/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

Dell (DELL) stock has been on a stunning run, surging more than 107% in just three months as it is benefitting from the artificial intelligence (AI) boom.

The rally gained momentum after Dell delivered stronger-than-expected fourth-quarter results alongside an upbeat outlook. A major catalyst behind the surge is exploding demand for Dell’s AI-optimized servers. Enterprises are rapidly increasing spending on AI infrastructure, upgrading data centers, and deploying high-performance computing systems to support next-generation workloads. That trend is creating a massive opportunity for Dell as businesses race to scale their AI capabilities.

With Dell scheduled to report first-quarter fiscal 2027 earnings on May 28, the momentum in its business is likely to accelerate. Moreover, Dell’s valuation is still reasonable. All these indicate that Dell stock has room to run.

Dell’s Q1 Growth to Show Acceleration

Dell delivered strong financial numbers to end fiscal 2026. Meanwhile, the first quarter fiscal 2027 growth rate is expected to remain even higher and accelerate sequentially.

The company reported Q4 revenue of $33.4 billion, up 39% year-over-year (YOY), while adjusted earnings per share (EPS) surged 45% to $3.89. The strong results were driven by accelerating AI demand and strong execution.

Dell’s AI business is growing at a solid pace, driven by strong orders and expanding enterprise adoption. In Q4 alone, Dell booked $34.1 billion in AI orders and shipped $9.5 billion worth of AI servers. The company exited the quarter with a record $43 billion AI backlog, signaling that demand continues to outpace supply even after massive shipment volumes.

Over the full fiscal year, Dell generated $64.1 billion in AI orders, with its AI customer base growing to more than 4,000 organizations. Importantly, growth is driven by a broad mix of hyperscalers, sovereign AI initiatives, neocloud providers, and traditional enterprises.

Adding to the positives, demand for Dell’s traditional server business also remains healthy. While GPUs are essential for AI model training, enterprises still require significant conventional computing infrastructure to support broader AI deployments, storage, networking, and enterprise workloads. This is creating a favorable environment for Dell’s broader Infrastructure Solutions Group (ISG).

Looking ahead, management expects first-quarter fiscal 2027 revenue to come in between $34.7 billion and $35.7 billion, representing approximately 51% growth at the midpoint. ISG is projected to grow more than 100%, supported by roughly $13 billion in AI server revenue. Meanwhile, the Client Solutions Group (CSG), which includes PCs and related products, is expected to deliver modest growth of around 2%.

Profitability is expected to improve sharply. Dell forecasts operating expenses to decline by low single digits, while operating income is expected to rise roughly 60%. Adjusted EPS is projected at approximately $2.90, implying around 87% YOY growth at the midpoint. The guidance is also higher than the analysts’ consensus EPS estimate of $2.79.

Dell’s Valuation Still Points to More Upside Ahead

Despite Dell’s impressive rally, the stock may still have room to run. The company appears poised to accelerate growth in fiscal 2027, driven by booming demand for AI infrastructure and renewed strength in its traditional server business. Record backlog levels, rising enterprise adoption, and improving profitability all position Dell to deliver another year of strong financial performance.

Importantly, Dell stock currently trades at roughly 24.86 times forward earnings, which still looks reasonable relative to its earnings outlook. Analysts expect EPS to surge 32% in fiscal 2027, with projections likely to rise further as AI spending continues to expand.

Momentum may not stop there. Dell is also projected to maintain double-digit earnings growth in fiscal 2028.

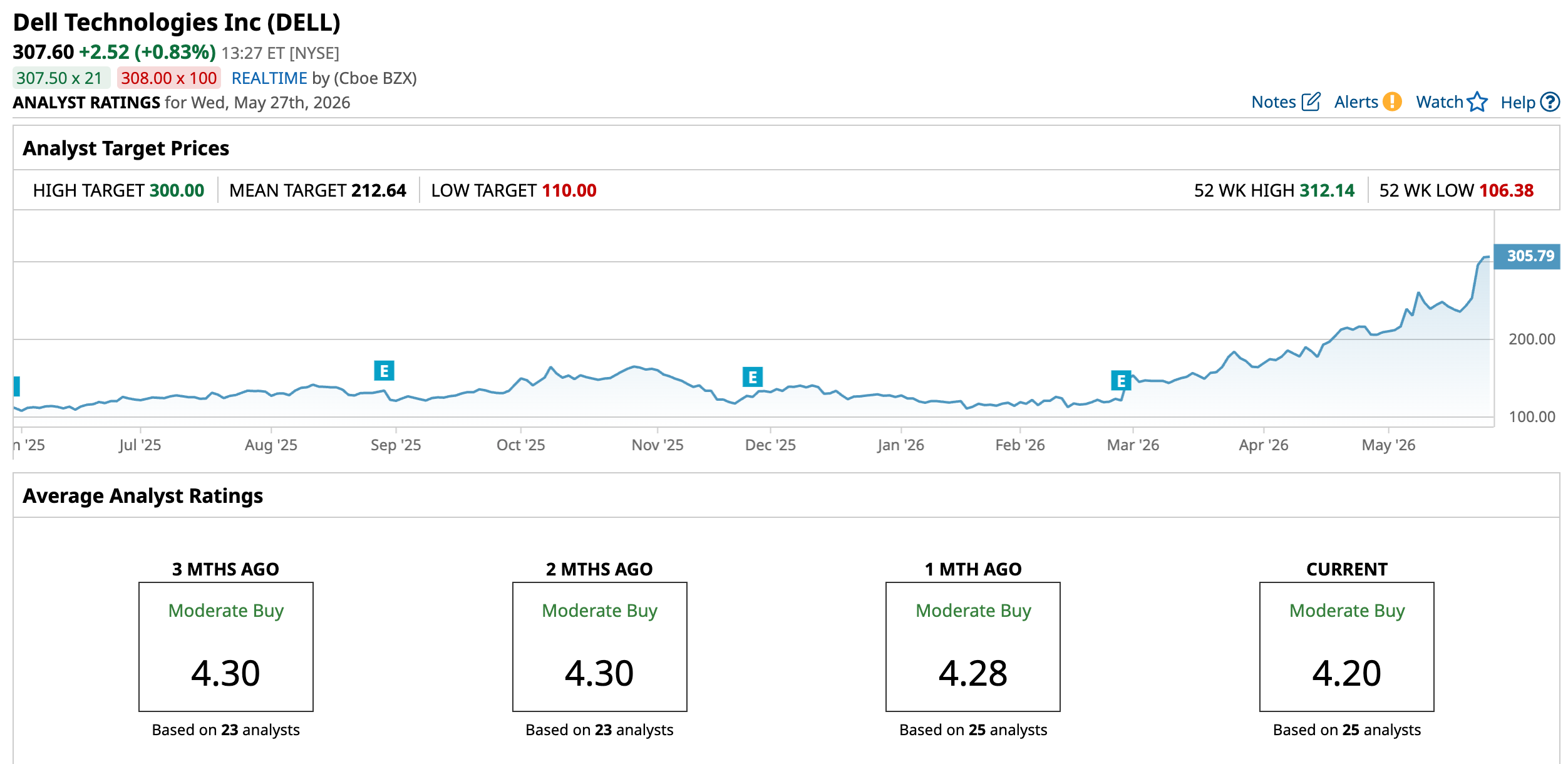

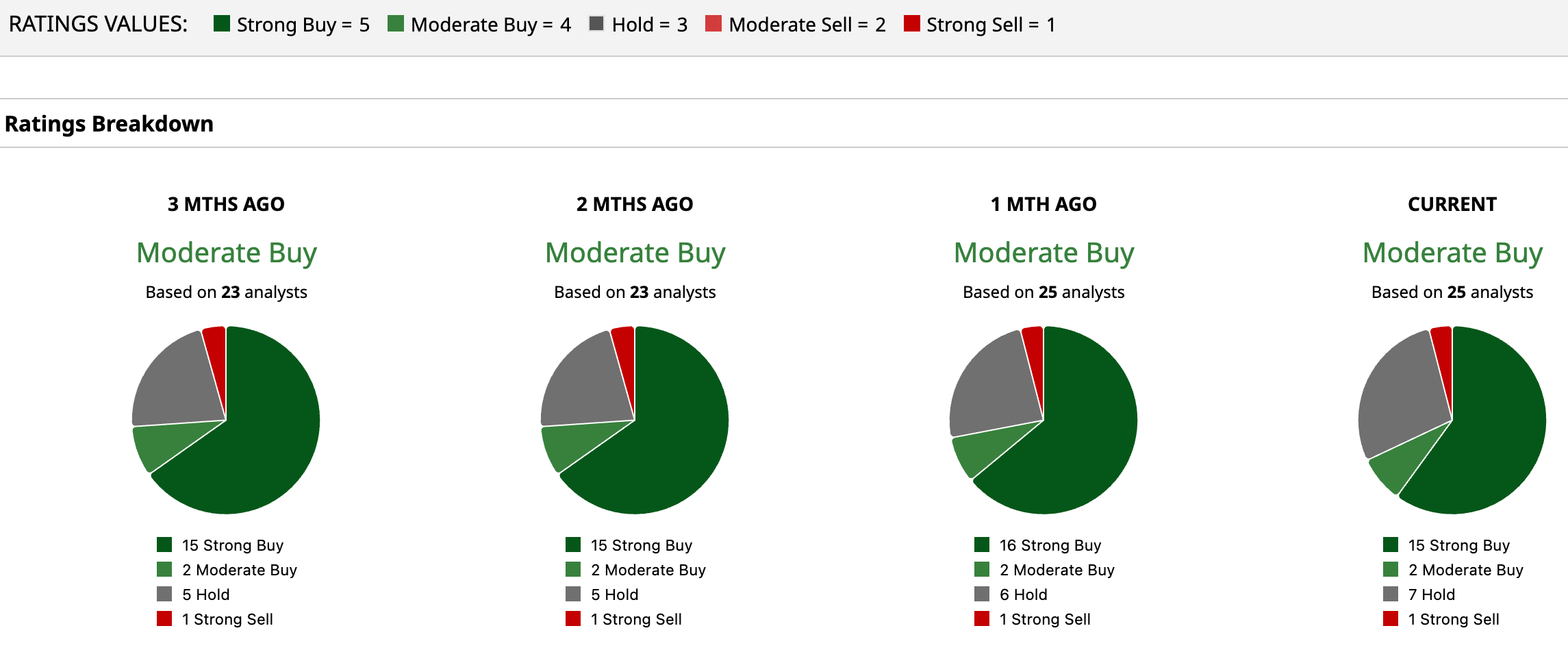

Dell’s strong growth and still-attractive valuation suggest Dell stock could continue to climb through 2026. Wall Street currently rates Dell stock as “Moderate Buy.”

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)