/Chubb%20Limited%20office%20sign-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

Zurich, Switzerland-based Chubb Limited (CB) provides insurance and reinsurance products and services. Valued at a market cap of $120.9 billion, the company offers an expansive suite of commercial and personal insurance solutions to a diverse client base ranging from multinational corporations to local small businesses, high-net-worth families, and individual consumers.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and CB fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the insurance - property & casualty industry. The company functions as a highly diversified risk manager capable of absorbing complex exposures on a global scale.

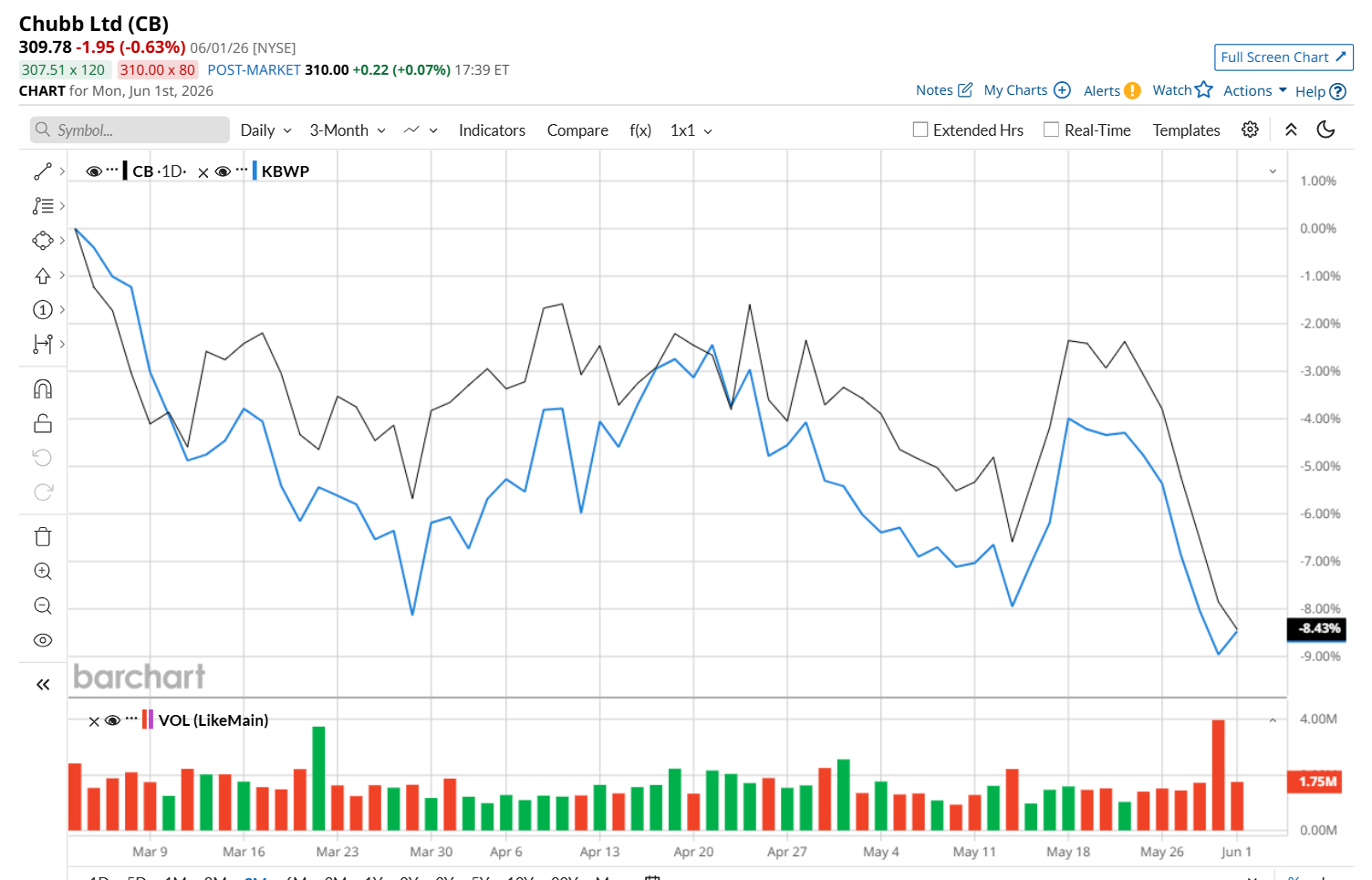

Despite its notable strength, this insurance company has dipped 10.4% from its 52-week high of $345.67, reached on Mar. 2. Moreover, shares of CB have declined 9.1% over the past three months, underperforming the Invesco KBW Property & Casualty Insurance ETF’s (KBWP) 8.3% loss during the same time frame.

However, in the longer term, CB has gained 4.2% over the past 52 weeks, outpacing KBWP's 7.6% downtick over the same time period. Additionally, on a YTD basis, shares of CB are down marginally, compared to KBWP’s 8.9% drop.

To confirm its recent bearish trend, CB has started trading below its 50-day moving average since late May. However, it has remained above its 200-day moving average since early November 2025.

Shares of CB fell 1.2% following its Q1 2026 earnings release on April 21. Driven by record investment income and low catastrophe losses, Chubb reported adjusted EPS of $6.82, which easily beat consensus estimates of $6.48. Its underlying performance also remained robust, highlighted by a 10.7% rise in consolidated net premiums written to $14.01 billion and a stellar P&C combined ratio of 84%. However, investor sentiment was slightly tempered by an increase in after-tax adjusted net realized losses, which rose to $343 million from $59 million a year earlier, alongside management's noted caution regarding softening pricing in large-account commercial property markets.

CB has outperformed its rival, The Allstate Corporation’s (ALL) 1.3% loss over the past 52 weeks. Meanwhile, it has aligned with ALL’s marginal drop on a YTD basis.

Despite CB’s recent underperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 26 analysts covering it, and the mean price target of $349.42 suggests a 12.8% premium to its current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)

/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)