/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

CoreWeave (CRWV), headquartered in Livingston, New Jersey, is a specialized cloud infrastructure provider purpose-built for large-scale artificial intelligence (AI) and machine learning workloads. Founded in 2017 and publicly listed on the Nasdaq in March 2025, the company has pivoted from its origins in cryptocurrency mining to become a dominant "hyperscaler" for the AI era.

As a key partner for leaders like Meta (META), OpenAI, and Anthropic, CoreWeave provides the critical "compute power" necessary to drive the global generative AI revolution.

CoreWeave Stock Outshines Market

Following its successful IPO in 2025, the stock has remained a favorite for AI-growth investors, though it has experienced significant volatility typical of high-growth tech. While shares are up over 62% year-to-date in 2026, they are currently consolidating from a 52-week high of $187. This rally is underpinned by massive institutional confidence, including a $2 billion equity investment from Nvidia (NVDA), though high capital expenditures and rising debt levels to fund data center expansion remain key points of scrutiny for long-term valuation.

Compared to the Nasdaq Composite ($NASX), CoreWeave has been a standout performer, significantly outpacing the tech-heavy index. Over the past 12 months, CRWV has climbed 125%, more than tripling the gains of the broader Nasdaq. This extreme outperformance highlights its status as a concentrated "pure play" on AI infrastructure demand.

CoreWeave's First Quarter Results

CoreWeave reported explosive growth for the first quarter on May 7, with total revenue surging 112% year-over-year to $2.1 billion. This comfortably beat analyst estimates of $1.97 billion, driven by robust demand for its specialized AI cloud platform. However, the company’s aggressive expansion strategy led to a GAAP net loss of $740 million, or -$1.40 per share, wider than the $315 million loss in the prior year.

Despite the net loss, the company’s operational efficiency remained visible, with adjusted EBITDA reaching $1.2 billion at a healthy 56% margin. The most significant highlight was the revenue backlog reaching a record $99.4 billion, a 284% increase from the first quarter of 2025.

Looking ahead, management has set an ambitious target of over $30 billion in annualized revenue by the end of 2027, with 75% of that goal already secured under long-term contracts. To support this trajectory, CoreWeave is executing a capital-intensive plan, with Q1 capital expenditures alone reaching $7.7 billion.

The company recently secured a $21 billion multi-year agreement with Meta and expanded its partnership with Anthropic, solidifying its role as a primary infrastructure provider for the world’s leading AI model developers.

The $100 Billion Reason

CoreWeave shares slipped 8% premarket on Friday and ending the day 4% on the red following a second-quarter revenue outlook that missed expectations, shifting significant pressure onto the company's second-half performance. Despite the conservative guidance and rising capital expenditure projections due to component pricing, analysts from Wells Fargo and Jefferies remained bullish, maintaining "Overweight" and “Buy” ratings with price targets of $155 and $160, respectively, with an upside potential of 34% to 40%.

This optimism is anchored by a record $99.4 billion revenue backlog, which includes over $40 billion in new commitments and a diversifying customer base, with 10 clients now committing to over $1 billion each.

Operationally, the company continues to see resilient pricing across NVIDIA’s GPU generations, including Blackwell and Hopper, as inference demand broadens. While investors expressed concern over the steep ramp required to meet full-year adjusted EBIT targets, analysts noted that CoreWeave’s 1GW+ of active capacity and five-year average contract durations provide strong long-term visibility. With near-term fleet capacity remaining sold out and the revenue backlog converging with performance obligations, Wall Street may view the current dip as a minor hurdle within a multi-trillion-dollar AI infrastructure buildout.

Should You Buy CRWV?

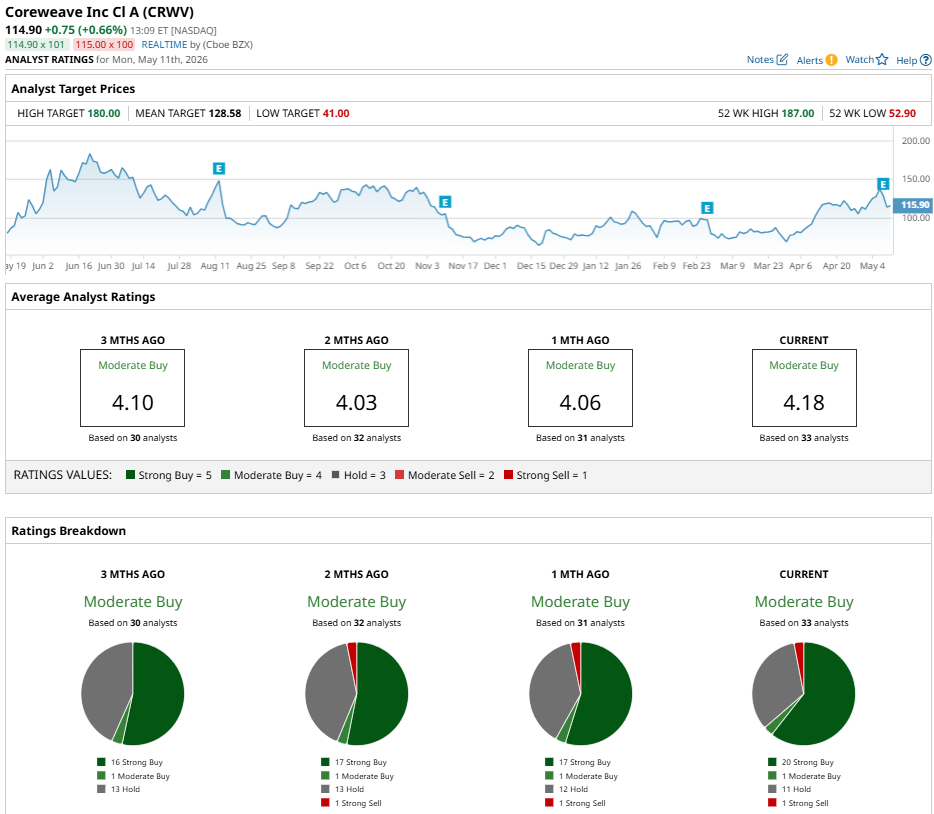

CoreWeave’s record-breaking $99.4 billion backlog serves as a massive buffer against near-term volatility, signaling long-term dominance in AI infrastructure. The stock currently holds a consensus "Moderate Buy" rating, supported by 21 "Buy" or "Strong Buy" designations from 33 analysts. With a recent mean price target of $128.58, CRWV offers a projected 11% upside from its current price.

While the recent revenue outlook miss and heavy capex requirements pose risks, the company’s strategic NVIDIA partnership and sold-out fleet capacity make it a compelling choice for investors seeking pure-play AI exposure.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)