Since November 2025, Black Stone Minerals has been in a holding pattern, posting a small loss of 1.1% while floating around $13.51. The stock also fell short of the S&P 500’s 10% gain during that period.

Is there a buying opportunity in Black Stone Minerals, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Black Stone Minerals Not Exciting?

We don't have much confidence in Black Stone Minerals. Here are two reasons you should be careful with BSM and a stock we'd rather own.

1. Fewer Distribution Channels Limit its Ceiling

The scale of a company’s revenue base is an important lens through which to view the topline, as it signals whether a producer has gone from a vulnerable commodity taker into a durable operating platform. Larger producers generate revenue across many wells, pads, takeaway routes, and geographies rather than relying on a single field or drilling program.

Black Stone Minerals’s $470 million of revenue in the last year is pretty small for the industry, suggesting the company hasn’t hit a level of diversification where investors can sleep easy at night.

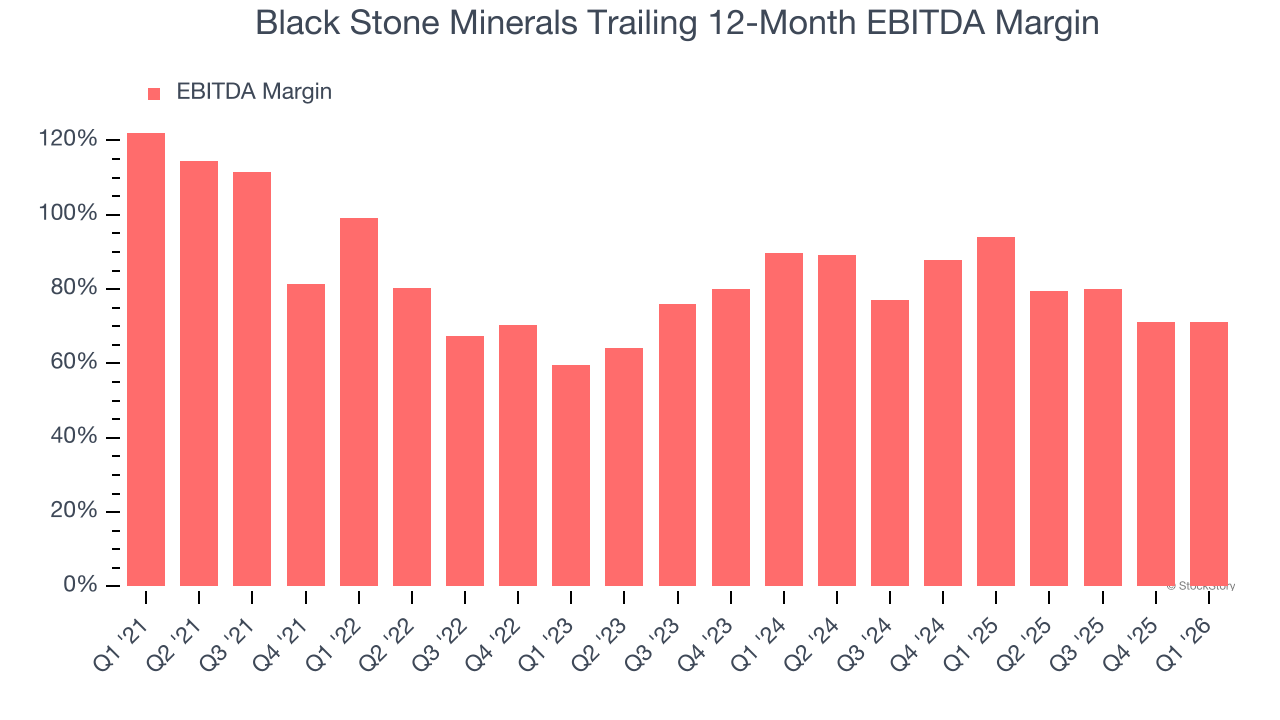

2. Shrinking EBITDA Margin

Adjusted EBITDA margin is an important measure of profitability for the sector and accounts for the gross margins and operating costs mentioned previously. Unlike operating margin, it is not distorted by accounting conventions around reserves, drilling costs, and assumptions on commodity consumption from the well or basin. Adjusted EBITDA highlights the economic reality of how much cash the rock produces before the capital structure (debt service) and the drilling budget (capex) are considered.

Analyzing the trend in its profitability, Black Stone Minerals’s EBITDA margin decreased by 28.1 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its EBITDA margin for the trailing 12 months was 71.1%.

Final Judgment

Black Stone Minerals’s business quality ultimately falls short of our standards. With its shares lagging the market recently, the stock trades at 12.9× forward P/E (or $13.51 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at an all-weather company that owns household favorite Taco Bell.

Stocks We Like More Than Black Stone Minerals

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)