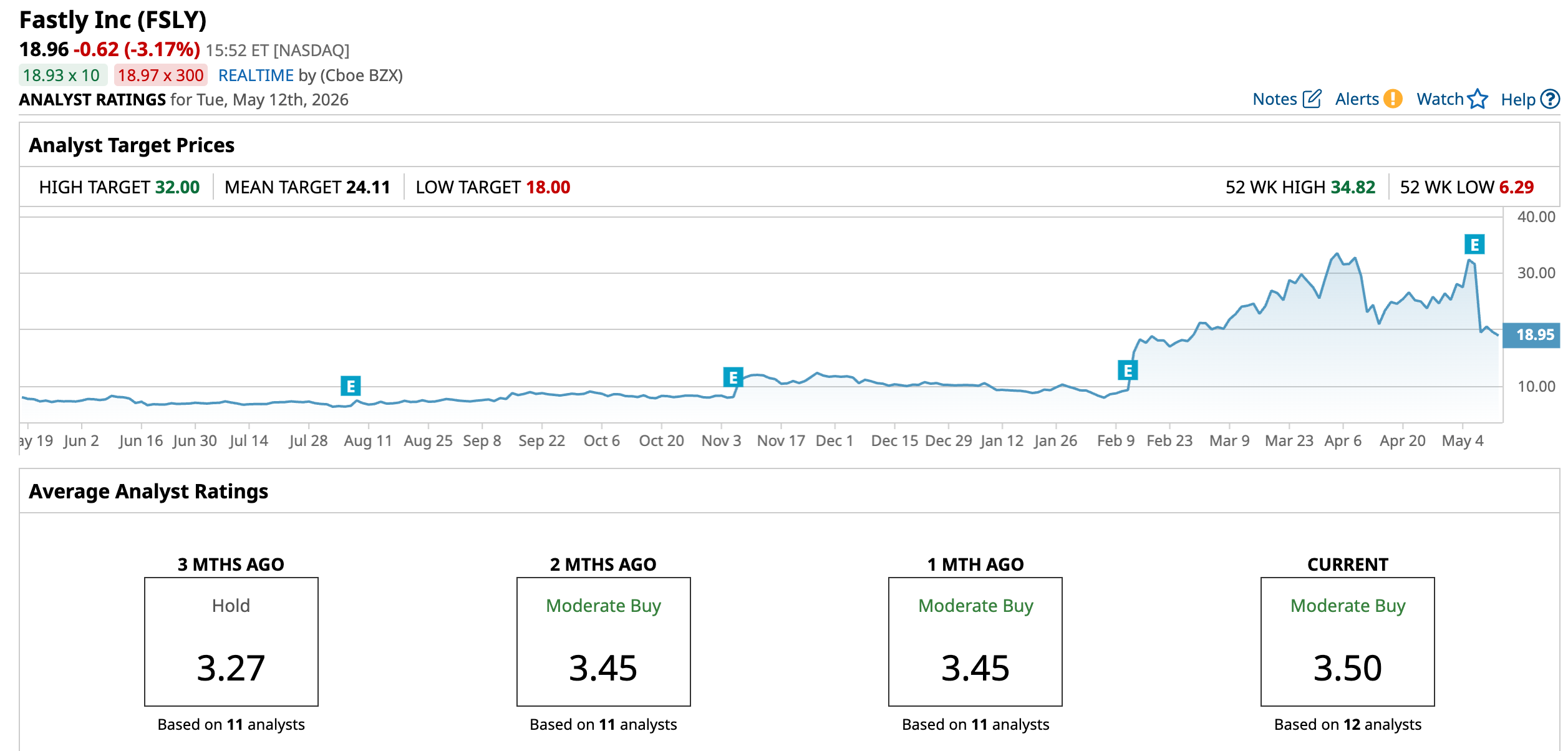

Content delivery network (CDN) company Fastly (FSLY) has been a volatile investment this year. After a 72.3% intraday jump on Feb. 12, the stock is up more than 85% this year. However, after posting its Q1 results, it has dropped 38.2% on May 7. The results were quite robust, with the company reporting record quarterly revenue and RPO, and even reporting an adjusted profit.

However, despite these better-than-expected results and the management’s guidance raise, Fastly took the blow as it failed to meet investors’ lofty expectations. The market seemed to be looking for even stronger performance than the company reported.

However, there's much to look forward to with Fastly.

About Fastly Stock

Headquartered in San Francisco, California, Fastly operates as an edge cloud platform provider that empowers developers to build, secure, and deliver digital experiences at scale. The company specializes in content delivery networks, edge computing, and security services, enabling real-time processing and programmable infrastructure close to end users for faster web applications.

From its central hub, which houses engineering, product, sales, and leadership teams, Fastly supports global operations to help businesses like media sites and e-commerce platforms thrive online. The company has a market capitalization of $3.06 billion.

Agentic and autonomous AI agents have boosted edge computing demand, positioning Fastly to handle traffic surges from large language models, driving a sharp rise in the company’s stock.

Over the past 52 weeks, the stock has gained 132.84%, while it has climbed 85% year-to-date (YTD). Just for comparison, the broader S&P 500 Index ($SPX) has increased 26.36% over the past 52 weeks and 7.88% YTD. It reached a 52-week high of $34.82 on April 8, but is now down 45.38% from that level.

On a forward-adjusted basis, Fastly’s price-to-sales ratio of 4.26 times is higher than the industry average of 3.29 times.

Fastly Q1 Results Show Momentum

Fastly’s first-quarter results showed solid momentum, as the company reportedly executed on its roadmap and showcased expansion within its installed base as well as its new business wins. Its revenue increased 20% year-over-year (YOY) to a record $173.02 million, which is higher than the $171.70 million that Wall Street analysts had expected.

This was driven by Network Services, which encompasses solutions to improve websites, apps, and APIs, with revenue of $126.20 million, up 11% YOY, while Security, which includes products to protect digital experience, had revenue of $38.80 million, growing 47%.

Fastly earned a non-GAAP gross margin of 65.1%, compared to 57.3% in the prior-year period. The company also reported non-GAAP EPS of $0.13, surpassing the $0.08 analysts had expected. Moreover, Fastly’s remaining performance obligations (RPOs) climbed to a record $369 million, up 63% YOY.

Additionally, the firm raised its full-year 2026 revenue guidance from $700 million-$720 million to $710 million-$725 million, while non-GAAP operating income guidance was raised from $50 million-$60 million to $58 million-$68 million. However, this was not enough to appease investors who had loftier expectations.

Wall Street analysts are robustly optimistic about Fastly’s ability to reduce its losses. For the current fiscal year, loss per share is projected at 31.3% annually to -$0.46, followed by a 21.7% improvement to -$0.36 in the 2027 fiscal year.

What Do Analysts Think About Fastly’s Stock?

This month, post Fastly’s Q1 results, analyst Rishi Jaluria from RBC Capital maintained a “Sector Perform” rating on the stock, while lowering the price target from $20 to $18. The analyst highlighted the company’s strong results but is also looking for further stabilization in the Network Services before having a more constructive view on the stock.

On the other hand, Fastly’s stock was maintained with an “Overweight” rating, and the price target was raised from $14 to $27 by analyst Jackson Ader at KeyBanc, indicating the firm's bullishness on Fastly’s prospects.

Last month, Evercore ISI maintained Fastly’s stock with an “Outperform” rating and a Street-high price target of $32. According to the analysts, Fastly has hit a turning point, with the narrative evolving from doubts over decelerating delivery-led growth and profitability to confidence in superior growth backed by improved execution and a fundamental platform transformation.

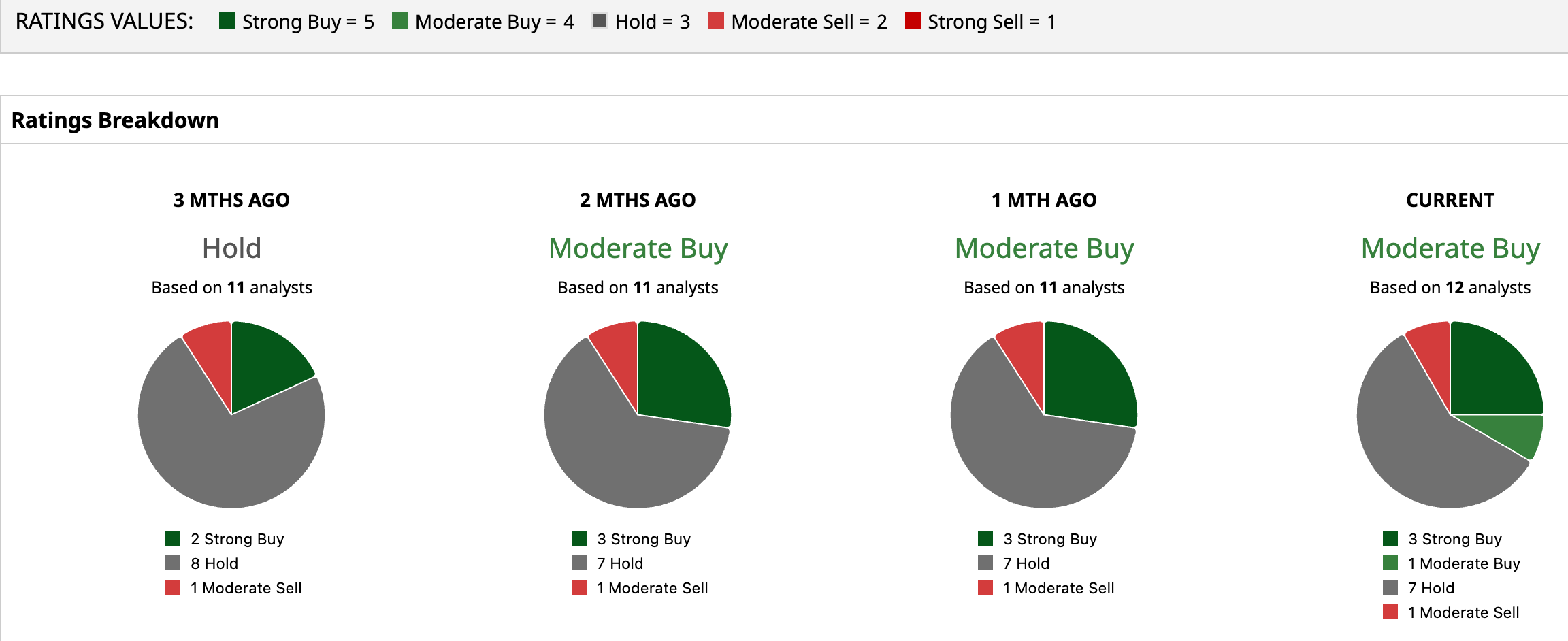

Wall Street analysts have a moderately favorable view of Fastly’s stock, awarding it with a “Moderate Buy” rating overall. Of the 12 analysts rating the stock, three analysts have rated it a “Strong Buy,” one analyst rated it “Moderate Buy,” while seven gave a “Hold” rating, and one analyst suggested “Moderate Sell.” The consensus price target of $24.11 represents a 27.16% upside from current levels, while the Street-high Evercore ISI-given price target of $32 indicates a 68.8% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)