/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

The artificial intelligence (AI) infrastructure boom has minted a new class of market winners, and Micron stock is one among them. Over the past year, Micron (MU) shares have skyrocketed more than 729%, turning a $10,000 investment into nearly $83,000.

As companies pour billions into AI data centers, advanced chips alone are not enough. AI models require enormous amounts of high-bandwidth memory and ultra-fast storage to process and train increasingly complex workloads. That surge in demand has positioned Micron as one of the top beneficiaries of the AI revolution.

Micron’s advanced memory solutions are becoming essential for hyperscale data centers powering large language models, cloud AI services, and enterprise AI deployments. At the same time, broader industry conditions are amplifying Micron’s momentum.

Global memory supply remains constrained, giving manufacturers stronger pricing power just as demand accelerates. That combination has significantly improved Micron’s profitability and strengthened earnings growth, helping drive investor optimism around the stock.

Looking ahead, the outlook for Micron stock remains strong as demand is likely to outpace supply. At the same time, Micron still looks attractively valued relative to its earnings growth potential.

Micron’s Explosive Growth Is Far from Over

Micron has delivered solid growth over the past several quarters, and the favorable demand and supply environment suggests that its growth is accelerating. The memory-chip maker is rapidly transforming into an important infrastructure supplier powering AI computing.

After delivering a blockbuster fiscal Q2, management guided for another solid quarter, with revenue expected to reach approximately $33.5 billion, up roughly 40% sequentially and nearly 300% year-over-year. AI servers, hyperscale cloud platforms, and next-generation data centers require significant amounts of high-performance memory. High-bandwidth memory (HBM), advanced DRAM, and enterprise SSDs are becoming essential infrastructure for AI computing, supporting Micron’s growth.

At the same time, industry supply remains constrained. That imbalance between surging AI demand and limited supply is creating one of the strongest pricing environments the memory market has seen in years. This is leading to extraordinary profitability for Micron.

Micron expects gross margins to surge to 81% in Q3, compared with just 39% a year ago. This follows an already exceptional 75% gross margin in Q2. Meanwhile, management expects Q3 earnings of approximately $19.15 per share, up from $1.91 per share in the same quarter last year. Higher pricing, manufacturing efficiencies, and a richer mix of AI-focused memory products are translating into solid revenue and earnings for the company.

Another catalyst supporting Micron’s investment appeal is its focus on multi-year strategic agreements. Historically, memory companies suffered from poor visibility due to highly cyclical demand and volatile pricing. But AI infrastructure spending is creating a different dynamic. Micron is increasingly signing multi-year strategic agreements related to long-term AI deployments.

If that transition continues, Micron could command structurally higher margins, stronger pricing power, and more durable earnings.

Micron’s Valuation Leaves Room for More Growth

Shares of Micron Technology have already delivered impressive gains, but the company’s valuation suggests the rally may be far from over. Despite the strong upward move in MU stock, investors are still paying a relatively modest price compared to the company’s accelerating earnings outlook.

Micron stock currently trades at around 13.3x forward earnings, a level that appears attractive given the company’s solid growth potential. Analysts expect Micron’s profits to skyrocket by 652.7% in 2026, followed by another robust increase of 71.6% in fiscal 2027. Micron’s explosive earnings growth and a relatively conservative valuation multiple strengthen the case for continued upside in the stock.

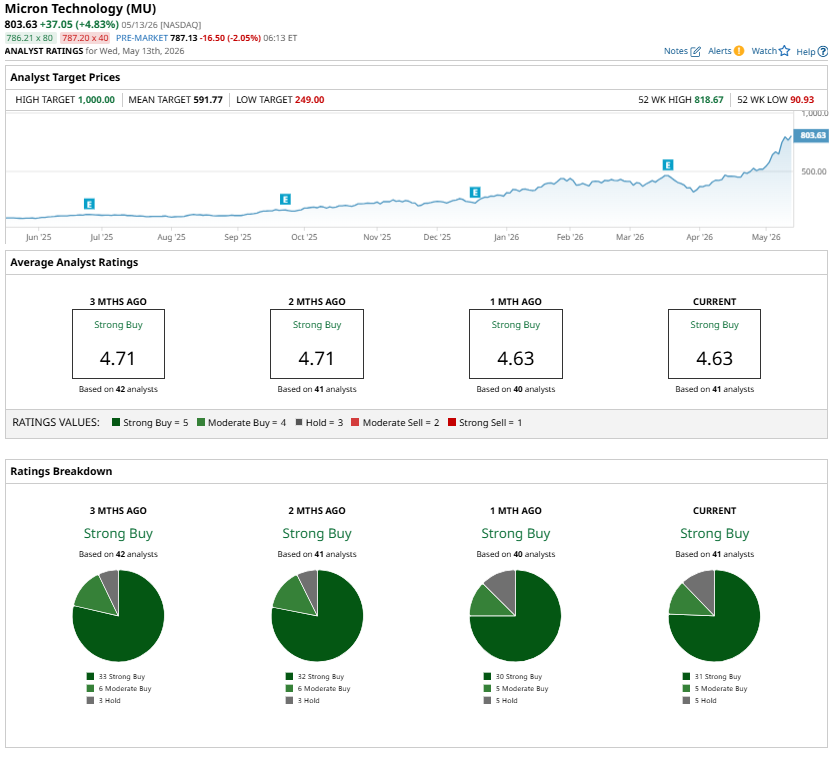

Analysts broadly maintain a “Strong Buy” consensus rating, reflecting optimism that the company is well-positioned to benefit from sustained demand for high-performance memory products in the years ahead.

The Street's high price target of $1,000 implies over 24% upside from its recent close of $803.63.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)