Dual Edge Research publishes two powerful newsletters that work great individually — and even better together. The Bull Strangle Newsletter focuses on stocks and options, combining stock ownership with premium-selling strategies to generate consistent income and market-beating returns. The Smart Spreads Newsletter specializes in seasonal commodity futures spreads, offering a diversified approach with low correlation to equities. Together, they deliver a complete investment perspective — one focused on income, the other on diversification — all under one simple subscription.

Introduction

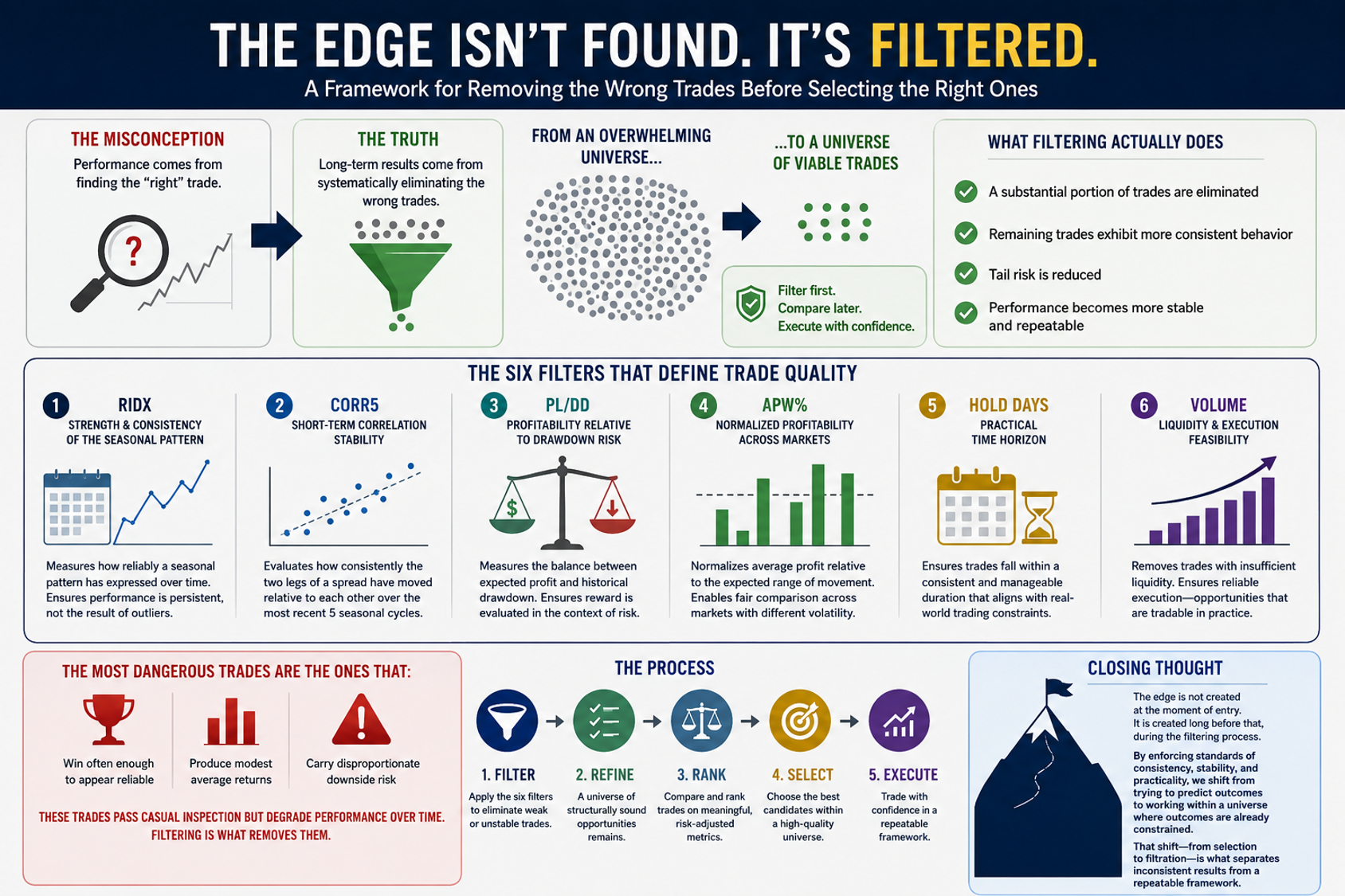

One of the most common misconceptions in spread trading is that performance is driven by finding the “right” trade. In reality, long-term results are far less dependent on discovery and far more dependent on elimination.

The raw universe of seasonal spread opportunities is enormous. Across markets, contract months, and time windows, the number of possible combinations quickly becomes unmanageable. Most of these combinations are not just suboptimal—they are structurally inconsistent, difficult to execute, or prone to unstable outcomes.

The edge, therefore, does not come from identifying a few exceptional trades. It comes from systematically removing the majority of trades that should never be considered in the first place.

Filtering Before Selection

Before any trade is evaluated, ranked, or sized, it must first pass through a series of structural filters. These filters are not designed to optimize performance. They are designed to enforce minimum standards of consistency, stability, and practicality. Only after this process is complete does meaningful comparison begin. This distinction is critical. Without filtering, trade selection becomes a comparison of noise. With filtering, it becomes a comparison of viable alternatives.

The Six Filters That Define Trade Quality

The filtering process relies on a set of metrics that evaluate different dimensions of trade behavior. Each one addresses a specific source of instability or inefficiency within the trade universe.

- RIDX — Strength and Consistency of the Seasonal Pattern: RIDX measures how reliably a seasonal pattern has expressed itself over time. It is not enough for a trade to have a strong average outcome. That outcome must be supported by repeated behavior across multiple years. RIDX helps ensure that observed performance is not the result of isolated events or outliers, but rather reflects a persistent structural tendency.

- Corr5 — Short-Term Correlation Stability: Corr5 evaluates how consistently the two legs of a spread have moved relative to each other over the most recent five seasonal cycles. Stable correlation is essential in spread trading. When correlation breaks down, the spread can behave unpredictably, increasing both volatility and risk. Corr5 acts as a safeguard against structurally unstable relationships.

- PL/DD — Profitability Relative to Drawdown Risk: PL/DD measures the balance between expected profit and historical drawdown. Many trades appear attractive when viewed through the lens of average return alone. However, if large or frequent drawdowns accompany those returns, the trade becomes difficult to hold in practice. This metric ensures that the reward is evaluated in the context of risk.

- APW% — Normalized Profitability Across Markets: Different markets exhibit different volatility profiles. A raw profit figure in one market may not be comparable to the same figure in another. APW% normalizes average profit relative to the expected range of movement, allowing trades to be evaluated consistently regardless of the underlying market. This creates a more meaningful comparison across the opportunity set.

- Hold Days — Practical Time Horizon: Seasonal patterns can exist over very short or very long timeframes. However, not all timeframes are practical for execution. Trades that require extremely precise timing or extended holding periods introduce additional risk. The Hold Days filter ensures that trades fall within a consistent and manageable duration, aligning with real-world trading constraints.

- Volume — Liquidity and Execution Feasibility: Liquidity is often overlooked in theoretical analysis but becomes critical in live trading. Spreads with insufficient volume can produce misleading price behavior, wider bid-ask spreads, and inconsistent fills. The Volume filter removes trades that cannot be executed reliably, ensuring that the remaining opportunities are tradable in practice—not just on paper.

What Filtering Actually Does

Individually, each of these filters addresses a specific weakness. Collectively, they reshape the entire opportunity set. When applied to a large universe of seasonal spreads, the impact is immediate and significant:

- A substantial portion of trades are eliminated

- Remaining trades exhibit more consistent behavior

- Tail risk is reduced

- Performance becomes more stable and repeatable

This is not optimization. It is a structural refinement. The goal is not to find the best possible trade in hindsight. It is to define a universe where most remaining trades are viable before selection even begins.

Why This Matters

The most dangerous trades are not the obvious losers. They are the trades that:

- Win often enough to appear reliable

- Produce modest average returns

- Carry disproportionate downside risk

These trades pass casual inspection but degrade performance over time. Filtering is what removes them. Once the universe has been reduced to structurally sound candidates, differences in performance become meaningful. At that point, ranking, selection, and portfolio construction can be applied with confidence.

Closing Thought

In seasonal spread trading, the edge is not created at the moment of entry. It is created long before that, during the filtering process.

By enforcing standards of consistency, stability, and practicality, traders shift from trying to predict outcomes to working within a universe where outcomes are already constrained. That shift—from selection to filtration—is what separates inconsistent results from a repeatable framework.

More Information

Now you can get two powerful newsletters — for one simple price!

- For stocks and options, the Bull Strangle Newsletter shows you how to combine stock ownership with dual option selling — a disciplined strategy that has consistently outperformed the S&P 500.

- For commodity futures, the Smart Spreads Newsletter focuses on seasonal commodity spreads — a proven, low-correlation approach that thrives in all types of markets.

Each newsletter is designed to deliver consistent income on its own — but when used together, they create a complete, diversified trading approach that works in any market environment.

Visit BullStrangle.com to subscribe for just $1 for the first month.

For a video overview of the Bull Strangle Newsletter

For a video overview of the Smart Spreads Newsletter

Darren Carlat

Dual Edge Research

(214) 636-3133

DualEdgeResearch@gamil.com

Disclaimer

This information is for informational purposes only and should not be considered as investment advice. Past performance is not indicative of future results, and all investments carry inherent risk. Consult with a financial advisor before making any investment decisions.

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

/Qualcomm%2C%20Inc_%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)

/Advanced%20Micro%20Devices%20Inc_%20logo%20and%20chart%20data-by%20Poetra_%20RH%20via%20Shutterstock.jpg)