When you think of credit cards, you usually think of two choices: Visa or Mastercard. That’s how big these two companies have become in the global payments ecosystem. They’re at the center of nearly every card transaction all over the world, even if consumers rarely directly interact with the company.

But of course, many long-term investors are interested in both, present company included. And while it’s easy to buy Visa and Mastercard stock in a single portfolio, some of us may not have that option and are forced to choose between the two.

So, which business is better: Visa or Mastercard? Which one offers stronger long-term growth, more stable earnings, and better exposure to global spending trends? And lastly, which one deserves a spot in your portfolio?

Let’s find out.

Visa (V)

Visa Inc. is a payments technology company operating as one of the largest electronic payment networks in the world. It connects consumers, merchants, banks, and businesses, helping process card and digital transactions across markets.

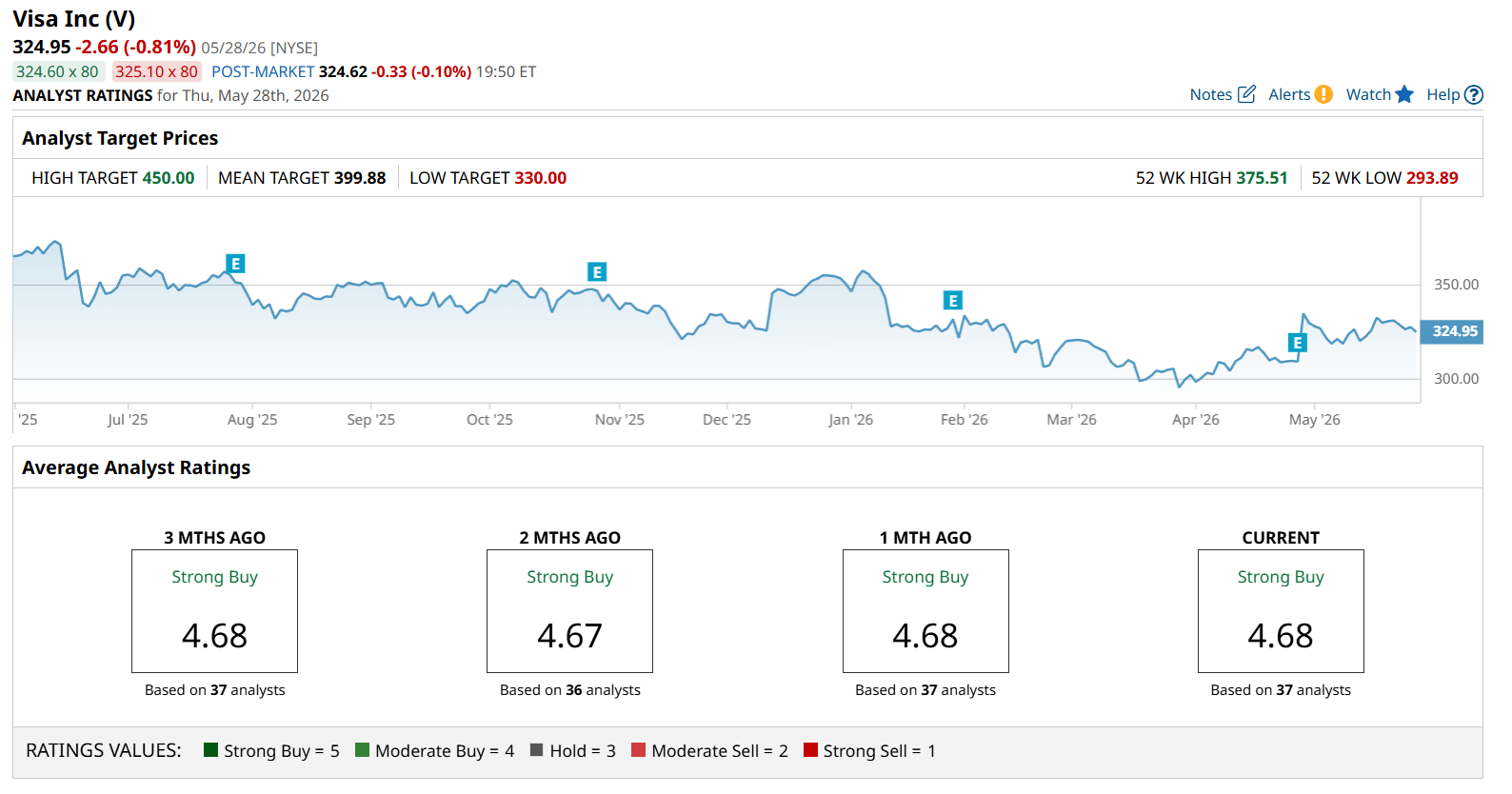

It has a market cap of $587 billion, and the stock traded between $294 and $376 over the past 52 weeks. Today, it's priced around the lower end of that range.

Mastercard (MA)

The rival, Mastercard Inc. also another payments company providing the network and technology behind card and digital payments. Its services help individuals and businesses move money electronically, supporting everyday payments, both local and cross-border.

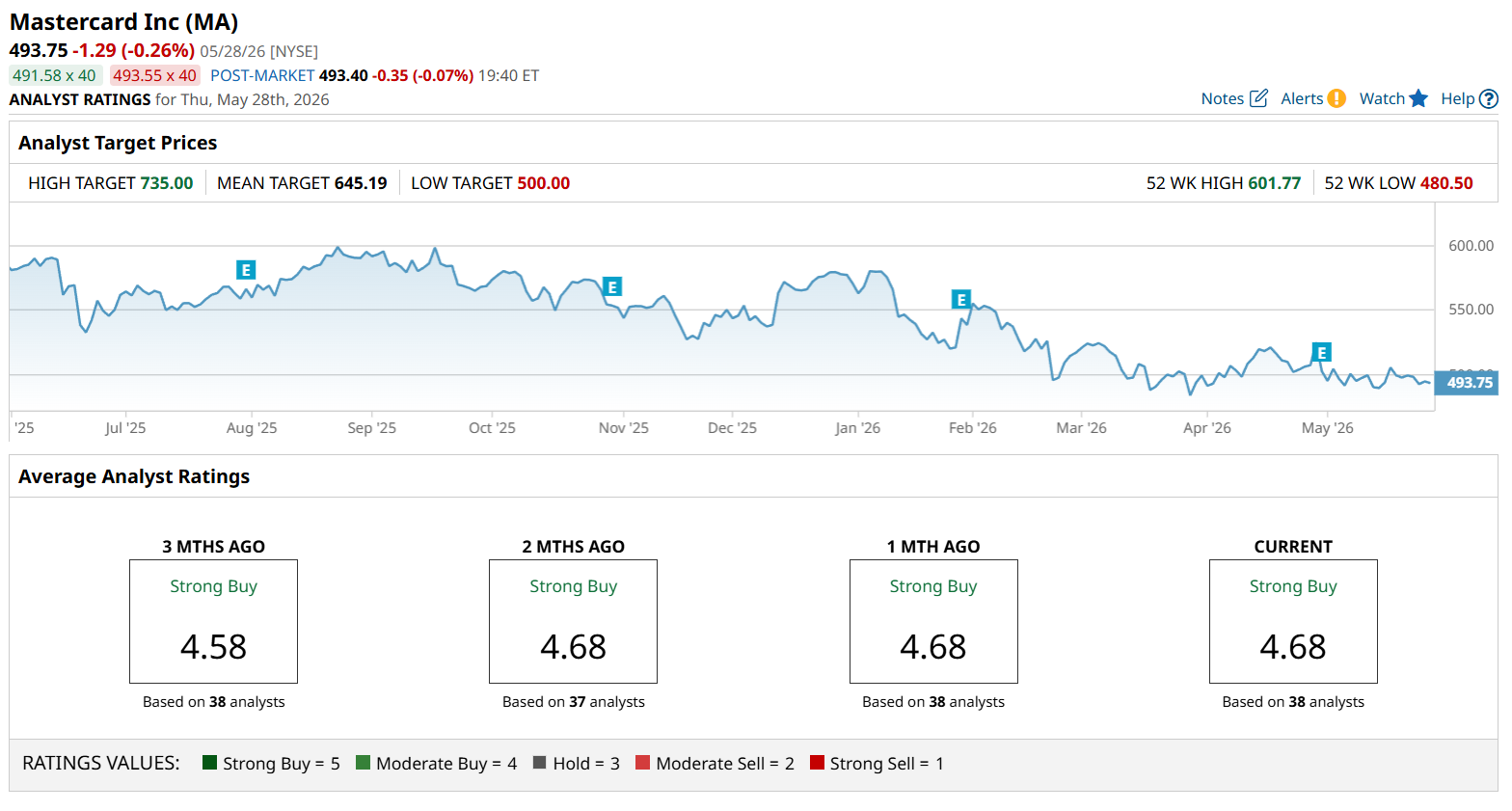

Mastercard is the smaller company of these two, with a market cap of $437 billion. Over the past 52 weeks, its stock traded between $480 and $602, and, like Visa, it's also trading near its 52-week low.

Now, onto the most important question: Which company is the better buy? Let’s find out.

Business model head-to-head comparison

Visa and Mastercard have nearly identical business models.

Visa and Mastercard operate the payment networks that handle transactions between consumers, merchants, and banks.

Neither of them issues cards, extends credit, or assumes credit risk when someone fails to pay their balance. Instead, they let the banks and financial institutions take that responsibility. When a Visa or Mastercard-branded card is used for a transaction, the respective company earns revenue from network-related fees.

The difference lies in scale: Visa has a larger network, giving it wider reach and greater payment volume. Mastercard is smaller, but it still has a strong global presence and meaningful exposure to international and cross-border transactions

Financial comparison

Now let’s look at their latest reported quarterly numbers.

| Metric | Visa | Mastercard |

| Net Revenue | $11.23 billion (+17% YOY) | $8.40 billion (+16% YOY) |

| Net Income | $6.02 billion (+32% YOY) | $3.88 billion (+18% YOY) |

| Forward P/E | 24.93x | 25.16x |

Right off the bat, Visa had higher revenue and growth, up 17% YOY to $11.2 billion, compared to Mastercard, whose net revenue was up 16% to $8.4 billion.

In terms of profitability, the trend is the same. Visa’s net income grew 32% to $6.02 billion, outpacing Mastercard’s earnings growth of 18%.

Valuation-wise, both stocks trade at forward P/E ratios of around 25x, above the sector average of 11.14x. The P/E ratio is a metric that indicates how much investors are willing to pay per dollar of profit, and right now, they are willing to pay a premium. That suggests both Visa and Mastercard are overvalued by over double the sector average.

Now, that’s not necessarily a bad thing, because top companies in their respective sectors typically have future growth and market expectations baked into their current price. Although that leaves less room for error on the company’s part.

Overall, Visa holds the slight edge, but Mastercard remains competitive with strong growth and similar valuation metrics.

Dividend profiles

Dividends can provide a cushion for investors, especially when stocks trade at a premium, as they offer returns regardless of short-term price movements.

Now, right off the bat, these two companies are excellent choices for dividend growth, but we couldn't exactly call them high-yield dividend stocks.

With that out of the way, Visa pays a forward annual dividend of $2.68, translating to a yield of around 0.8%. The company has also raised its dividend for 17 consecutive years, and payouts have increased by 97% in the last five years.

On the other hand, Mastercard has a 13-year dividend streak. It pays $3.48 per share, translating to an approximately 0.7% yield, and the company has increased its dividends by 90% over the last five years.

So that’s another point for Visa.

Wall Street opinion

Now, let’s see what Wall Street has to say.

A consensus among 37 analysts rates Visa stock a “Strong Buy,” with mean-to-high target prices suggesting between 23% and 38% upside over the next year.

The sentiment is practically the same for Mastercard, with a consensus rating of “Strong Buy” from 38 Wall Street analysts. Its mean-to-high target prices suggest between 31% and 49% potential upside.

Final thoughts

Based on the metrics, Visa is likely the better buy, with stronger financials, dividends, and a similar valuation.

However, Mastercard offers more room for capital growth, going by analyst target prices. Both companies have a strong future; it all depends on their execution and ability to adapt to market demands, so make sure to do your due diligence.

On the date of publication, Rick Orford had a position in: V, MA. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.