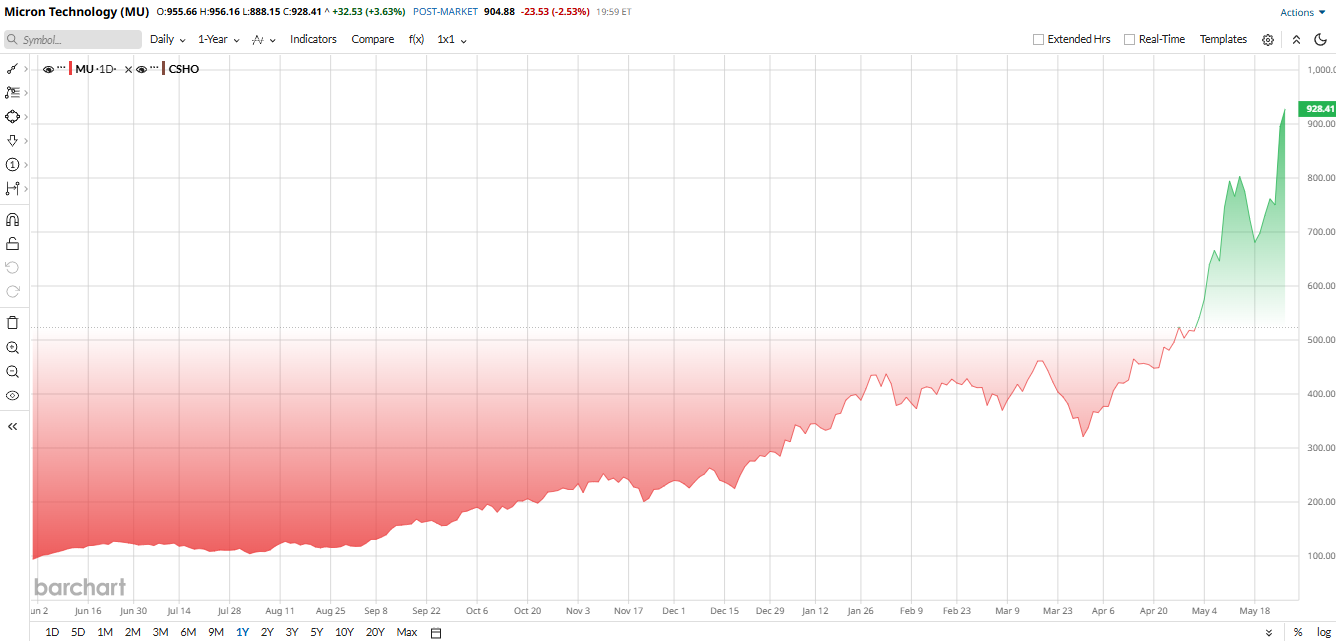

Micron Technology (MU) has gone from a cyclical also-ran to one of the most talked-about stocks in the market. The company briefly crossed the $1 trillion mark on May 26 after UBS raised its price target to $1,625 from $535, and the rally spilled over into other memory names as investors kept betting that AI data centers will keep using more high-bandwidth memory and NAND flash. The broader chip group has been hot too, with semiconductors leading the market and the Philadelphia Semiconductor Index hitting a record as AI spending keeps widening.

Micron is still a memory-chip maker at heart, but that now looks like a much better business than it did a few years ago. The stock has climbed more than eightfold over the past 12 months and is up 223% year-to-date, with the rally driven by AI demand, tight supply, and pricing power that has changed the story around the company.

Why the Stock Still Looks Powerful

The chart has been stretched for months, but momentum keeps winning. Micron bounced back above its 50-day moving average in March, and later technical commentary warned the stock was trading far above its 200-day average, which usually signals a stock that is already well ahead of itself. Even so, buyers have kept showing up because the company’s fundamentals keep getting better.

On valuation, Micron is a little tricky. It does not look cheap on sales, but it still looks inexpensive on earnings. Micron trades at 8.4 times expected earnings over the next 12 months, compared with 22.15x for the S&P 500 and 26.23x for the Nasdaq 100. That is why some bulls still call it a value story, even after a monster rally.

What the Trillion-Dollar Move Really Says

The trillion-dollar club is more than a bragging right. It tells you that investors no longer see Micron as just a boom-and-bust memory stock. They are starting to view it as an AI infrastructure play, because memory has become critical to data movement and model training inside AI servers. UBS said its higher target reflects stronger AI demand and long-term supply agreements, while the company’s 2026 HBM supply is already sold out and HBM4 production is underway.

That matters for the stock’s future. If AI demand keeps outrunning supply, Micron can keep enjoying better pricing and better margins. If supply catches up too fast, the old cyclical story can come back. That is the main reason the stock still has room to run, but also still carries real risk.

The Latest Quarter Gave Bulls Plenty to Like

Micron’s fiscal second quarter was the kind of report that can change a stock’s narrative. Revenue nearly tripled to $23.86 billion from $8.05 billion a year earlier, while net income climbed to $13.79 billion, or $12.07 a share, from $1.58 billion, or $1.41 a share. On an adjusted basis, earnings came to $12.20 a share, well above the $9.19 estimate cited by analysts. Gross margin also improved to about 75%, which shows how much pricing power the company has picked up.

Micron also printed $6.9 billion in adjusted free cash flow and ended the quarter with $16.7 billion in cash, marketable investments, and restricted cash. Management raised fiscal 2026 capital spending to above $25 billion, from an earlier plan, and guided fiscal third-quarter revenue to $33.5 billion, far above Wall Street’s $24.29 billion expectation at the time. It also projected adjusted EPS of $19.15 for the quarter.

“Micron set new records across revenue, gross margin, EPS, and free cash flow in fiscal Q2, driven by a strong demand environment, tight industry supply, and our strong execution, and we expect significant records again in fiscal Q3,” according to CEO Sanjay Mehrotra.

Mehrotra argued that memory has become a strategic asset in the AI era. That is the heart of the bull case now. Micron is not just selling more chips. It is selling into a market that still looks short on supply.

Micron Is Spending to Stay Ahead

The company is not standing still. Recently, Micron bought Powerchip’s Tongluo fabrication site in Taiwan for $1.8 billion and plans to build a second facility there as it expands leading-edge DRAM and HBM capacity. Micron has also said its next-gen HBM4 chips for Nvidia’s (NVDA) Vera Rubin platform are in production, and that its 2026 HBM supply is already sold out. Those are the kinds of moves that support the idea that demand is staying ahead of supply.

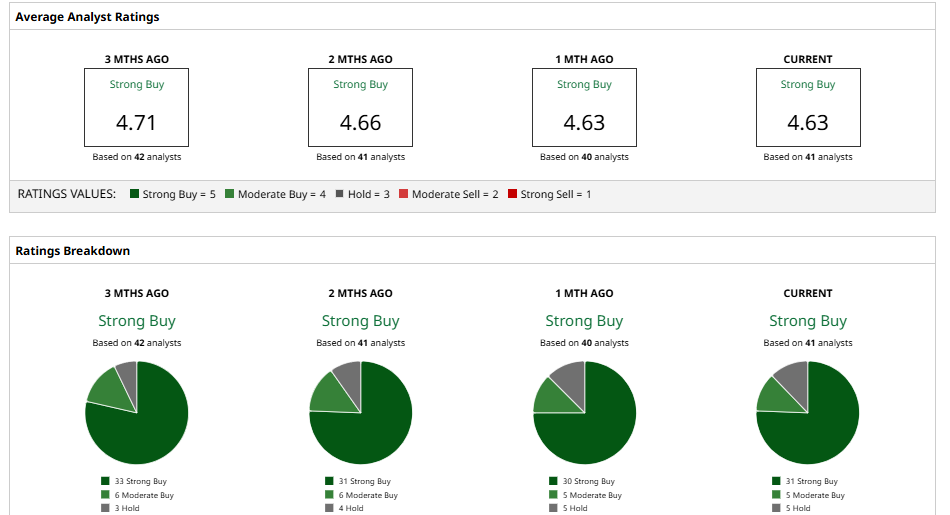

Analysts Still Think the Rally Can Run

Wall Street remains very bullish, even after the run. UBS is now at $1,625, Morgan Stanley once called Micron a top pick with a $520 target, KeyBanc recently had a $600 target, and D.A. Davidson initiated coverage with a “Buy” and a $1,500 target. Mizuho also kept Micron as a top pick. The common thread is the same: Analysts think AI memory demand can stay tight longer than the market once believed.

Still, not everyone is blind to the risk. Some analysts warn that new capacity could pressure memory prices in 2027 and 2028, which is why Micron still deserves respect as a cyclical stock, even if it is now a much better one than it used to be.

But overall it's a consensus “Strong Buy” and it still gives 76% upside from its street target of $1,625.

For now, the stock looks like it still has room to run. The bigger question is how long the AI memory boom lasts.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)