AI spending is no longer just lifting microchip stocks. It is now showing up across the cloud and software side, too. Alphabet (GOOG) (GOOGL) Cloud posted a 63% revenue increase in its latest quarter, while Amazon's (AMZN) AWS grew 28%. Hence, companies are spending real money on the infrastructure needed to run AI at scale. As a result, money is flowing back into cloud infrastructure and networking stocks that had long been treated like slow yet steady names.

That shift is a big reason Akamai Technologies (AKAM) is getting fresh attention. On May 7, with its first-quarter results, the company said a major U.S.-based AI customer had agreed to spend $1.8 billion over seven years on its Cloud Infrastructure Services.

The deal with Anthropic is now the biggest customer deal in AKAM's history. The timing mattered because the rest of the quarter was solid as well. Cloud Infrastructure Services revenue jumped 40% to $95 million, and management raised full-year non-GAAP EPS guidance to $6.78 at the midpoint. Investors reacted fast, sending the stock up 26.58% the following day.

With a seven-year, $1.8 billion AI infrastructure deal in hand and its fastest-growing business still gaining speed, has Akamai Technologies stock already had its big move, or is there still more room to run?

The Numbers Behind the Momentum

Akamai helps companies move data around the internet quickly and safely, using its global edge network to speed up and protect websites, apps, and online services.

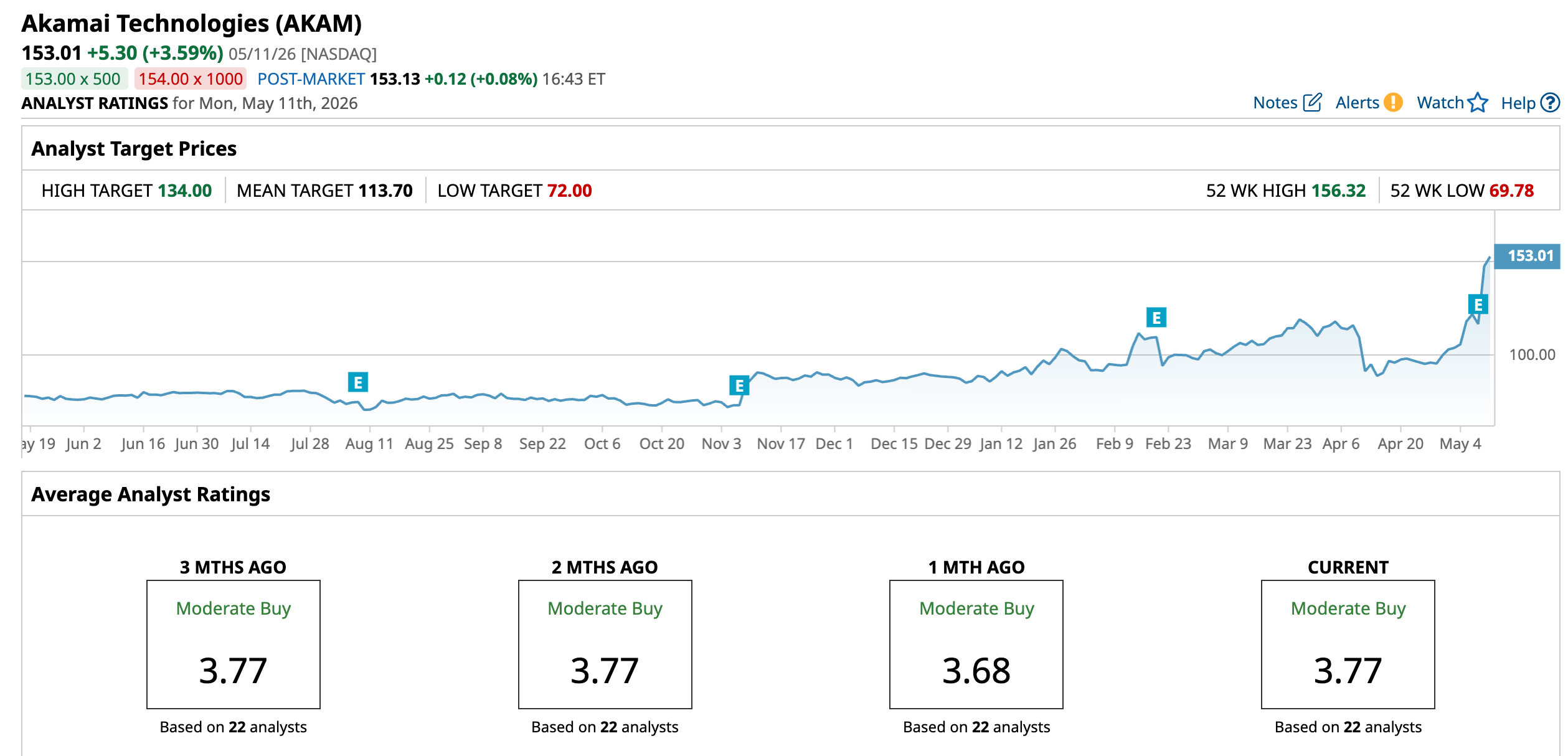

The stock has had a big run, climbing 100.67% over the past 12 months and 75.37% year-to-date (YTD).

It now trades at a forward price-to-earnings of 27.96 times versus about 24.97 times for its sector, which shows the market is giving it a premium for its growth push.

Results last quarter were solid, but not perfect. In Q1 FY2026, revenue was $1.07 billion, up 5.8% from a year earlier and right in line with forecasts, while adjusted EPS of $1.61 was just above expectations. Adjusted operating income was $282.8 million, for a 26.3% margin, but operating margin on a reported basis slipped to 10.7% from 15.2% a year ago, and free cash flow margin dropped to 3.1% from 14.8% in the prior quarter, showing some pressure from higher spending.

The good news is that billings grew 9.7% to $1.13 billion, which points to healthy demand, and management nudged full-year guidance higher, now looking for $4.50 billion in revenue and $6.78 in adjusted EPS at the midpoint.

Growth Levers Powering Akamai’s Edge

Akamai Technologies is widening its reach through Arrow Electronics, which gives the company a broader path into enterprise customers buying cloud, security, and app delivery tools. Through Arrow’s enterprise computing solutions business, Akamai is getting its products in front of more companies looking for full IT setups across cloud, data centers, networking, and software. This helps the company sell deeper into large customers that want both speed and security in the ways in which they run digital services.

At the same time, Akamai is making a bigger push into AI infrastructure. Its new AI Grid, built on NVIDIA’s (NVDA) design, stretches across 4,400 edge locations and is meant to move AI workloads closer to the locations they are actually used, instead of sending everything back to a central data center. With thousands of RTX PRO 6000 Blackwell GPUs across its network, the company is building out the kind of low-latency setup needed for real-time AI tasks.

That push goes further with its plan to add even more NVIDIA Blackwell GPUs across its distributed cloud platform. The goal is simple: cut delays, reduce data transfer bottlenecks, and make it easier for customers to run AI inference at scale across many locations. As more AI use cases depend on fast response times, this gives Akamai Technologies a clearer role in the infrastructure layer behind them.

Analysts Reassess the Upside

For the June quarter, earnings are forecast at $1.00 per share, down 9.09% from $1.10 a year ago. By the September quarter, that is expected to improve slightly to $1.07, up 0.94%. For all of 2026, earnings are projected to come in at $4.15 per share, down 5.90% from $4.41 last year.

KeyBanc Capital Markets kept its “Overweight” rating and raised its price target to $195, saying Akamai Technologies’ GPU and colocation buildout could support strong, high-margin cloud revenue over the life of its seven-year contract base.

Scotiabank analyst Patrick Colville also turned more upbeat, lifting his target from $120 to $180 and keeping a “Sector Outperform” rating. That target suggested about 22% upside from where the stock was trading after the earnings jump.

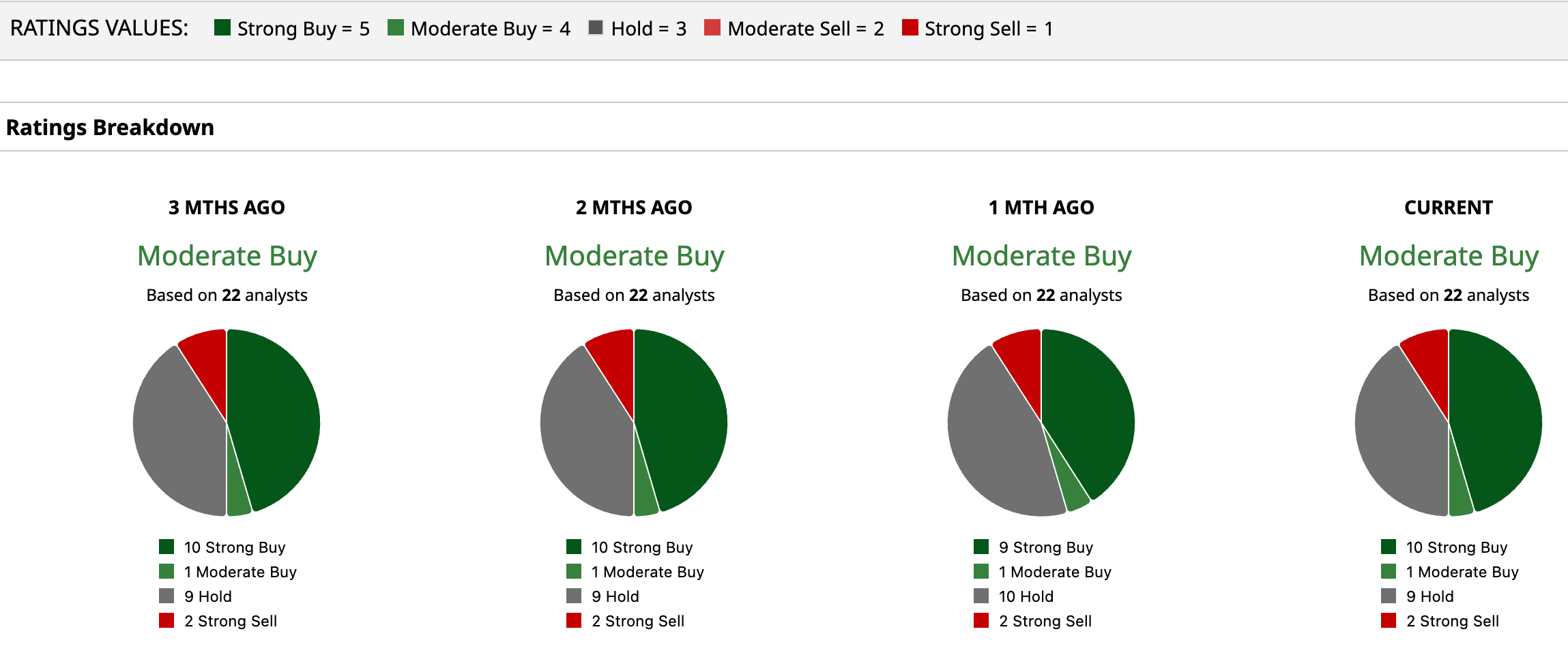

All 22 analysts covering Akamai Technologies rate it a consensus “Moderate Buy,” but AKAM has already surpassed the average price target is $113.70 and the Street-high target of $134.

Conclusion

Akamai still looks buyable here, not because the stock is cheap in a traditional sense, but because the $1.8 billion, seven-year AI infrastructure Anthropic deal materially changes the company’s growth profile and gives investors a clearer line of sight into its cloud expansion. The shares have already moved sharply, so near-term volatility would not be surprising, but the direction still looks biased higher if Akamai keeps converting AI demand into real cloud revenue and follows through on the stronger outlook management just laid out.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Microsoft%20France%20headquarters%20by%20JeanLuclchard%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)