/Advanced%20Micro%20Devices%20Inc_%20logo%20on%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

Shares of Advanced Micro Devices (AMD) have rallied more than 303% over the past year, climbing to record highs. The surge reflects rising demand for high-performance instinct GPUs as businesses and cloud providers accelerate investments in AI infrastructure.

While much of the spotlight has been on AI accelerators, high-performance CPUs are also witnessing strong adoption. As AI workloads evolve beyond training models toward inferencing and Agentic AI applications, computing requirements are expanding significantly. This shift is creating demand for more accelerators and CPUs.

AMD appears well-positioned to benefit from strong AI demand. The company offers a broad portfolio spanning both data center CPUs and AI accelerators, allowing it to deliver integrated, rack-scale AI solutions. Its strong supply chain capabilities and ongoing investments in manufacturing capacity further strengthen its ability to scale alongside growing industry demand.

Beyond revenue growth, AMD has been improving profitability at a solid pace, signaling stronger operational efficiency. Its significant earnings growth indicates that AMD stock still has room to run.

AMD’s EPYC and Instinct Momentum Signals Strong Growth Ahead

AMD appears well-positioned to sustain its strong business momentum as demand for high-performance computing and AI infrastructure continues to accelerate. The company delivered an impressive first-quarter performance, supported by robust adoption of its EPYC server processors, Instinct AI accelerators, and Ryzen CPUs.

Revenue for the quarter rose 38% year-over-year (YOY) to $10.3 billion, while earnings climbed more than 40%. Its free cash flow more than tripled to $2.6 billion. Further, growth was broad based across the company, with every business segment posting YOY gains.

The data center division has become AMD’s core growth engine. Segment revenue surged 57% from a year earlier to a record $5.8 billion, driven primarily by strong demand for EPYC server CPUs and Instinct GPUs. The company continues to benefit from rising enterprise and cloud spending on AI infrastructure as businesses expand computing capacity to support increasingly complex workloads.

AMD’s server business maintained strong momentum, with sales increasing more than 50% YOY. Demand from both cloud providers and enterprise customers remained robust. Market share gains accelerated as AMD ramped production of its fifth-generation EPYC Turin processors while continuing to see healthy adoption of its fourth-generation EPYC chips across diverse workloads.

The long-term outlook for server processors remains highly attractive as Agentic AI applications drive a structural increase in computing requirements. AMD now expects the total addressable market for server CPUs to grow significantly. That expanding market opportunity could provide a significant runway for future growth.

The company’s near-term outlook also remains strong. AMD expects server CPU revenue to increase more than 70% YOY in the second quarter, with robust growth likely to continue through the second half of 2026 and into 2027 as next-generation EPYC processors ramp further.

AMD’s AI accelerator business is also gaining traction at a rapid pace. Revenue from its data center AI operations grew by a strong double-digit percentage YOY as adoption of Instinct accelerators expanded across cloud providers, enterprises, sovereign AI projects, and supercomputing customers.

AMD’s existing partners are expanding the use of Instinct accelerators across a broader range of AI workloads, while new customers continue to adopt the platform for both AI training and inference applications.

With AI infrastructure spending continuing to increase, AMD will witness strong demand across its data center and AI product portfolio. Moreover, its solid revenue will translate into stellar earnings, which strengthens its bullish investment thesis.

AMD Stock Is a Buy

AMD remains strongly positioned to capitalize on the accelerating demand for AI infrastructure and high-performance computing. With record data center growth, expanding adoption of CPUs and Instinct accelerators, and continued market share gains, the company is likely to deliver strong growth.

Despite the strong rally, AMD’s valuation still appears attractive relative to its growth outlook. AMD trades at a price-to-earnings (P/E) multiple of 60.12, which is reasonable given analysts' expectations of earnings growth of 82.57% in 2026 and 60.64% in 2027. Such growth projections suggest the stock could still have meaningful upside potential.

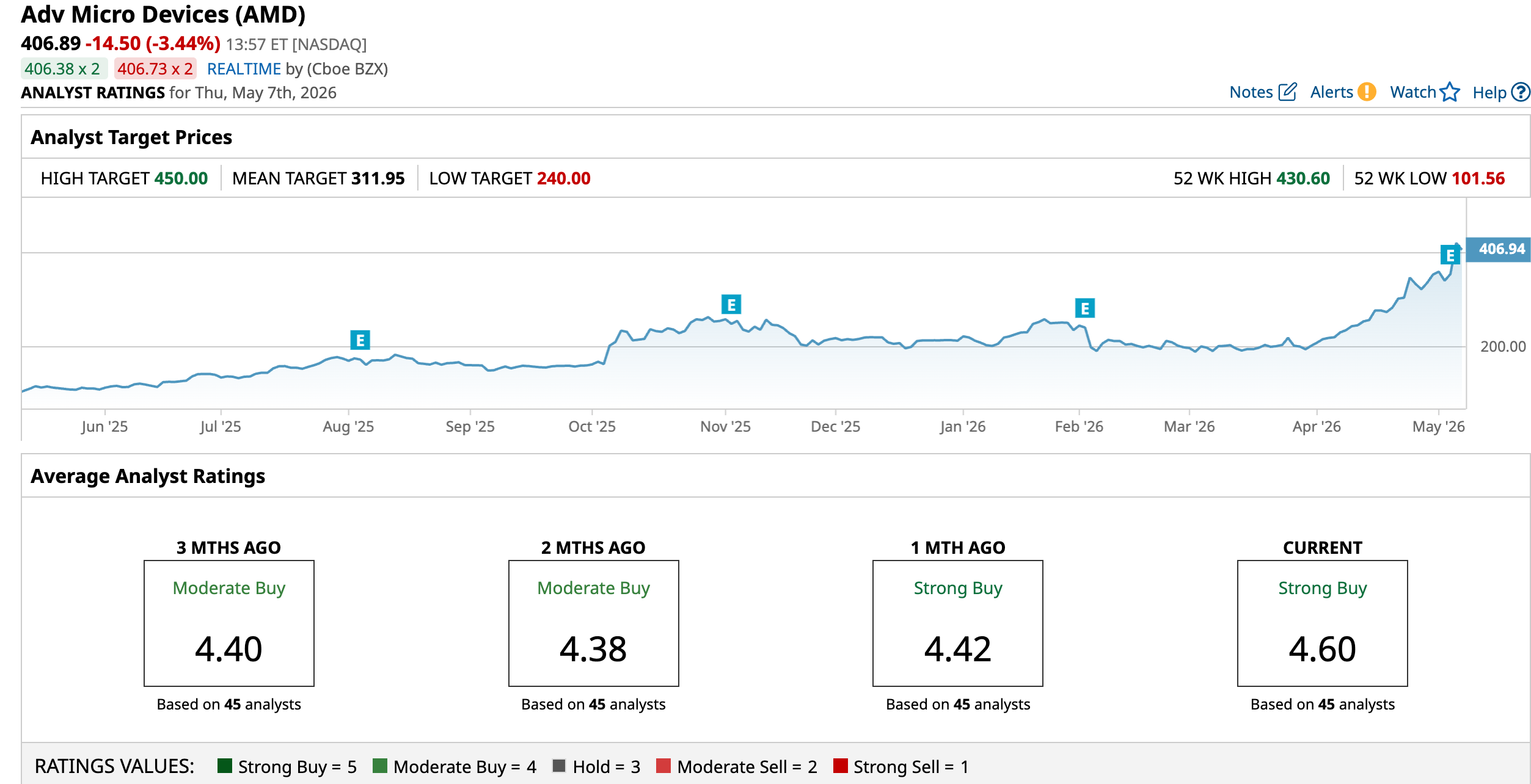

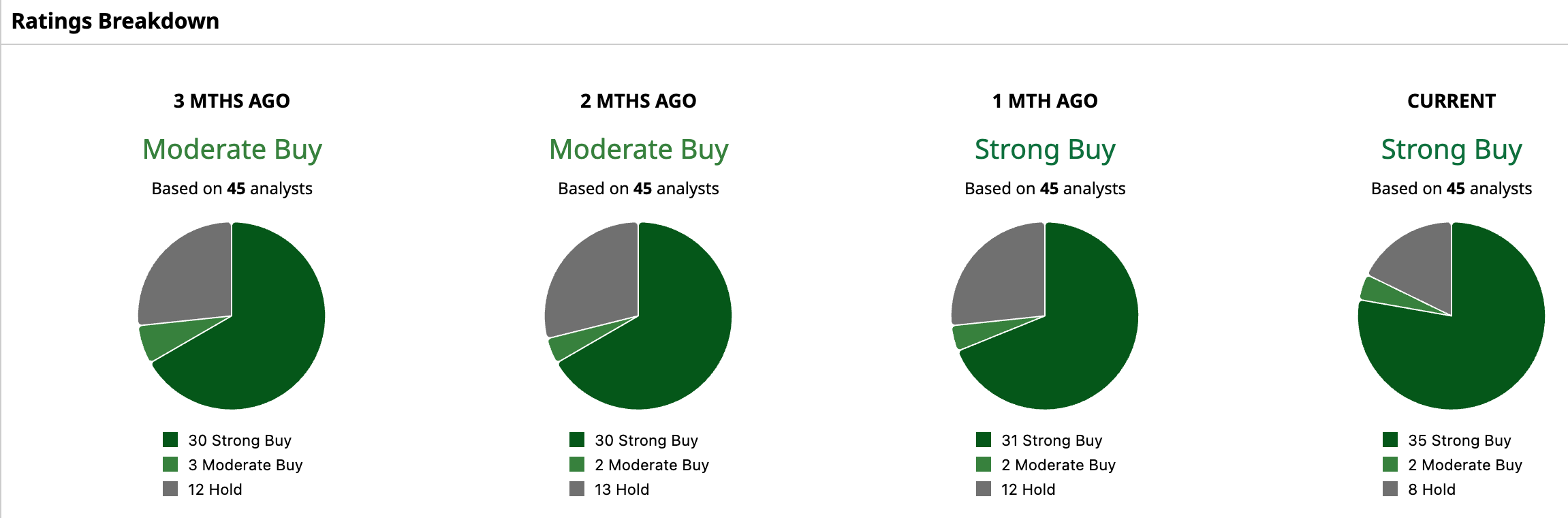

Wall Street sentiment also remains positive, with analysts maintaining a “Strong Buy” rating on AMD.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)