/NVIDIA%20Corp%20logo%20on%20phone%20and%20AI%20chip-by%20Below%20the%20Sky%20via%20Shutterstock.jpg)

Semiconductor industry behemoth Nvidia Corporation (NVDA) has delivered solid gains of almost 20% this year. However, investors seem to have higher expectations for the company, given its track record and the fact that one of its rivals in the AI space, Advanced Micro Devices (AMD), has gained 96.7% this year.

However, this fact did not stop Chase Coleman’s Tiger Global, one of the most closely watched hedge funds, from increasing its Nvidia holdings by one million shares, from 11,011,752 to 12,011,752. Such robust institutional buying could raise investor confidence and drive the stock higher.

Nvidia is facing exponential demand for computing, especially in a rapidly evolving space driven by the growing popularity of agentic AI. The company remains central to this growing phenomenon, as its chipsets remain highly coveted. Its Grace Blackwell platform and NVLink offering have become central to inference. Its Vera Rubin platform is set to join this list, as AI agents continue to be rapidly adopted.

We take a closer look at Nvidia now before the company’s Q1 earnings.

About Nvidia Stock

Nvidia has emerged as the world’s most valuable company, driven by its dominance in artificial intelligence and high‑performance computing. The firm’s powerful GPUs and AI platforms power data centers, cloud services, and cutting‑edge applications, making it a central player in the global technology landscape and the engine behind the ongoing AI revolution. The company commands a massive market capitalization of $5.38 trillion.

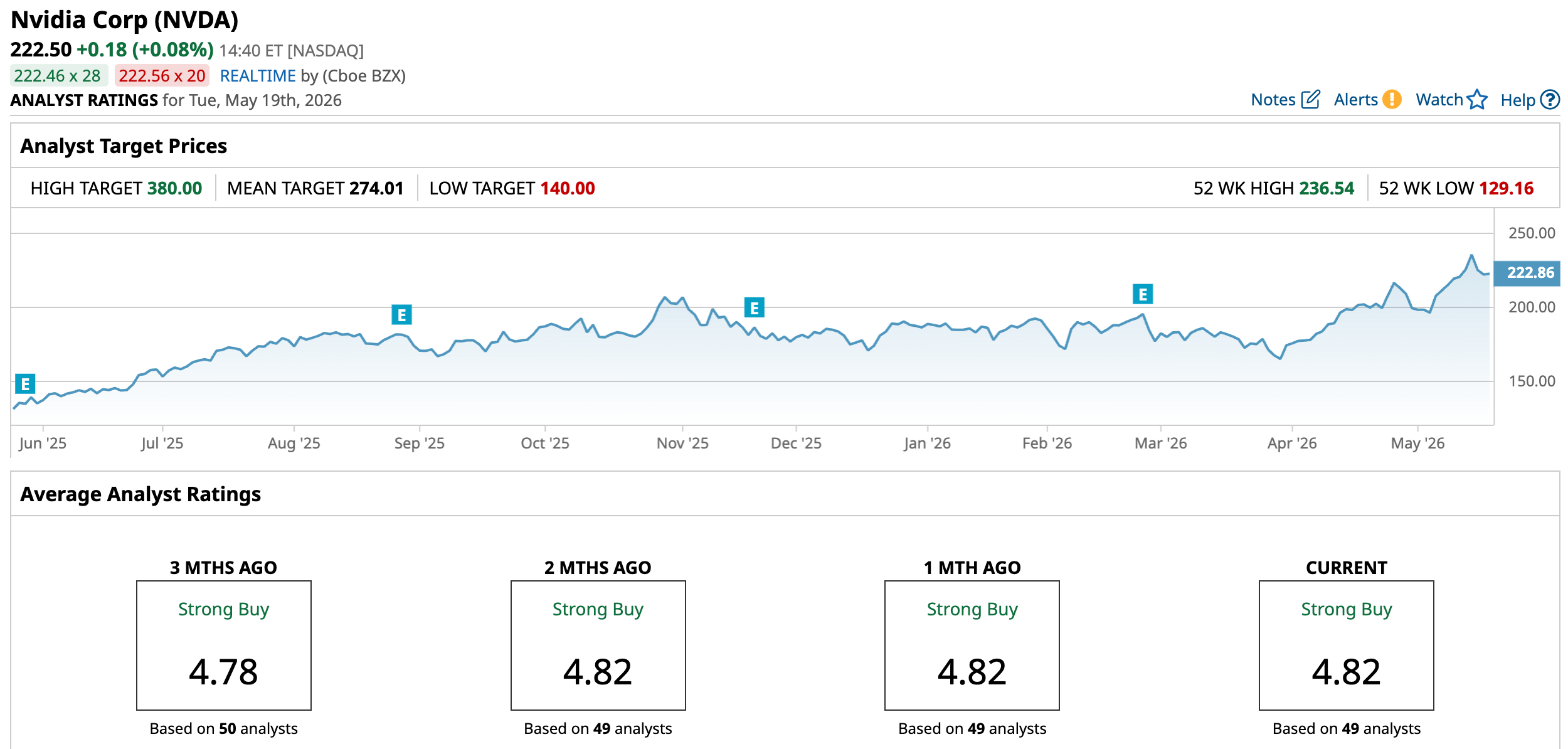

Unrelenting AI demand is still creating tailwinds for Nvidia’s stock. Explosive demand for Nvidia's GPUs is driving a huge surge in data center operations. As the company’s dominance persists, over the past 52 weeks, the stock has gained 64.73%, while it has been up 19.74% year-to-date (YTD). Powered by the strong demand for AI infrastructure and as compute supply remains constrained, NVDA’s stock reached an all-time high of $236.54 on May 14, but is down 5.78% from that level.

On a forward basis, NVDA’s price-to-earnings (non-GAAP) ratio of 28.75 times is 18% higher than the 24.36 times industry average.

Nvidia Q4 Earnings Beat as AI Demand Fuels Record Revenue

For the fourth quarter of fiscal 2026 (quarter ended Jan. 25), Nvidia reported a record quarterly revenue of $68.13 billion, up 73% year-over-year (YOY), which was also higher than the $66.21 billion that Wall Street analysts (as polled by LSEG) had expected. The company’s Q4 data center revenue reached a record $62.30 billion, up 75% from the year-ago period. This clearly shows that Nvidia is now earning about 91% of its top line from data center operations.

Profitability jumped as the top-line growth translated into bottom-line gains. Nvidia’s non-GAAP operating income increased 81% YOY to $46.11 billion, while non-GAAP EPS grew 82% to $1.62, topping analysts’ expectations of $1.53. The company issued better-than-expected guidance, expecting a Q1 FY2027 revenue of $78 billion, plus or minus 2%.

Wall Street analysts are robustly optimistic about Nvidia’s future earnings. They expect the company’s EPS to climb by 120.8% YOY to $1.70 for Q1 FY2027 (to be reported on May 20, after the market closes). For fiscal 2027, EPS is projected to surge 71.8% annually to $7.85, followed by 33.9% growth to $10.51 in fiscal 2028.

What Do Analysts Think About Nvidia Stock?

Recently, analysts at TD Cowen maintained a “Buy” rating on Nvidia’s stock, while raising the price target from $235 to $275. The firm's Joshua Buchalter cited the company’s solid fundamentals and hyperscale capital expenditure expansion, in which Nvidia captures the majority. TD Cowen expects Nvidia to meet or surpass its usual quarterly sales beat of roughly $1 billion to $2 billion.

RBC Capital analysts reiterated an “Outperform” rating and a $250 price target. Analysts at the firm believe that Nvidia is better positioned to address component shortages and power and infrastructure constraints, and they also view the company’s balance sheet strength as a structural advantage.

Cantor Fitzgerald analysts raised the price target from $300 to $350, while maintaining an “Overweight” rating. The firm pointed to extremely constrained compute supply, noting that Nvidia’s capacity is fully booked through 2026 and 2027. Agentic AI, driven by the launch of Clawdbot and underpinned by sturdy token demand at Anthropic and OpenAI over the past three months.

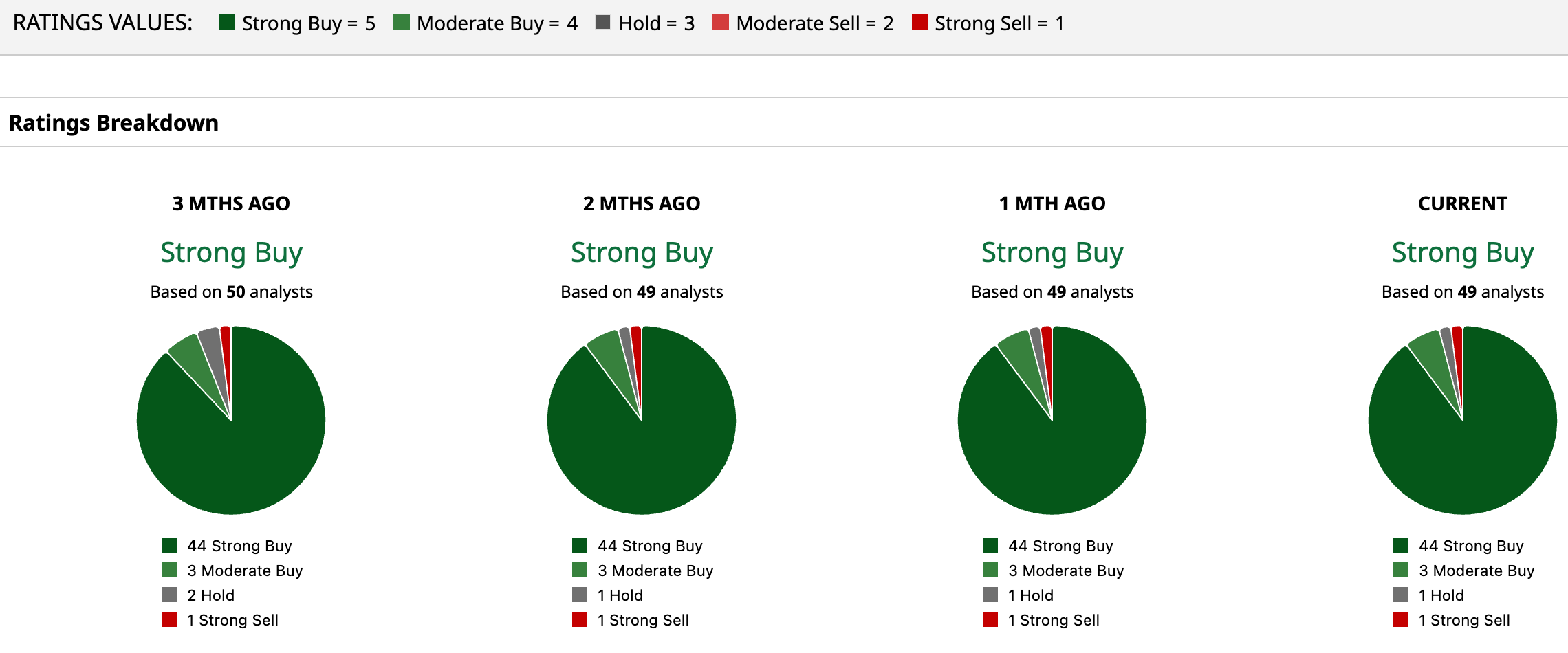

Nvidia has been in the spotlight on Wall Street for some time now, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 49 analysts rating the stock, a majority of 44 rate it a “Strong Buy,” three rate it a “Moderate Buy,” one analyst takes the middle-of-the-road approach with a “Hold,” and only one analyst gives it a “Strong Sell” rating. The consensus price target of $274.01 represents 23.15% upside from current levels. Moreover, the Street-high price target of $380 indicates a 70.8% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)

/A%20close-up%20of%20the%20SpaceX%20sign%20on%20a%20black%20building%20by%20IanDewarPhotography%20via%20Adobe%20Stock.jpeg)