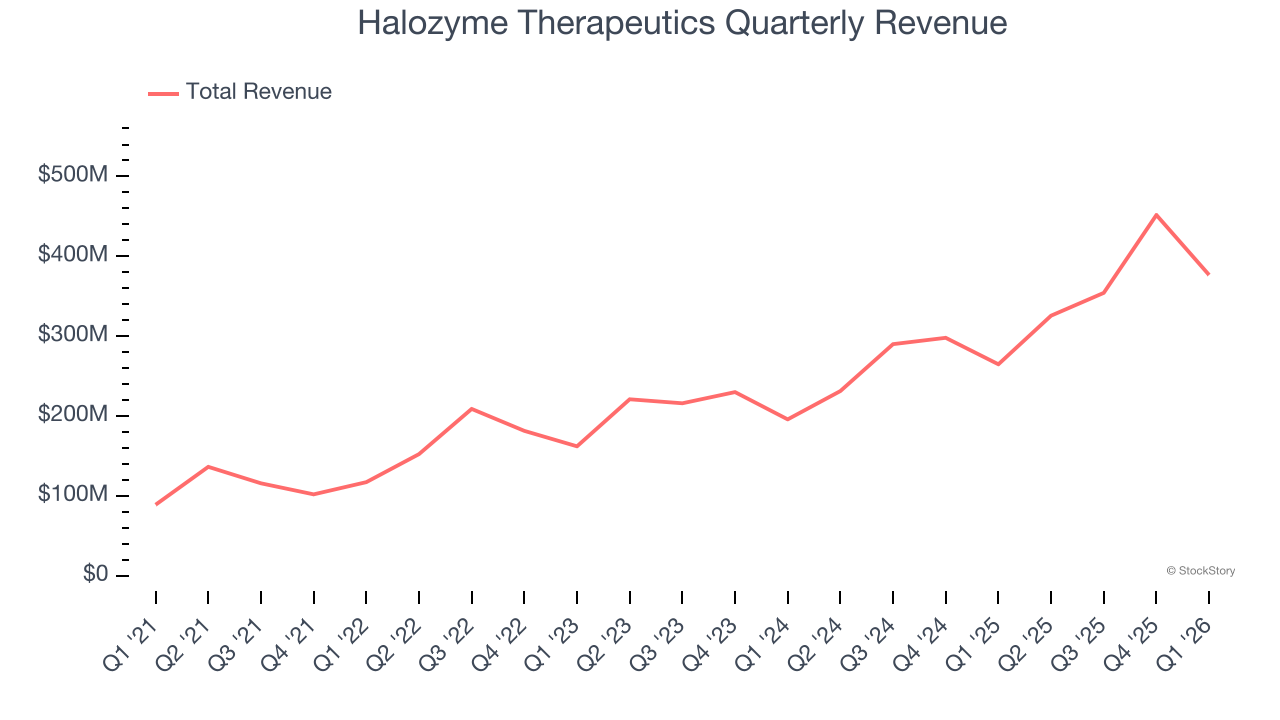

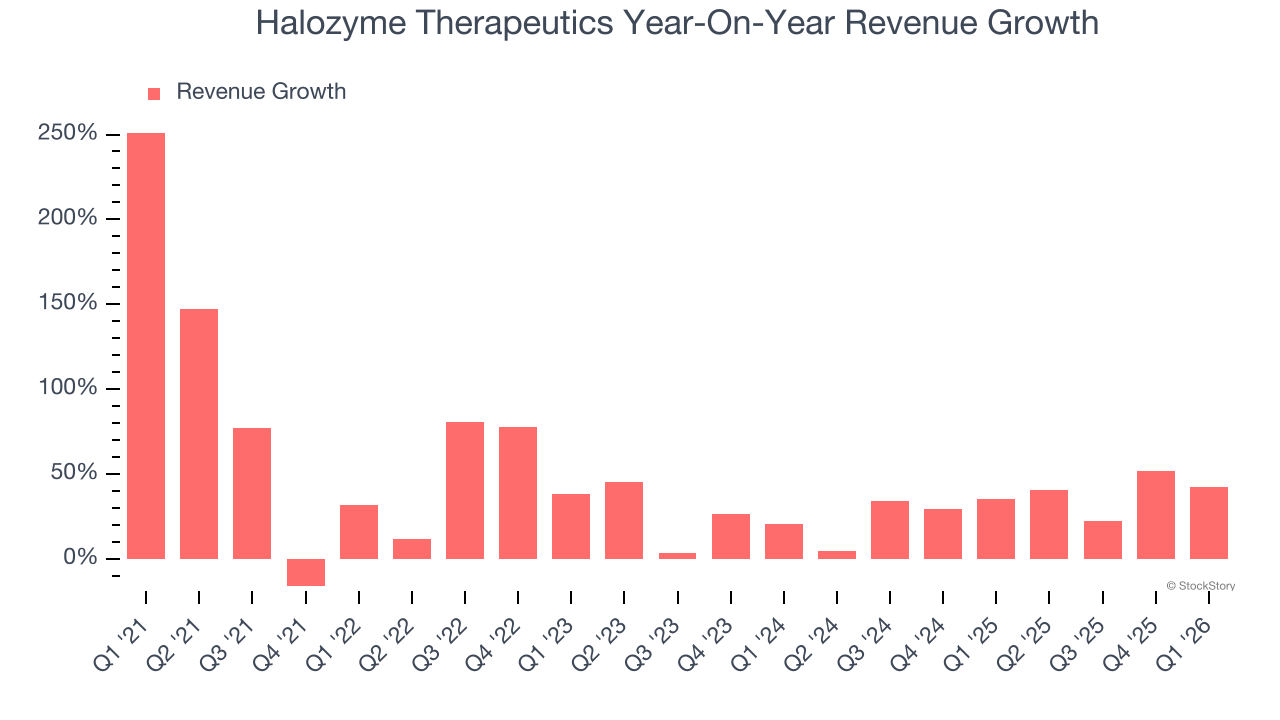

Biopharmaceutical drug delivery company Halozyme Therapeutics (NASDAQ:HALO) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 42.2% year on year to $376.7 million. The company expects the full year’s revenue to be around $1.76 billion, close to analysts’ estimates. Its non-GAAP profit of $1.60 per share was 5.3% above analysts’ consensus estimates.

Is now the time to buy Halozyme Therapeutics? Find out by accessing our full research report, it’s free.

Halozyme Therapeutics (HALO) Q1 CY2026 Highlights:

- Revenue: $376.7 million vs analyst estimates of $355.1 million (42.2% year-on-year growth, 6.1% beat)

- Adjusted EPS: $1.60 vs analyst estimates of $1.52 (5.3% beat)

- Adjusted EBITDA: $229.5 million vs analyst estimates of $214 million (60.9% margin, 7.2% beat)

- The company reconfirmed its revenue guidance for the full year of $1.76 billion at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $8 at the midpoint

- EBITDA guidance for the full year is $1.17 billion at the midpoint, above analyst estimates of $1.15 billion

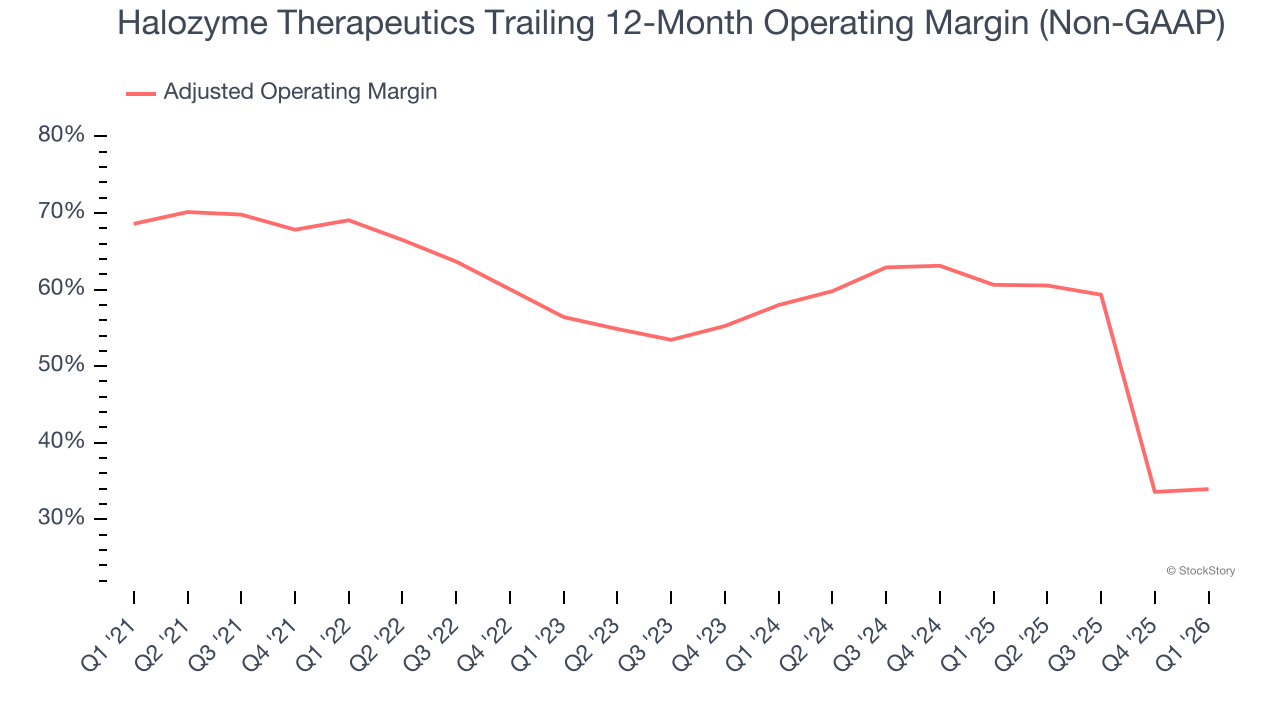

- Operating Margin: 49%, down from 53.4% in the same quarter last year

- Market Capitalization: $7.60 billion

"I am pleased to announce our new $1 billion share repurchase program and that we project to repurchase at least $400 million in 2026, which is a reflection of our strong cash generation and confidence in the long-term value and durability of our business. We started 2026 with exceptional momentum, highlighted by three new recent collaboration and licensing agreements with Vertex, Oruka and GSK, demonstrating the strong interest in Hypercon and ENHANZE and showcasing the real potential to exceed our goal of three new SC delivery platform deals this year. The two Hypercon multi-target agreements confirm the strong interest of biopharma companies to reduce injection volume through hyperconcentration and allow more flexible administration in the home. Our new multi-target agreement with GSK represents a significant opportunity for ENHANZE with multiple promising oncology targets, including its first potential application with antibody drug conjugates. This momentum creates durable new royalty opportunity beginning in the 2030s and extending to at least the mid-2040s," said Dr. Helen Torley, President and Chief Executive Officer of Halozyme.

Company Overview

Known for transforming hours-long intravenous infusions into minutes-long subcutaneous injections, Halozyme Therapeutics (NASDAQ:HALO) develops and licenses its proprietary ENHANZE technology that enables subcutaneous delivery of injectable drugs that would otherwise require intravenous administration.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Halozyme Therapeutics grew its sales at an incredible 35.4% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Halozyme Therapeutics’s annualized revenue growth of 32.2% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Halozyme Therapeutics reported magnificent year-on-year revenue growth of 42.2%, and its $376.7 million of revenue beat Wall Street’s estimates by 6.1%.

Looking ahead, sell-side analysts expect revenue to grow 21.6% over the next 12 months, a deceleration versus the last two years. Still, this projection is admirable and suggests the market is baking in success for its products and services.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

Halozyme Therapeutics has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average adjusted operating margin of 51.7%.

Looking at the trend in its profitability, Halozyme Therapeutics’s adjusted operating margin decreased by 35.1 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 24 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Halozyme Therapeutics generated an adjusted operating margin profit margin of 49%, down 4.5 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

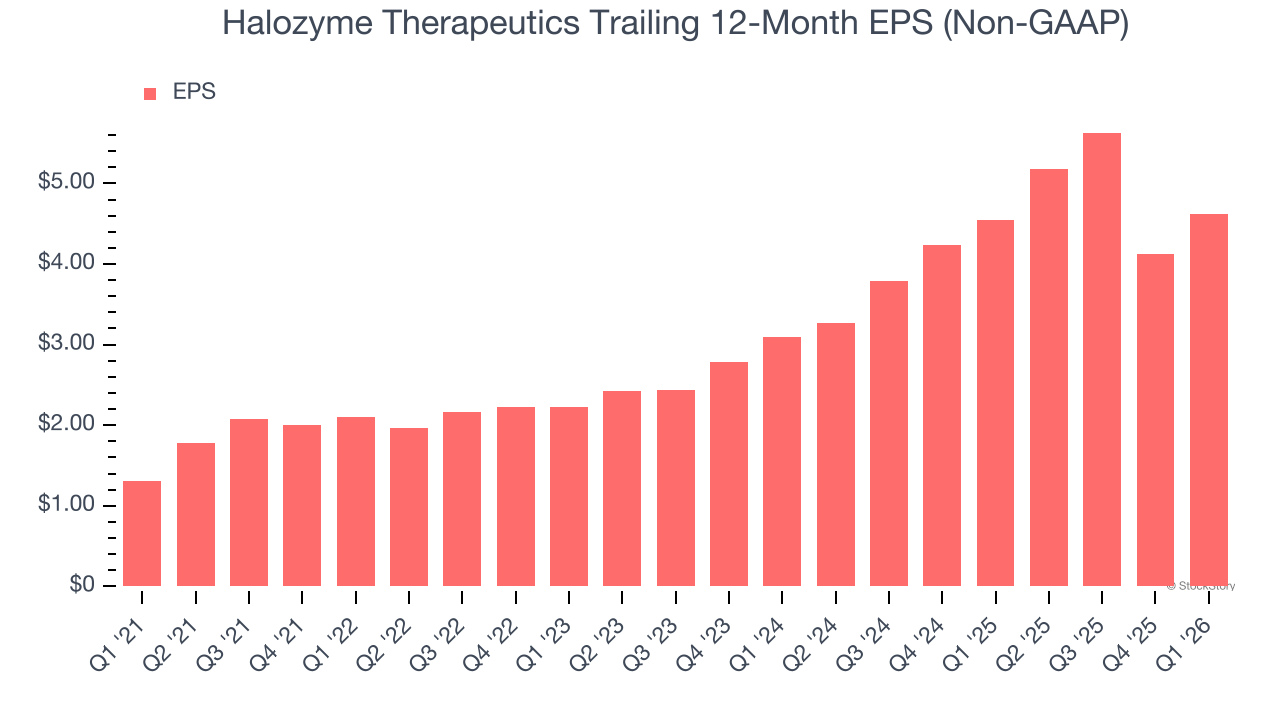

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Halozyme Therapeutics’s EPS grew at an astounding 28.7% compounded annual growth rate over the last five years. However, this performance was lower than its 35.4% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Diving into the nuances of Halozyme Therapeutics’s earnings can give us a better understanding of its performance. As we mentioned earlier, Halozyme Therapeutics’s adjusted operating margin declined by 35.1 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Halozyme Therapeutics reported adjusted EPS of $1.60, up from $1.11 in the same quarter last year. This print beat analysts’ estimates by 5.3%. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Halozyme Therapeutics’s Q1 Results

We were impressed by how significantly Halozyme Therapeutics blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance slightly missed. Overall, this print had some key positives. The stock remained flat at $67.08 immediately following the results.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).

/Amazon_com%20Inc_%20%20package%20by%20-%20AdrianHancu%20via%20iStock.jpg)

/Salesforce%20Inc%20HQ%20building-by%20JHVEPhoto%20via%20Shutterstock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Intel%20Corp_%20Santa%20Clara%20campus-by%20jejim%20via%20Shutterstock.jpg)