There's a seasonal window opening up between now and August that looks favorable for lower rates, particularly at the long end of the curve. Bond traders have seen this pattern play out enough times to pay attention:

Key Reasons for Summer Yield Declines:

- "Summer Slowdown" & Lower Liquidity: Trading volumes typically decrease as institutional investors go on vacation, which can reduce liquidity and, paradoxically, prompt more aggressive "search for yield" behavior among remaining managers.

- Reinvestment Flows: Large coupon payments from investment-grade bonds often mature or are paid out in June and July, prompting portfolio managers to reinvest this cash into new, long-term bonds.

- "Sell in May" Effect: As some investors rotate out of equities and into lower-risk assets, such as long-duration Treasury bonds, demand increases, pushing bond prices up and yields down.

- Softening Economic Data: Markets often experience a lull in data releases, and summer employment reports often signal weakening, fueling market expectations of a more dovish Federal Reserve.

- Positive Seasonals for Duration: Historically, April through August is the strongest period for bonds (a "bullish" pattern), compared with the bearish, high-yield-issuance period in early autumn.

It's not a guaranteed move, but the setup is there again this year, and positioning has started to reflect it.

Two things are helping the case right now. First, we're heading into the U.S. government's fiscal year close in September, and history shows rates often ease ahead of that period as Treasury issuance patterns and budget flows create some natural demand for longer paper. Second, tensions between the U.S. and Iran appear to be easing, which should ease pressure on oil prices in the coming months. Lower energy costs would ease inflation concerns and give the long end more room to rally as the market prices in less persistent price pressure.

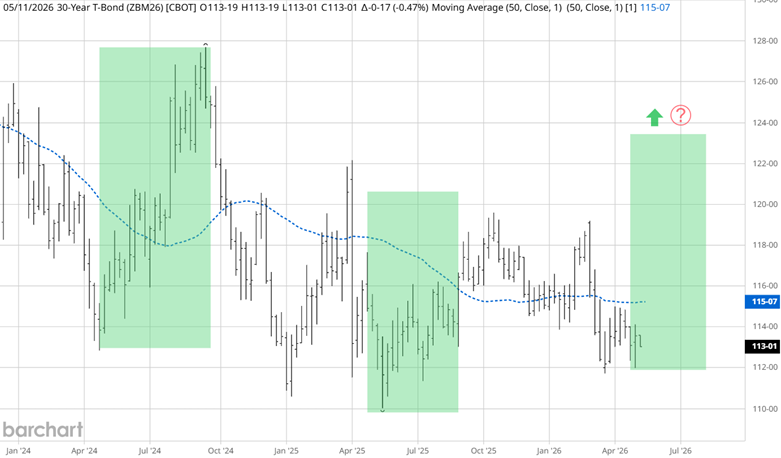

Technical Picture

Source: Barchart

Technically, the weekly nearby chart of the 30-year bond futures looks lethargic. The 50-week simple moving average is moving sideways. While the Federal Reserve might be looking for inflation to return to its 2% target, the long end of the yield curve appears to be finding its happy spot. We will discuss the upcoming seasonal pattern soon, but for reference, I have highlighted (in green boxes) the last two years' seasonal patterns of higher prices and lower yields. The last green box is the big question: Will we see the traditional 30-year bond price rally this year?

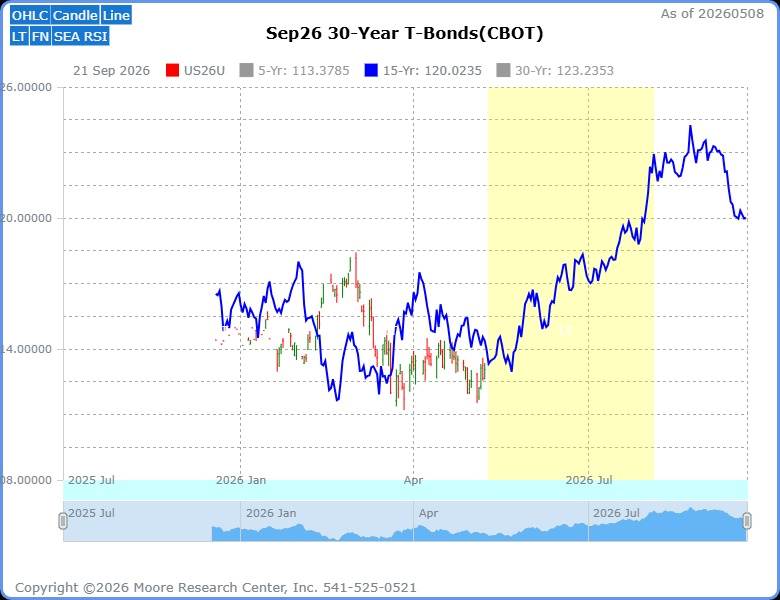

Seasonal Pattern

Source: Moore Research Center, Inc. (MRCI)

MRCI research over the past 15 years on the 30-year bond September futures contract (blue line) reveals that its seasonal low typically occurs in late February. This year, the low came a month later at the end of March. The bond market then rallied briefly before retesting the seasonal low in May. In early May, the restest occurred, and as long as the February low holds, we have a good chance of the seasonal low being in place. The yellow box represents MRCI's optimal buying window. The duration is 87 calendar days, allowing short-term traders to trade in and out of the market with a bullish bias, or longer-term traders to build and manage a bullish core position.

The results of MRCI's extensive research have revealed that the September bond futures have closed higher on about August 04 than on May 10 in 13 of the past 15 years, an 87% occurrence. During the hypothetical testing period, 4 of the years had no daily closing drawdown. The average net profit per contract was a whopping $4,343.75.

As a crucial reminder, while seasonal patterns can provide valuable insights, they should not be the basis for trading decisions. Traders must consider technical and fundamental indicators, risk management strategies, and market conditions to make informed, balanced trading decisions.

Assets to Participate in the Bullish Interest Rate Market

Treasury bond futures (expecting bond prices higher / yields lower):

- 30-Year U.S. Treasury Bond Futures (ZB): The direct instrument. Traded on CME, highly liquid, with each point worth $1,000. This is the core contract for playing the long end.

- 10-Year Treasury Note Futures (ZN): Very highly correlated to the 30-year, though with shorter duration. Many traders use it as a liquid proxy or pair it with the 30-year for curve trades.

- iShares 20+ Year Treasury Bond ETF (TLT): The most popular ETF for long-duration Treasuries. Moves closely with 30-year futures but trades like a stock with easier access for smaller accounts.

- Vanguard Long-Term Treasury ETF (VGLT): Tracks longer Treasuries (average maturity in the 10-25 year range) with low costs and solid liquidity.

- Other long government bond ETFs include SPDR Portfolio Long Term Treasury ETF (SPTL), Schwab Long-Term U.S. Treasury ETF (SCHQ), or iShares 25+ Year Treasury STRIPS ETF (GOVZ) for more targeted exposure.

- Options on 30-year or 10-year futures: Calls or call spreads for leveraged directional bets with defined risk.

In Closing…

In the end, this seasonal window from now through early August offers one of the more consistent setups in the Treasury market, showing up in 13 of the last 15 years where the September 30-year bond futures closed higher on or around August 4 than on May 10—an 87% hit rate according to MRCI data. That's not random; it aligns closely with the U.S. government's fiscal year, which ends in September, when issuance patterns, budget flows, and reinvestment activity tend to create natural support for longer-dated paper. Whether you trade the ZB futures directly, use the highly correlated ZN 10-year contract, or prefer TLT and other ETFs, the setup is worth watching. Just remember, seasonals are a bias, not a crystal ball—pair them with solid risk management and stay flexible if the fundamentals shift.

On the date of publication, Don Dawson did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)