/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)

Apple (AAPL) stock recently hit a record high, thanks to its ability to consistently deliver solid financial results, supported by resilient iPhone demand and accelerating momentum in its high-margin Services segment. This strength remained evident in the second quarter, as Apple posted impressive revenue growth despite a challenging macroeconomic environment.

Given Apple’s strong performance and growth outlook, there are some compelling reasons to consider buying AAPL stock. At the same time, one issue also means that investors should remain cautious. Let's take a closer look.

iPhone Demand Continues to Drive Apple’s Growth Engine

AAPL stock looks compelling, given the company’s solid growth driven by resilient iPhone demand and the rapid expansion of its high-margin Services business. Notably, Apple delivered an impressive performance in the first half of the year, with revenue growing at a double-digit rate and margins improving despite rising memory costs.

In Q2, Apple reported revenue of $111.2 billion, up 17% from the same period last year. A major driver behind this growth was the strong performance of the iPhone, which generated $57 billion in revenue — up 22% year-over-year (YOY) — despite ongoing supply constraints.

Demand for the iPhone 17 lineup remained robust across key global markets, including the U.S. and Greater China. Apple also reported that its active installed base for iPhone reached an all-time high, while the number of customers upgrading to newer devices set a new March-quarter record. These trends indicate that Apple’s core hardware business momentum is likely to continue in the coming quarters.

Apple's Services Business Is Becoming a Profitability Powerhouse

Beyond hardware sales, Apple’s Services segment remains an increasingly important growth engine for the company. Apple has built a vast ecosystem of over 2.5 billion active devices worldwide that supports recurring revenue streams across subscriptions, payments, and digital content. Services revenue climbed to $31 billion during the quarter, up 16% YOY, with double-digit growth recorded across most markets and categories.

The Services business also continues to strengthen Apple’s profitability profile. Overall gross margin improved sequentially to 49.3%. While product gross margin declined to 38.7%, Apple's Services gross margin expanded further to 76.7%.

The sustained iPhone demand and accelerating Services revenue position Apple well to maintain healthy top-line growth. Management expects total revenue for the June quarter to increase between 14% and 17% YOY. Although the iPad segment may face tougher comparisons due to the previous year’s launch cycle, Apple expects Services growth to remain broadly in line with the March quarter.

Overall, Apple’s expanding installed base, loyal customer ecosystem, and growing contribution from high-margin Services continue to strengthen the company’s long-term investment case.

Rising Costs and Valuation Risks Could Limit Upside

Despite Apple’s strong financial performance, there are reasons for investors to remain cautious. The company has continued to deliver healthy revenue growth while steadily expanding its margins, supported by strong iPhone demand and accelerating momentum in its high-margin Services business. However, rising component costs, driven by higher memory prices, are likely to emerge as a significant headwind.

Apple indicated that the impact of higher memory costs on gross margins was relatively limited during the March quarter, largely because the company benefited from previously accumulated inventory. However, management has warned that memory costs are expected to rise significantly in the second half of fiscal 2026, which could put pressure on profitability in the coming quarters.

Apple’s valuation also remains a concern. Much of the optimism surrounding Apple’s record iPhone sales and expanding services ecosystem appears to already be reflected in the stock price. AAPL stock currently trades at 33.5 times forward earnings, which is high considering its earnings growth trajectory.

According to Wall Street estimates, EPS is projected to increase 17.% in fiscal 2026, followed by more moderate 9% growth in fiscal 2027.

Should You Buy Apple Stock?

Apple will continue to benefit from unmatched brand loyalty, an expanding ecosystem, recurring Services revenue, and its enormous installed base. However, rising memory costs are expected to put pressure on profit margins, which could weigh on earnings growth and limit near-term upside potential.

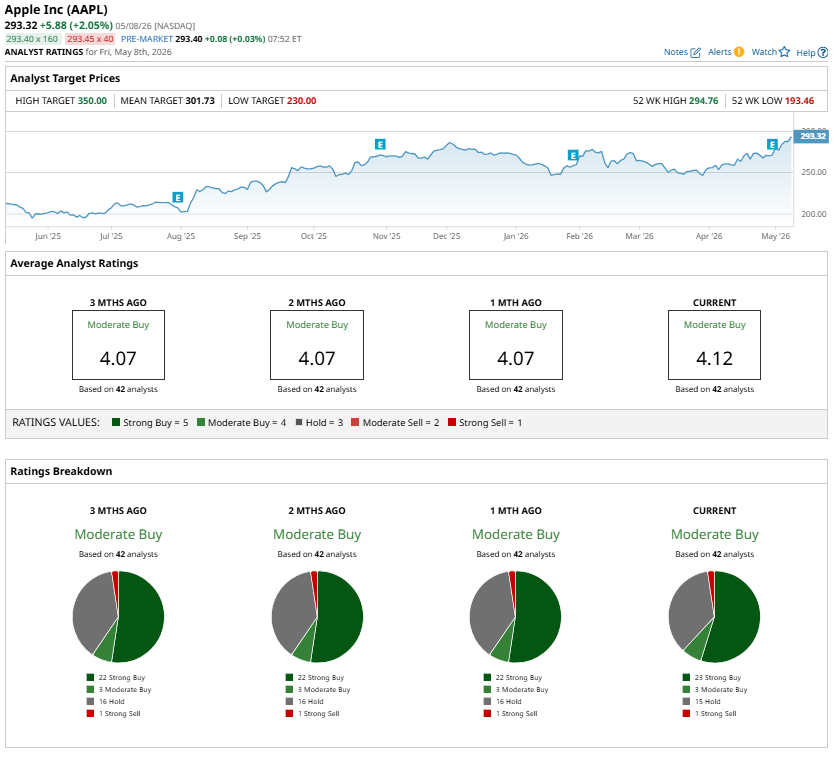

Overall, Apple remains a strong long-term investment. However, its valuation warrants caution. Meanwhile, analysts maintain a “Moderate Buy” consensus rating on AAPL stock.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Accenture%20plc%20buiding%20with%20logo-by%20JHVEPhoto%20via%20iStock.jpg)