.8% on a YTD basis and 21.1% over the past 52 weeks.

While SO stock has underperformed, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of “Moderate Buy” from 25 analysts' coverage, and the mean price target of $102.39 is a premium of 14.1% to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)