The semiconductor market is having a huge year. Research firm Omdia now expects industry revenue to grow 62.7% in 2026, with the DRAM market alone nearly doubling from 2025. Computing and data storage revenue could pass $700 billion, up 90% year-over-year (YOY). Prices are moving just as fast.

Contract DRAM prices have already jumped 58% to 63% over the past quarter, and Gartner says they could rise another 125% in 2026. Etron Technology’s chairman Nicky Lu also said prices are still climbing 10% to 20% every month.

One of the biggest winners from this surge is Micron Technology (MU). On May 27, UBS analyst Timothy Arcuri raised his price target to $1,625 from $535, more than tripling it. He pointed to major shifts in the memory market and new long-term supply deals that give Micron Technology better earnings visibility.

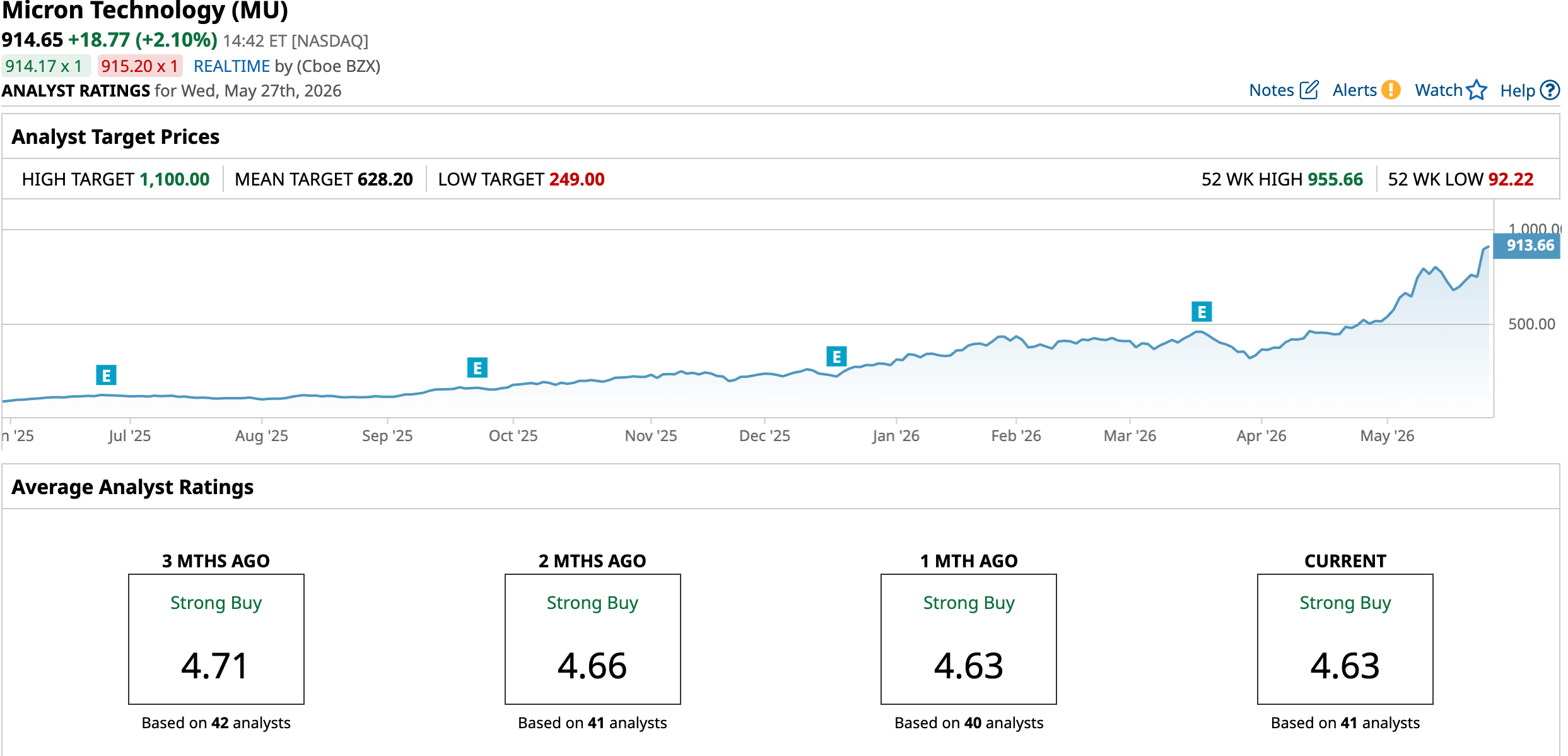

It is now the highest target on Wall Street and suggests about 116% upside from the stock’s last close at the time. The market reacted quickly. Within hours, MU stock jumped 19.3%, pushing Micron Technology past a $1 trillion market cap and making it the 11th U.S. company to hit that mark.

With a call like that, can Micron Technology still double from here, or has most of the upside already played out?

Inside Micron’s Latest Numbers

Micron Technology makes memory and storage chips, mainly DRAM and NAND, which are used in data centers, AI servers, and everyday electronics.

Over the past 52 weeks, Micron Technology shares are up 841.66% and have gained another 218% so far this year.

Even after that rally, the stock still trades at a forward price-to-earnings of 12.99 times, which is well below the sector average of 24.99 times. Micron Technology also pays a small dividend. Its most recent payout was $0.15 on March 30, giving the stock a 0.07% yield and a forward payout ratio of 2.13%. That is still far below the technology sector average yield of 1.37%, and the company has only one year of dividend increases with quarterly payments.

The latest numbers beamed strength. Revenue came in at $23.86 billion, up 196% from a year ago and 20.1% above estimates. Adjusted EPS was $12.20, beating forecasts by 40.8%. Operating income rose to $16.46 billion, and operating margin expanded to about 69% from 22% a year earlier. Free cash flow improved to $6.9 billion from a negative $113 million, while inventory days slipped to 123. Guidance was also strong, with Q2 revenue projected at $33.5 billion and adjusted EPS at $19.15, both comfortably above Wall Street expectations.

The Drivers Behind the Story

Micron's growth plan is now heavily tied to making more chips, and Taiwan is a big part of that. The company has completed its acquisition of PSMC’s P5 site in Tongluo, Taiwan, a deal first announced on Jan. 17, 2026. The site adds about 300,000 square feet of existing 300mm cleanroom space and expands Micron Technology’s manufacturing footprint near its Taichung campus. The goal is to produce more advanced DRAM, including HBM, to keep up with strong AI demand. Micron Technology has already started retrofitting the site, and meaningful shipments from the fab are expected in fiscal 2028.

The Taiwan expansion does not stop there. Micron Technology also plans to build a second facility at the Tongluo site, adding another roughly 270,000 square feet of cleanroom space, with construction expected to begin by the end of fiscal 2026. The $1.8 billion Powerchip deal lifts Micron's global capacity by more than 10%, which matters because management has already said it may only be able to meet about half to two-thirds of global demand.

Back in the U.S., Micron Technology has started producing 1α DRAM at its Manassas, Virginia, fab, the most advanced memory ever made in the country. That technology will quadruple DDR4 wafer supply at the site and help support U.S. customers in automotive, defense, aerospace, industrial, networking, and medical devices. It also fits into a much bigger plan that includes two new fabs in Idaho by the end of 2028 and the company’s long-term $100 billion chip project in New York.

What Analysts Expect Next

For the current quarter ending May 2026, analysts on average expect earnings of $18.97 per share, up from $1.73 a year ago, which would mean 996.53% growth. For the August 2026 quarter, the estimate rises to $22.02 per share from $2.86 a year earlier, a 669.93% jump. For full-year fiscal 2026, the forecast stands at $57.82 per share, up from $7.68 last year, or 652.86% growth.

UBS may have the boldest target on Wall Street, but it is not the only bullish firm. Mizuho kept its “Outperform” rating and its $800 price target, with analyst Vijay Rakesh saying there is still “no clear line of sight” on when the memory supply-demand imbalance will end because DRAM and NAND are still key to AI demand.

CFRA also got more bullish in mid-May, raising its target to $900 from $500. Analyst Angelo Zino said Micron Technology’s financial position has “vastly improved,” and he expects pricing to stay strong well into 2027 as AI spending and HBM wafer demand remain high.

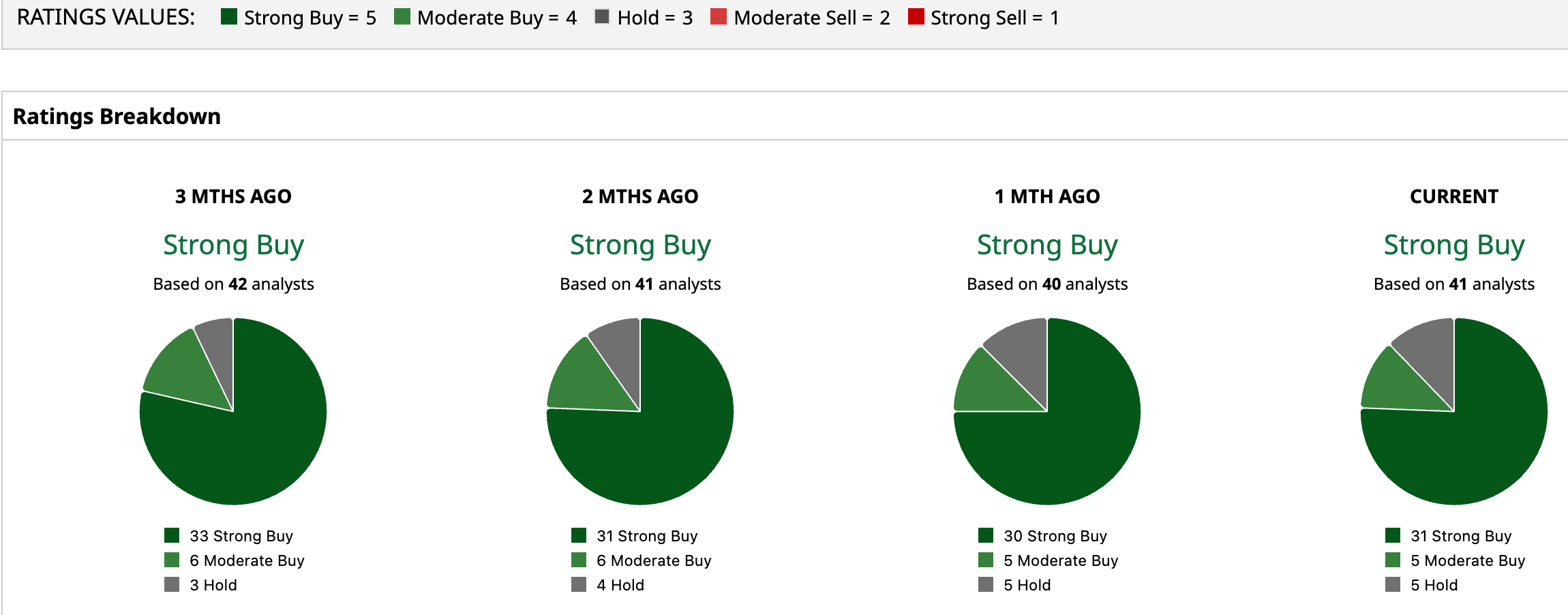

Analysts overall are still very bullish on Micron Technology. The consensus of 41 analysts surveyed rates the stock a “Strong Buy.” The average price target of $628.20 has already been surpassed, but the Street-high price of $1,100 shows Micron Technology could climb 20.27% from here.

Conclusion

Micron still looks buyable here, but only for investors who can handle volatility after such a massive run. The bull case is straightforward: earnings are exploding, AI-driven memory demand remains tight, capacity is expanding, and analysts still see pricing strength lasting into 2027. Even so, MU has already moved far ahead of the average Wall Street target, so this is probably not an ideal entry point for investors chasing quick upside. Most likely, the stock continues trending higher over time if execution stays strong, though near term swings and pullbacks would not be surprising after such an extraordinary rally.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)