/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)

As Wall Street continues pouring money into familiar artificial intelligence (AI) giants like Nvidia Corporation (NVDA), billionaire hedge fund Whale Rock Capital Management is quietly rotating toward a different corner of the AI trade.

In the first quarter, the tech-focused investment firm not only opened new positions in three lesser-known AI infrastructure plays, with $336 million worth of shares in Advanced Energy Industries (AEIS), nearly $180 million in Viavi Solutions (VIAV), and $394 million in MKS (MKSI), but also reduced its stake in Nvidia, signaling a shift away from crowded mega-cap winners and toward the companies powering the next phase of the AI buildout.

The moves, which total $910 million, suggest Whale Rock founder Alex Sacerdote sees greater upside in the suppliers enabling AI expansion rather than the dominant chipmakers already at the center of investor attention. AEIS provides advanced power systems used in semiconductor manufacturing and data centers, VIAV specializes in optical networking and communications testing equipment, while MKSI supplies critical photonics, vacuum, and process technologies embedded throughout the semiconductor supply chain.

Together, the bets reflect a broader thesis that the real beneficiaries of the AI arms race may increasingly be the companies building the infrastructure underneath it. Let’s dig deeper.

Stock #1: Advanced Energy Industries

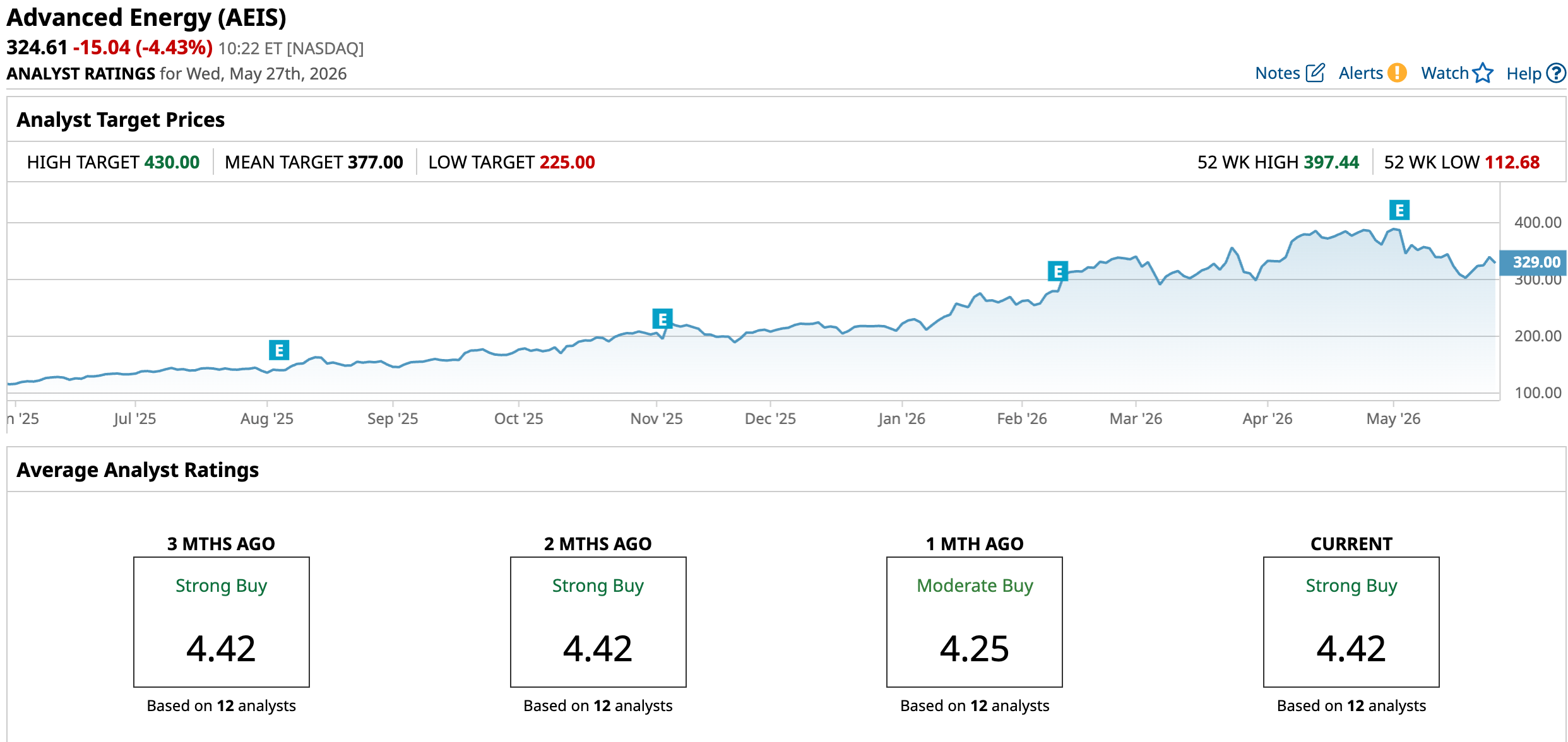

Based in Denver, Colorado, Advanced Energy Industries is a precision power conversion and control technology company that supplies critical systems used across semiconductor manufacturing, AI data centers, industrial equipment, telecommunications, and medical devices. The company has increasingly emerged as a key beneficiary of the AI infrastructure boom, particularly through its exposure to hyperscale data centers and advanced semiconductor manufacturing. Advanced Energy’s market cap currently sits at $12.92 billion.

AEIS has surged 177.67% over the past 52 weeks and 55.85% year-to-date (YTD), massively outperforming the broader S&P 500 Index’s ($SPX) 26.85% returns over the past year and 9.73% gains this year as investors rotate into AI infrastructure suppliers beyond the mega-cap chipmakers.

In terms of valuation, the stock trades at around 43.90 times forward earnings, reflecting a premium compared to industry peers and the historical average.

Advanced Energy released its first-quarter 2026 earnings on May 4, with results that topped Wall Street expectations. The company reported revenue of $511 million, representing a 26% year-over-year (YOY) increase, while non-GAAP earnings per share (EPS) came in at $2.09, up 70% from the prior year and ahead of analyst estimates. Management highlighted record data center computing revenue of $194.2 million during the quarter, which surged more than 100% YOY, driven by strong demand tied to AI computing infrastructure.

Additionally, management issued strong guidance, forecasting second-quarter 2026 revenue of $540 million, plus or minus $20 million, with non-GAAP EPS projected at $2.18, plus or minus $0.25. The company additionally raised its full-year 2026 revenue growth outlook to the low-to-mid-20% range, up from prior expectations for high-teen growth, while data center revenue growth is now expected in the mid-30% range.

Analysts tracking AEIS project the company’s profit to reach $7.65 per share in 2026, up 45.16% from the prior year.

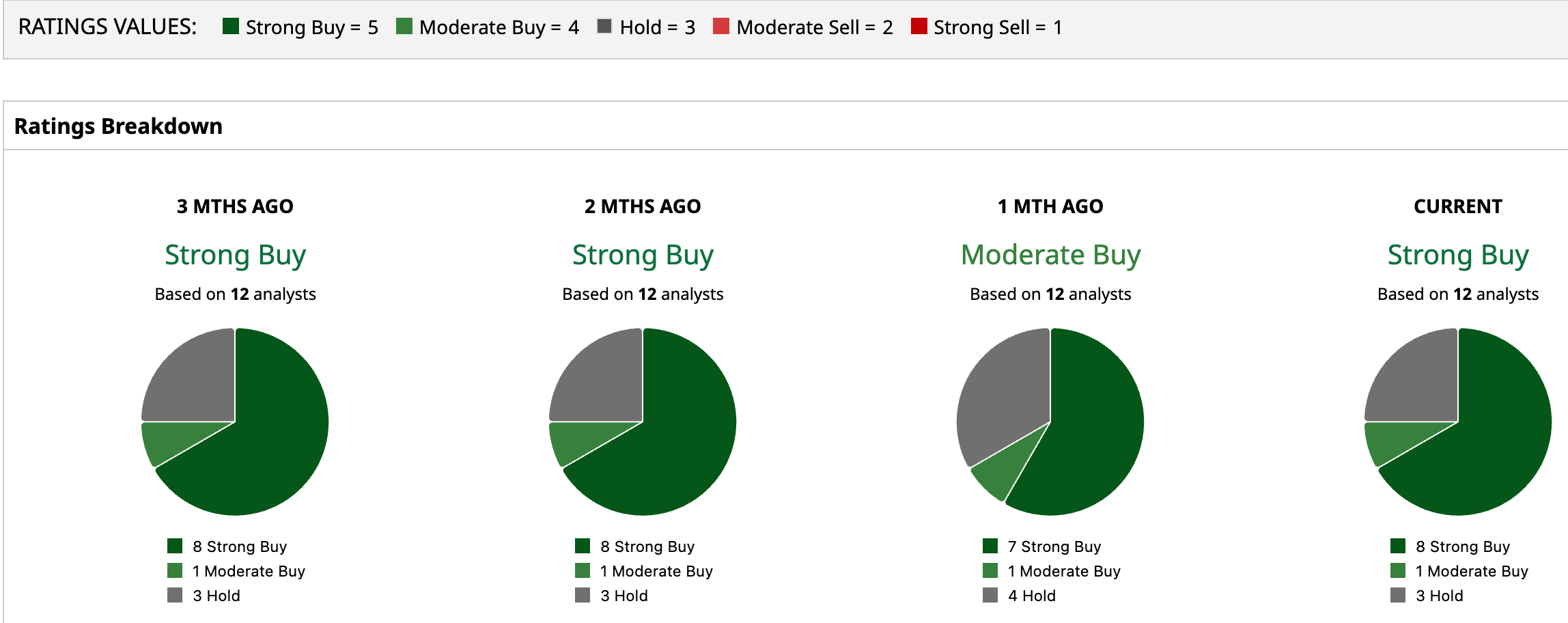

Wall Street’s outlook on the stock is optimistic, with a consensus “Strong Buy” rating overall. Of 12 analysts covering the stock, eight recommend a “Strong Buy,” one opts for a “Moderate Buy,” and the remaining three suggest a “Hold.”

The average analyst price target of $377 indicates potential upside of 16.14% from the current price levels. The Street-high price target of $430 suggests that AEIS could rally as much as 32.47% from here.

Stock #2: Viavi Solutions

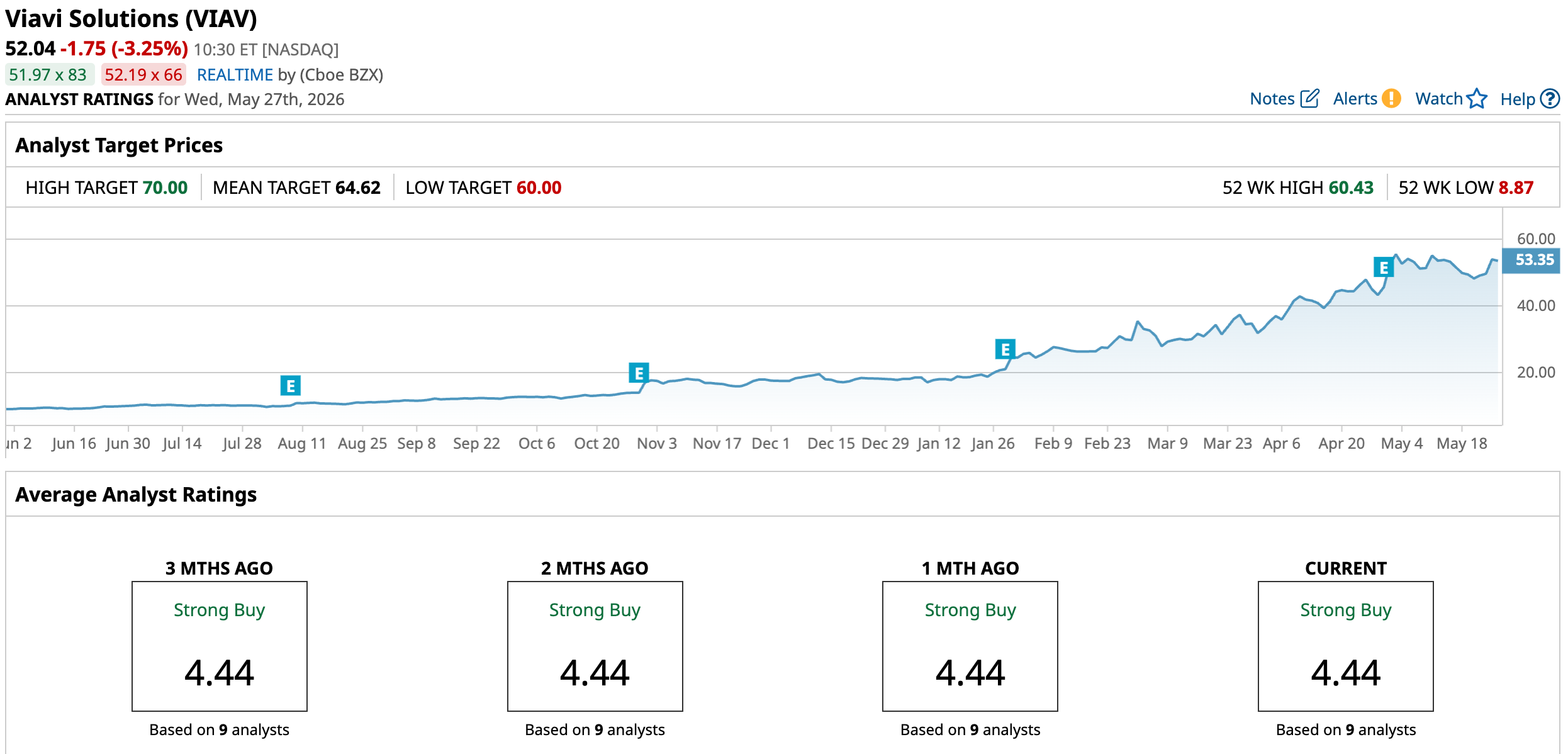

Based in Chandler, Arizona, Viavi Solutions is a network testing, optical technologies, and communications equipment company that provides critical solutions for telecom operators, cloud providers, aerospace and defense customers, and hyperscale data centers. The company has increasingly emerged as a key beneficiary of the AI infrastructure boom through its exposure to optical networking, data center connectivity, and high-speed network testing solutions used in next-generation AI systems. Viavi’s market cap currently sits at $12.58 billion.

VIAV shares have surged a staggering 463.74% over the past 52 weeks and are up nearly 192.31% YTD, dramatically outperforming the broader S&P 500 Index as investors flock into AI infrastructure names tied to optical networking and data-center buildouts.

Priced at approximately 67.59 times forward earnings, the stock trades at a premium valuation as Wall Street increasingly prices in accelerating AI-driven demand trends.

Viavi released its fiscal third-quarter 2026 earnings on April 29, delivering results that comfortably exceeded Wall Street expectations. The company reported revenue of $406.8 million, up 42.8% YOY, while non-GAAP EPS rose 80% YOY to $0.27. Non-GAAP operating income climbed 79.2% from the prior year to $85.5 million, while operating margin expanded 430 basis points YOY to 21%, reflecting strong operating leverage and improving profitability.

Moreover, the company’s core Network and Service Enablement segment generated $321.5 million in revenue during the quarter, surging 54.4% YOY, driven by strong demand from AI data centers, and aerospace and defense markets.

For the fiscal fourth quarter of 2026, Viavi guided revenue to a range of $427 million to $437 million and projected non-GAAP EPS between $0.29 and $0.31. Management also indicated that momentum across the data center ecosystem is expected to remain strong throughout the calendar year.

Analysts expect the company to deliver an EPS of $0.73 in fiscal 2026, up 143.3% YOY.

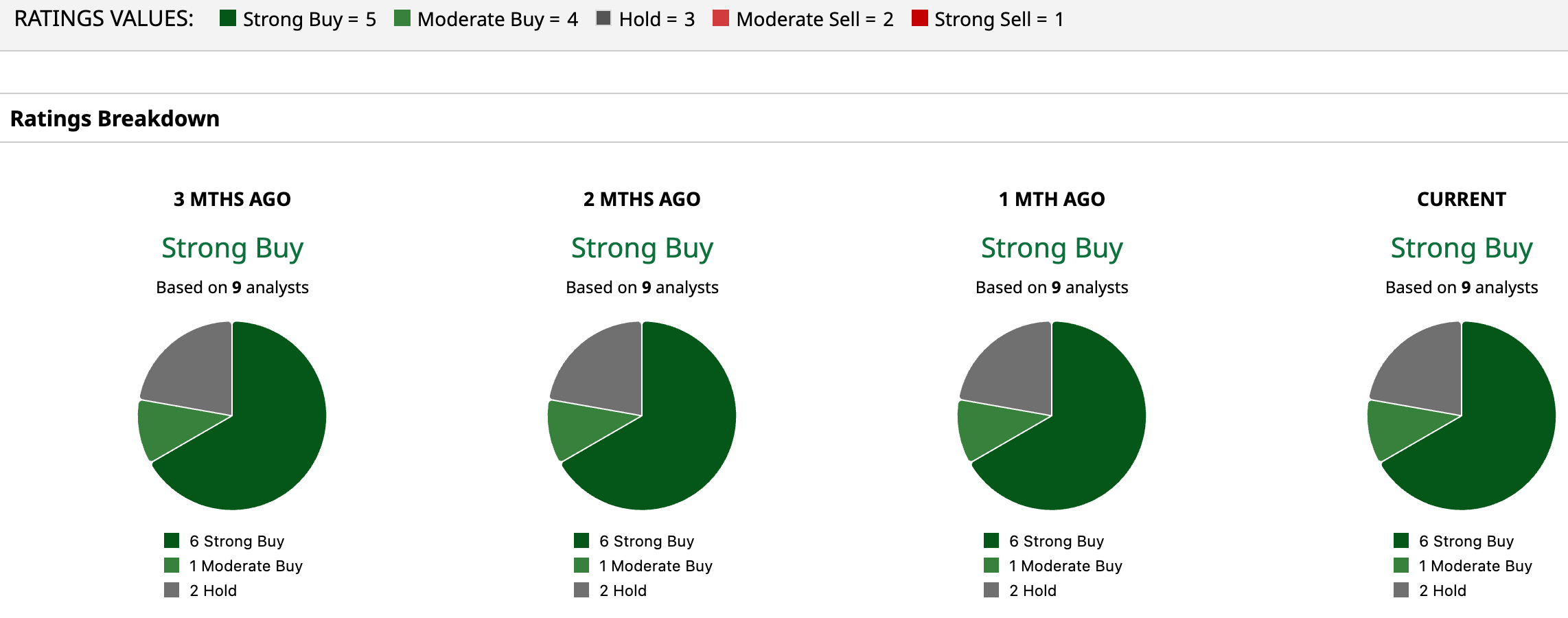

Wall Street is highly bullish overall, with a consensus “Strong Buy” rating for VIAV. Out of the nine analysts covering the stock, six recommend a “Strong Buy,” one advises a “Moderate Buy,” and the remaining two analysts are playing it safe with a “Hold.”

The average analyst price target of $64.62 indicates potential upside of 24.17% from the current price, while the Street-high target of $70 suggests that the stock could surge as much as 34.5%.

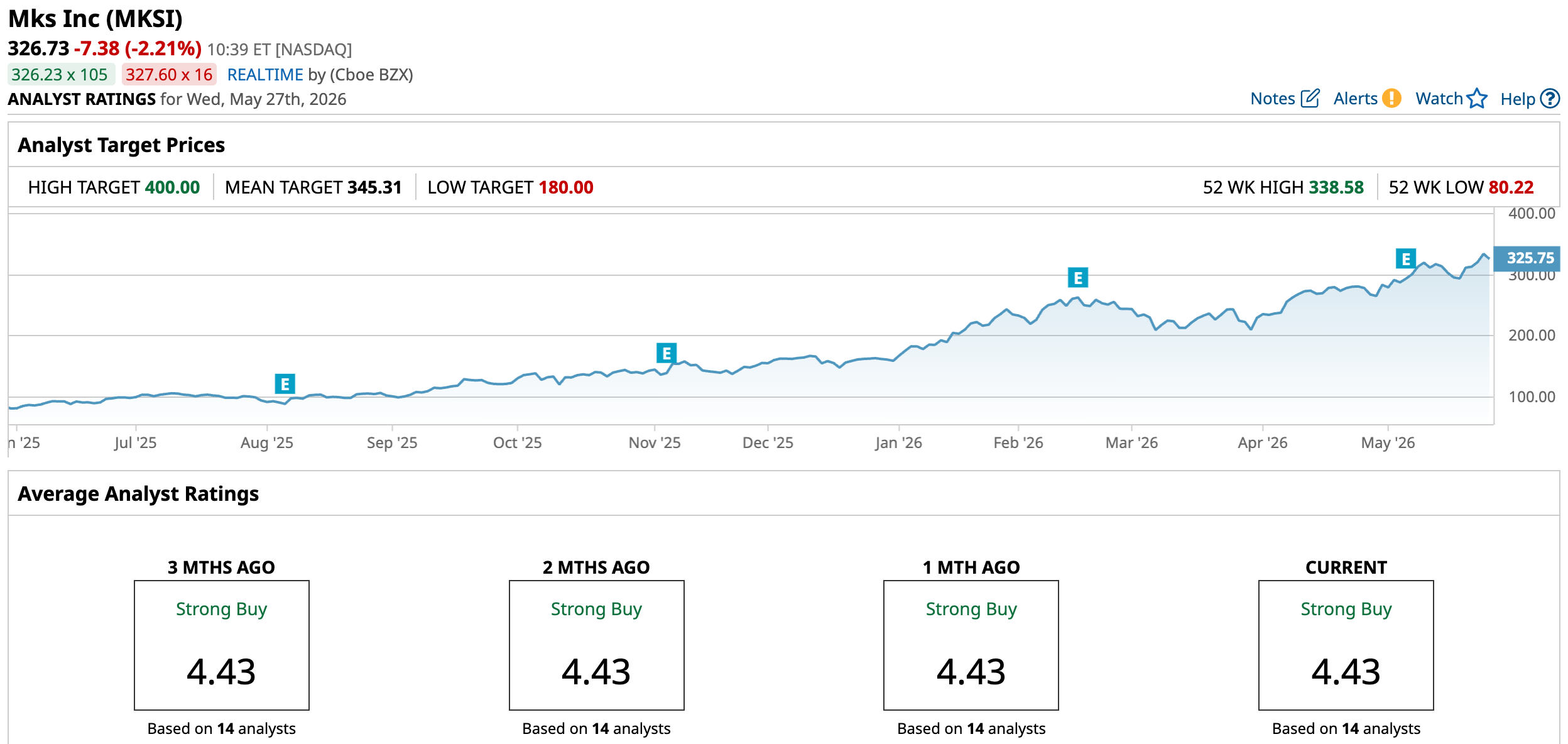

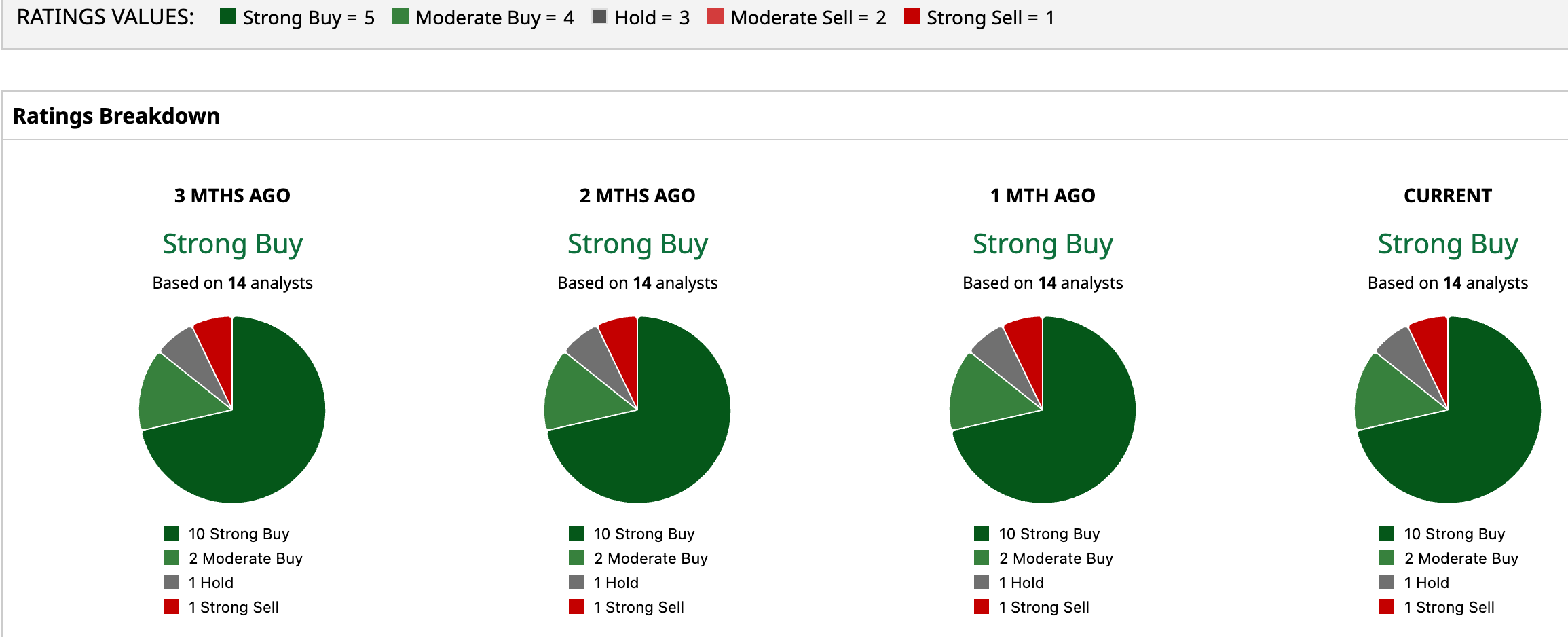

Stock #3: MKS

Based in Andover, Massachusetts, MKS is a semiconductor equipment and advanced manufacturing technology company that provides critical subsystems, process control solutions, lasers, photonics, vacuum technologies, and specialty chemicals used across semiconductor fabrication, AI data centers, industrial automation, and electronics manufacturing.

The company has increasingly emerged as a major beneficiary of the artificial intelligence infrastructure boom through its deep exposure to advanced semiconductor manufacturing and high-performance computing supply chains. MKS Instruments’ market cap currently sits $22.6 billion.

MKSI shares have surged 277.76% over the past 52 weeks and are up 106.73% this year, beating the broader market.

Trading at 28.77 times forward earnings, the stock commands a premium valuation relative to peers as Wall Street prices in accelerating AI-driven semiconductor demand.

MKS released its first-quarter 2026 earnings on May 6. The company reported revenue of $1.08 billion, representing a 15.2% YOY increase, while non-GAAP EPS climbed to $2.30, up from the year-ago quarter value of $1.71. Its adjusted EBITDA increased 17.4% YOY to $277 million, reflecting improving operating leverage and stronger semiconductor demand trends.

The company’s Semiconductor Market segment remained the primary growth driver during the quarter, with revenue rising to $466 million, fueled by increasing demand tied to AI accelerators, advanced memory, and high-bandwidth computing infrastructure.

For the second quarter of 2026, MKS guided revenue to a range of $1.2 billion, plus or minus $40 million and projected non-GAAP EPS of $2.90, plus or minus $0.30. Management noted that AI-driven investments by hyperscalers and chip manufacturers continue to support stronger long-term demand visibility across the company’s portfolio.

In addition, analysts expect fiscal 2026 EPS growth of 46.5% YOY to $11.54.

The stock has a consensus “Strong Buy” rating overall. Among the 14 analysts covering the stock, 10 recommend a “Strong Buy,” two advise a “Moderate Buy,” one suggests a “Hold,” and one opts for a “Strong Sell.”

While the average analyst price target of $345.31 indicates potential upside of 5.7%, the Street-high price target of $400 suggests that the stock could rally as much as 22.43% from here.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Close-%20up%20of%20computer%20chip%20with%20AI%20sign%20by%20YAKOBCHUK%20V%20via%20Shutterstock.jpg)