/Western%20Digital%20Corp_%20external%20harddisk-by%20charnsitr%20via%20Shutterstock.jpg)

Western Digital (WDC) looks like one of the more compelling AI infrastructure plays on the market right now, and Wall Street is starting to price that in more aggressively.

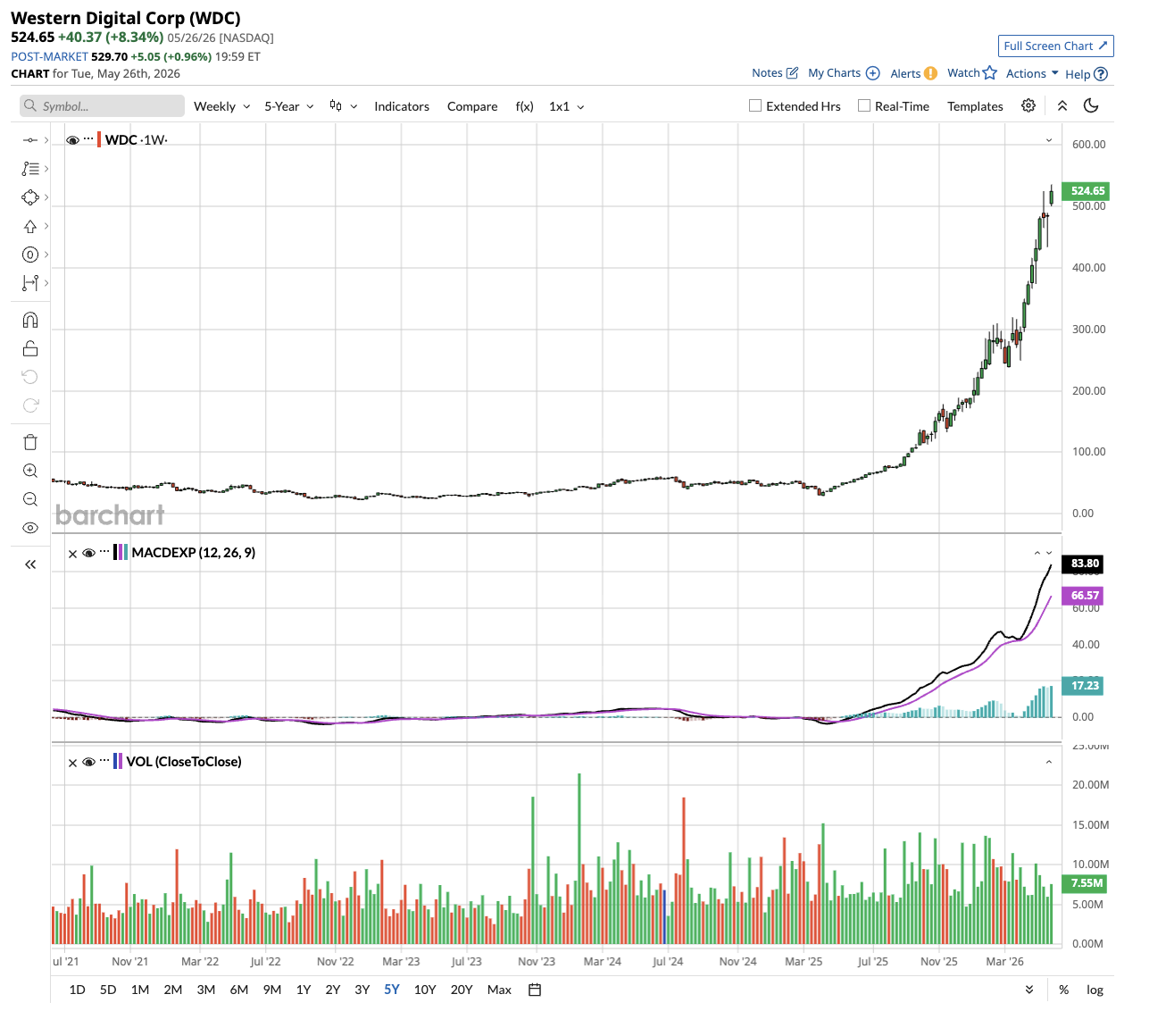

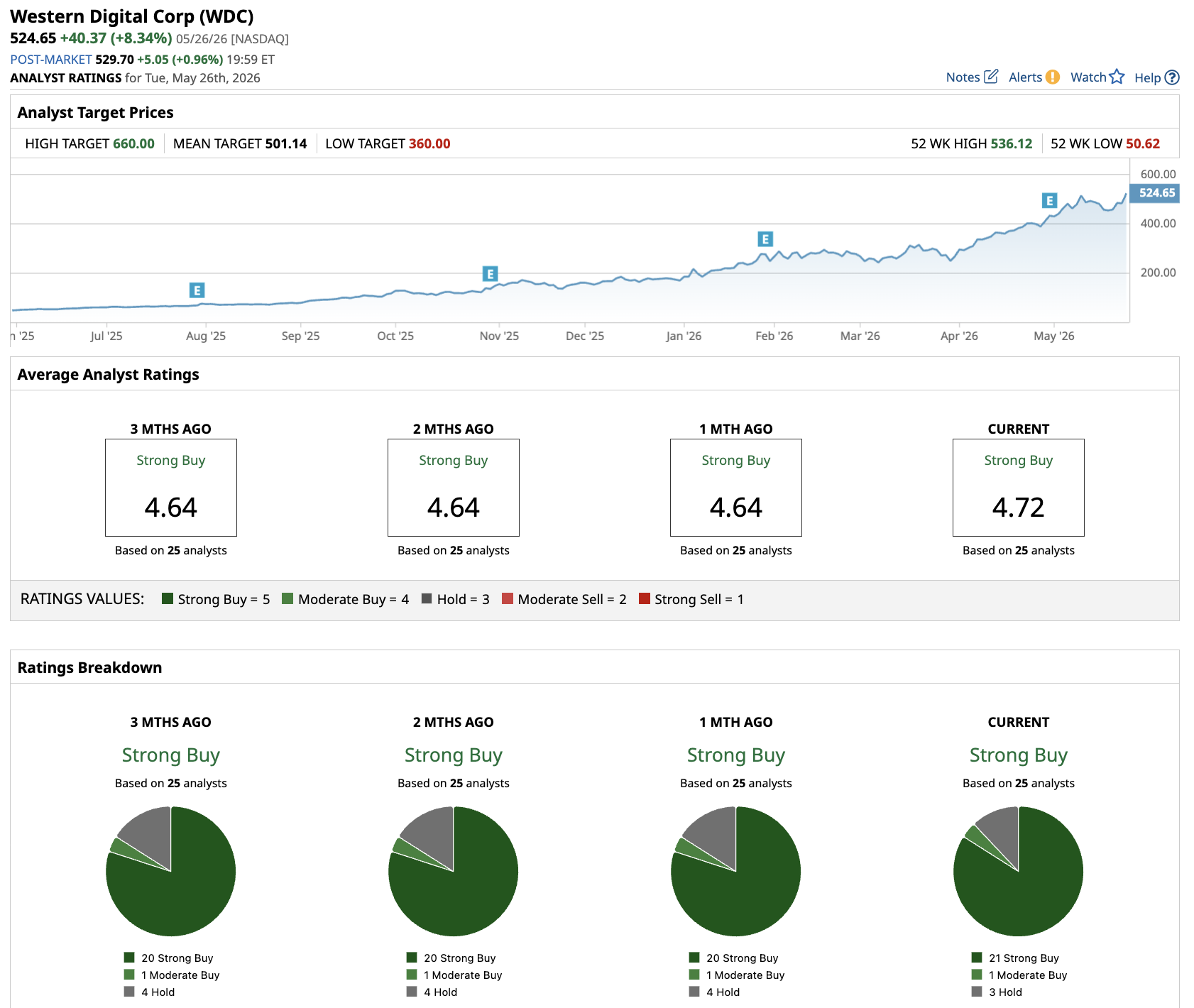

Evercore ISI raised its price target on Western Digital to $575 from $410 while maintaining its “Outperform” rating on the stock. The investment firm made the move following investor meetings with the company's investor relations team. WDC stock currently trades around $525, and the new target implies roughly 10% upside from here.

The call reflects a broader argument Evercore ISI is making: that the hard disk drive industry is critical to the AI buildout but still widely under appreciated by investors.

The AI Moat for WDC Stock

When people think about AI infrastructure, they picture graphics processing units, data centers, and high-bandwidth memory. Evercore ISI said the hard disk drive industry has a credible path to sustaining more than 20% revenue growth and more than 30% compound annual growth rate in earnings per share over the medium term.

Western Digital Chief Financial Officer Kris Sennesael made the case at the J.P. Morgan 54th Annual Global Technology, Media and Communications Conference in May. He said the company now expects exabyte demand to grow at more than 25% annually over the next three to five years. That is up sharply from its February 2025 estimate of mid-teens growth.

Training large AI models requires storing enormous amounts of data. Inference, which Sennesael said will account for roughly two-thirds of AI compute in 2026, generates vast amounts of new output that companies want to retain. Add in physical AI, such as autonomous vehicles and robotics, and you have multiple converging demand drivers that all funnel back to storage.

"Every time we talk to them, the demand is stronger for longer," Sennesael said of Western Digital's hyperscaler customers.

Western Digital Is Positioned to Capture the Opportunity

WDC ships hard disk drives with an average capacity of about 23 terabytes per unit today. A next-generation product using enhanced perpendicular magnetic recording, or ePMR, is in qualification at the 40-terabyte level and expected to ramp in the second half of calendar year 2026.

Beyond that, Western Digital has spent the past decade developing heat-assisted magnetic recording, or HAMR, now in qualification with four customers. HAMR will launch at 44 terabytes in 2027, and the company has a road map extending to more than 100 terabytes per drive.

Western Digital can support 25% annual exabyte growth without adding unit manufacturing capacity. It does so through technology transitions that let it pack more storage onto each drive it ships.

Notably, the company shares technology road maps with hyperscalers, invites them to its factories, and has entered into long-term agreements with major customers covering calendar years 2027 and 2028, with some extending into 2029.

Western Digital's average selling price per terabyte rose 9% year-over-year last quarter. As drives get larger and more capable, WDC is expected to continue raising its per-terabyte charge.

What Is the WDC Stock Price Target?

Valued at a market cap of $181 billion, WDC stock is up 929% in the last 12 months. Analysts tracking WDC stock forecast revenue to rise from $9.52 billion in fiscal 2025 to $35 billion in fiscal 2030.

In this period:

- Adjusted earnings per share are forecast to expand from $4.93 to $52.16.

- Free cash flow is projected to improve from $1.28 billion to $14 billion.

If WDC stock is priced at 20x forward earnings, it could more than double within the next 40 months. Out of the 25 analysts covering WDC stock, 21 recommend “Strong Buy,” one recommends “Moderate Buy,” and three recommend “Hold.” The average WDC stock price target is $501, below the current price of $531.

The HDD industry has two dominant suppliers (three, if you count Toshiba's much smaller market share), and new entrants are virtually nonexistent, given the business' complexity and capital intensity. Demand tailwinds from AI training, inferencing, and physical AI appear durable rather than cyclical.

And Western Digital's dual-platform strategy, running ePMR and HAMR simultaneously, gives it more flexibility than a competitor focused entirely on a single recording technology.

Evercore ISI's revised target of $575 represents a considered reset based on direct management engagement, not a headline-chasing bump. For investors looking for AI infrastructure exposure beyond the obvious names, Western Digital deserves a closer look.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Autodesk%20Inc_%20Portland%20office-by%20hapabapa%20via%20iStock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)