/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

Lumentum Holdings (LITE) is about to get a major visibility boost. The company recently confirmed that it will join the Nasdaq-100 Index before market open on Monday, May 18. For investors paying attention, this is a big deal.

Why? The index inclusion signals that one of the most important players in AI infrastructure is finally getting the recognition it deserves. Here's what investors should know.

Why Lumentum's Nasdaq-100 Inclusion Matters for Investors

Joining the Nasdaq-100 means accelerated buying by index funds and exchange-traded funds (ETFs) tracking the benchmark. Billions of dollars in passive investment money flow through those funds. When a company gets added, demand for its stock tends to rise, at least in the short term.

But the real story here goes well beyond index mechanics.

"Lumentum's inclusion in the Nasdaq-100 underscores the critical role our optical products play in AI-driven infrastructure," said President and CEO Michael Hurlston, according to a company statement. Hurlston pointed to co-packaged optics, optical circuit switches, and 200G lasers as technologies the world is only beginning to adopt.

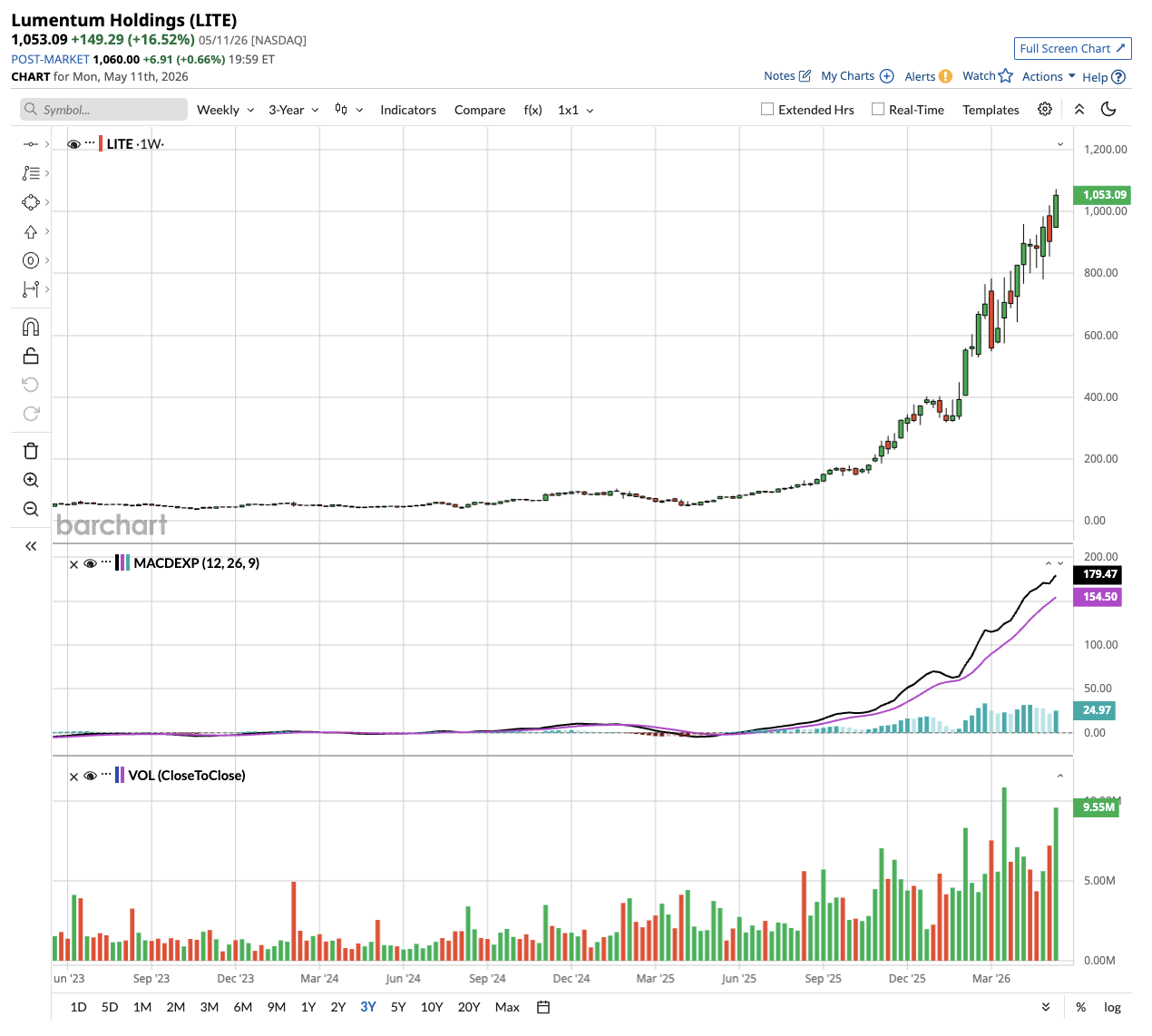

Valued at a market capitalization of more than $77 billion, LITE stock is up by 1,280% in the past year and has comfortably crushed broader market returns.

Lumentum Delivered a Record-Breaking Quarter

In its fiscal third quarter of 2026, Lumentum posted revenue of $808 million, marking a 90% year-over-year (YOY) jump. The company's non-GAAP operating margin also expanded by more than 2,100 basis points YOY to 32.2%, indicating strong operating leverage.

Two business segments drove the results. For one, components brought in $533 million, up 77% YOY. This includes pump lasers and narrow linewidth laser assemblies. On top of that, the systems segment generated $275 million in revenue, up 121% YOY, fueled by soaring demand for high-speed cloud transceivers.

In Q3, non-GAAP EPS came in at $2.37, which was ahead of expectations.

For the fourth quarter, management guided for revenue between $960 million and $1.01 billion. The midpoint of $985 million would represent sequential growth of roughly 22%.

The AI Infrastructure Play Most Investors Overlook

Lumentum sits at an intersection of AI spending that most investors haven't fully priced in yet.

Hyperscalers such as Alphabet (GOOGL), Amazon (AMZN), and Microsoft (MSFT) are running out of space and power inside individual data centers. So, they're building distributed architectures that link multiple data centers across different locations, which requires massive amounts of optical hardware to keep data moving at the speed of light.

Lumentum supplies the components that make this possible — pump lasers, narrow linewidth assemblies, and wavelength-selective switches that act as "optical traffic cops," routing enormous volumes of data without slowing it down.

Demand for these products is outpacing supply by more than 30%, according to management. That supply-demand gap isn't closing anytime soon, either. In fact, CEO Michael Hurlston said on the Q3 earnings call that the imbalance has widened since the previous quarter.

Meanwhile, Nvidia (NVDA) recently made a direct investment in the company, injecting roughly $2 billion into Lumentum's balance sheet during Q3.

A $2 Billion Quarterly Revenue Goal

Management has publicly set a goal of reaching $2 billion in quarterly revenue. Given that the company just crossed $808 million, that goal might sound ambitious. But investors should consider what's still early-stage or barely ramping for the company.

On the optical circuit switches (OCS) front, Lumentum has secured a “multi-year, multi-billion dollar purchase agreement” and expects meaningful contributions to accelerate in the second half of 2026. For co-packaged optics (CPO), a new Greensboro, North Carolina, fab acquired in mid-March is being converted to support this product line, with revenue contributions expected starting in early 2028. Finally, 1.6T transceivers shipments are set to ramp in fiscal Q4 with better margins.

That said, supply-chain constraints, execution challenges on new product ramps, and competition from China are all legitimate concerns that management flagged.

What Do Analysts Think of LITE Stock?

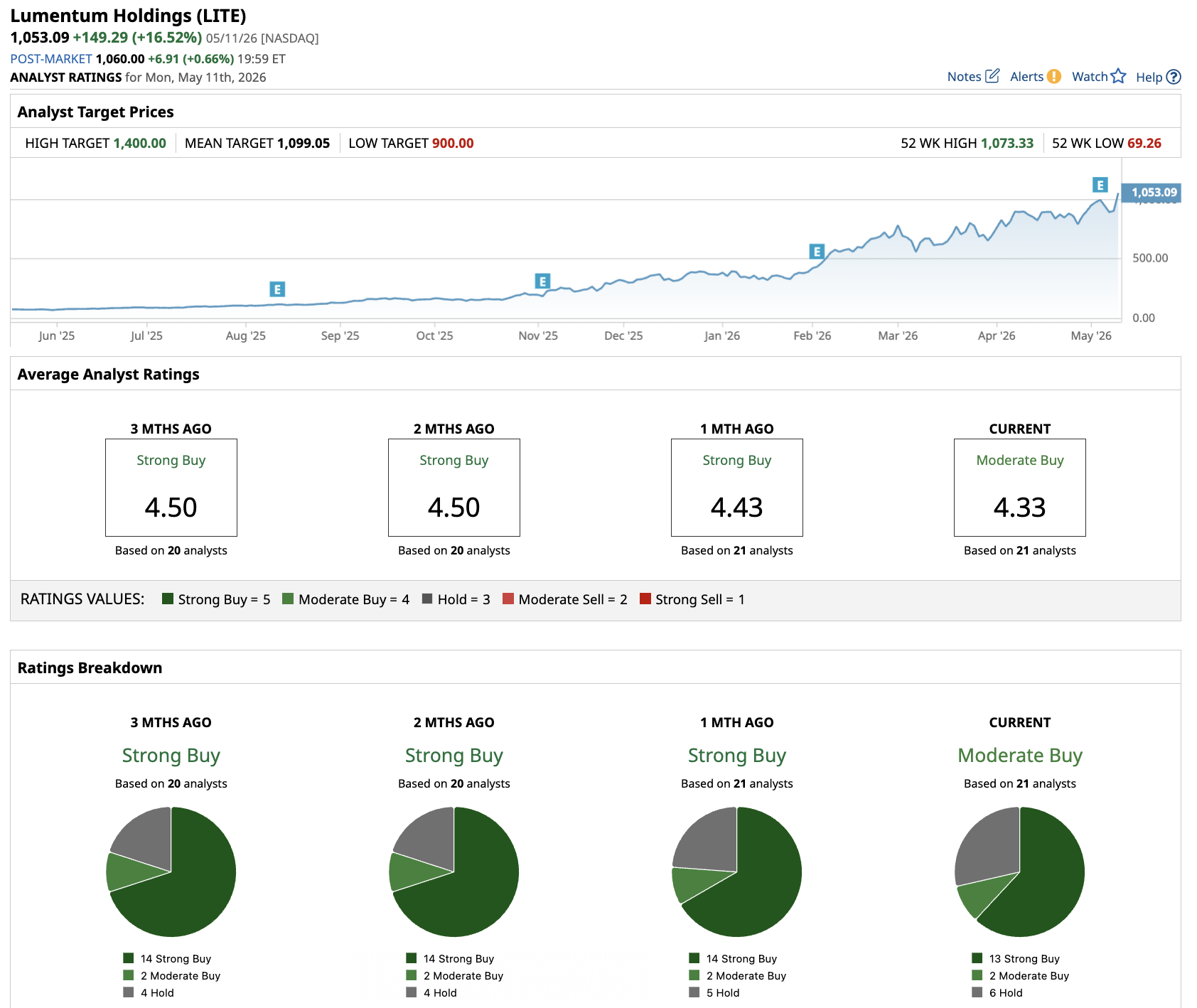

Overall, analysts have a consensus “Moderate Buy” rating on Lumentum. Out of the 21 analysts covering LITE stock, 13 recommend a “Strong Buy,” two recommend a “Moderate Buy,” and six recommend a “Hold” rating. The average price target is $1,099.05, which represents 7% potential upside from current levels.

Lumentum is not a speculative bet on some distant AI future. It's a company already generating record revenue, expanding margins at a remarkable pace, and sitting at the center of infrastructure spending that isn't slowing down.

The Nasdaq-100 inclusion on May 18 is the headline. But the real reason to pay attention to LITE stock is what's underneath this news: a business firing on nearly every cylinder, with several major growth drivers that have barely gotten started.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)