Strategy (MSTR) reported its first-quarter 2026 earnings on May 5, and as of May 3, it held 818,334 Bitcoin, up 22% so far this year. The company said that stash had a cost basis of $61.81 billion and a market value of $64.14 billion, with an average purchase price of about $75,537 per coin. That massive Bitcoin position led to a $14.46 billion unrealized loss in the first quarter and pushed net loss to $12.54 billion, or $38.25 per diluted share, much worse than the $4.22 billion loss it posted a year earlier.

Still, Strategy preferred stock is becoming a bigger part of the story. The company has now made 23 straight preferred payouts on time and in full, for a total of more than $693 million since it launched those products in early 2025.

Its STRC preferred stock, the Variable Rate Series A Perpetual Stretch Preferred Stock, has grown to $8.5 billion in just nine months, making it the largest preferred stock by market value in the world, with an annualized dividend rate currently fixed at 11.50% and monthly payments of $0.96 per share. In the Q1 earnings release, Executive Chairman Michael Saylor also said the company plans to ask shareholders to approve a shift to semi-monthly STRC dividend payments to help improve liquidity and price stability.

With more than $13.5 billion in preferred equity outstanding, Bitcoin is still driving the numbers, and a possible change in dividend payments is on the table. What does Strategy's Q1 story actually mean for the investors holding it?

Inside the Numbers

Strategy, formerly MicroStrategy, now runs two businesses at once: its initial enterprise software business and its much bigger Bitcoin holding strategy, which now shapes how most investors see the company.

The stock shows that clearly. Shares are down 55.95% over the past 52 weeks, but still up 20.14% so far this year as Bitcoin sentiment has improved.

Even on valuation, Strategy looks unusual, trading at a forward price-to-earnings of 1.37 times compared with the sector average of 24.61 times.

Its STRC preferred stock currently offers an annualized dividend rate of 11.50% and pays $0.96 per share each month, and Strategy has continued to declare and pay, or is set to pay, those dividends since the start of fiscal 2026.

The first-quarter numbers show where the real pressure came from. Revenue rose 11.9% from a year ago to $124.3 million, while gross profit came in at $83.4 million with a 67.1% margin, which suggests the software side is still holding up. But that was drowned out by a $14.47 billion operating loss, almost all of it tied to a $14.46 billion unrealized Bitcoin loss. Net loss reached $12.54 billion, or $38.25 per share, while cash slipped slightly to $2.21 billion, showing again that Bitcoin, more than the core business, is driving the reported results.

What Is Powering the Story

On the software side, Strategy used Strategy World 2026 to show where it wants to grow outside Bitcoin. Chief Product Officer Saurabh Abhyankar talked about new features for Strategy Mosaic, the company’s semantic layer for business data. The updates included Model Linking, which helps teams connect data from areas like sales, finance, and marketing, plus Mosaic Sentinel, a toolset for risk checks, anomaly detection, and cost tracking for AI agents. Strategy also added wider support for open standards like the Model Context Protocol and Open Semantic Interchange, with Git-based version control.

At the same time, Strategy’s preferred stock story is starting to reach beyond its own balance sheet. In February at Strategy World 2026, Prevalon Energy and Anchorage Digital said they had each put part of their corporate treasury into STRC. That matters because it suggests other institutions may be willing to use Strategy's preferred stock products, not just watch the company use them for itself.

Still, Bitcoin is the main driver. In January, Strategy bought 13,627 BTC for $1.25 billion in its biggest purchase since last summer, using money raised through common-stock sales. By May 3, Strategy held 818,334 BTC and had posted a 9.4% BTC Yield and about $4.97 billion in BTC $ Gain so far this year.

Wall Street’s Read

For the June 2026 quarter, the average estimate is $65.09, up from $32.60 a year earlier, which points to 99.66% year-over-year (YOY) growth. For the September 2026 quarter, analysts expect $41.08 versus $8.42 last year, or 387.89% growth. For full-year 2026, the estimate jumps to $136.35 from a loss of $15.23 a year earlier, which comes out to projected growth of 995.27%.

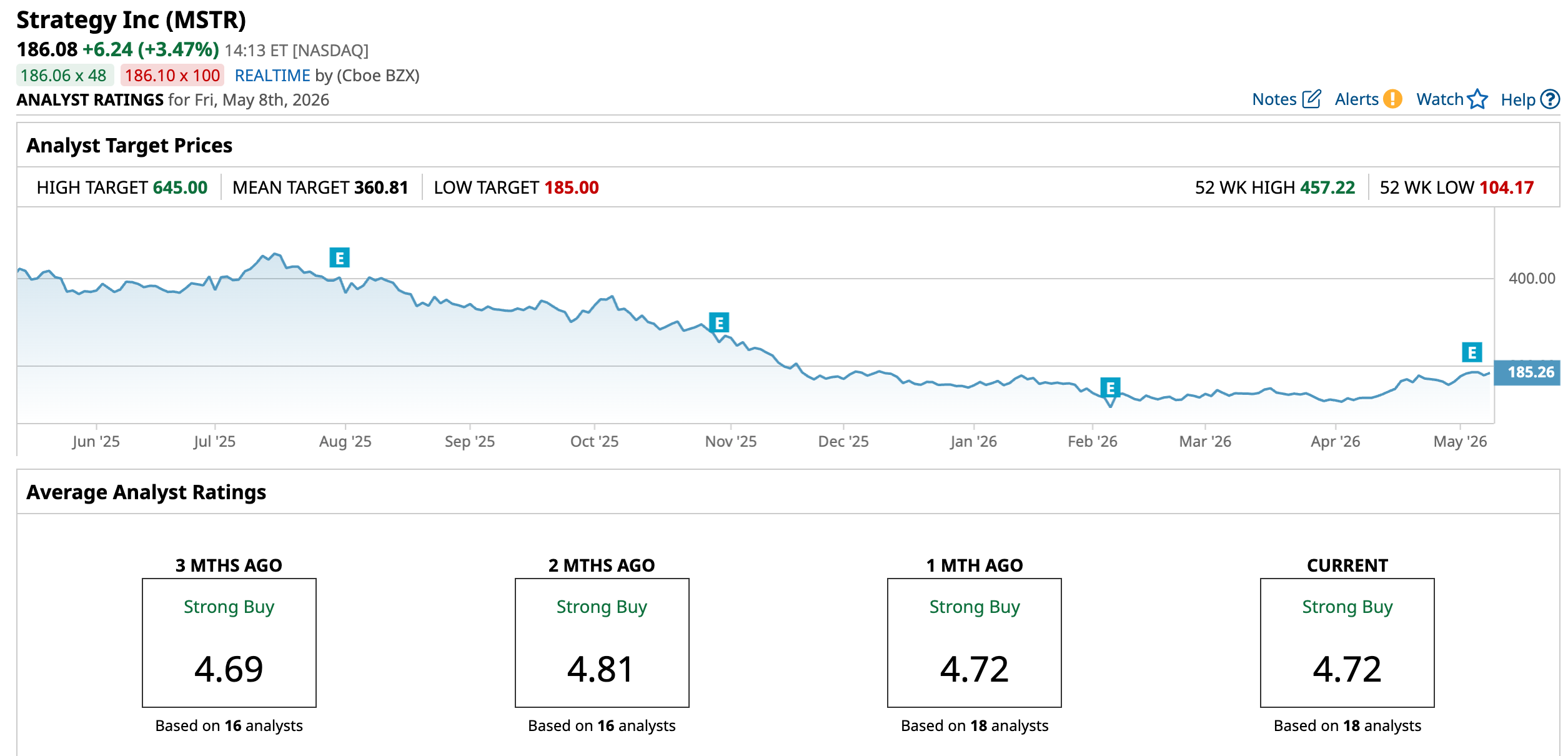

Not every analyst is reading the stock the same way, though. Cantor Fitzgerald raised its price target on Strategy to $212 from $192 and kept an “Overweight” rating, helped by stronger Bitcoin prices and better sentiment around the shares.

Canaccord Genuity took the other side, with analyst Joseph Vafi cutting his target by more than 60% after Bitcoin fell below $70,000, saying the drop sharply lowered the value of Strategy’s huge crypto holdings.

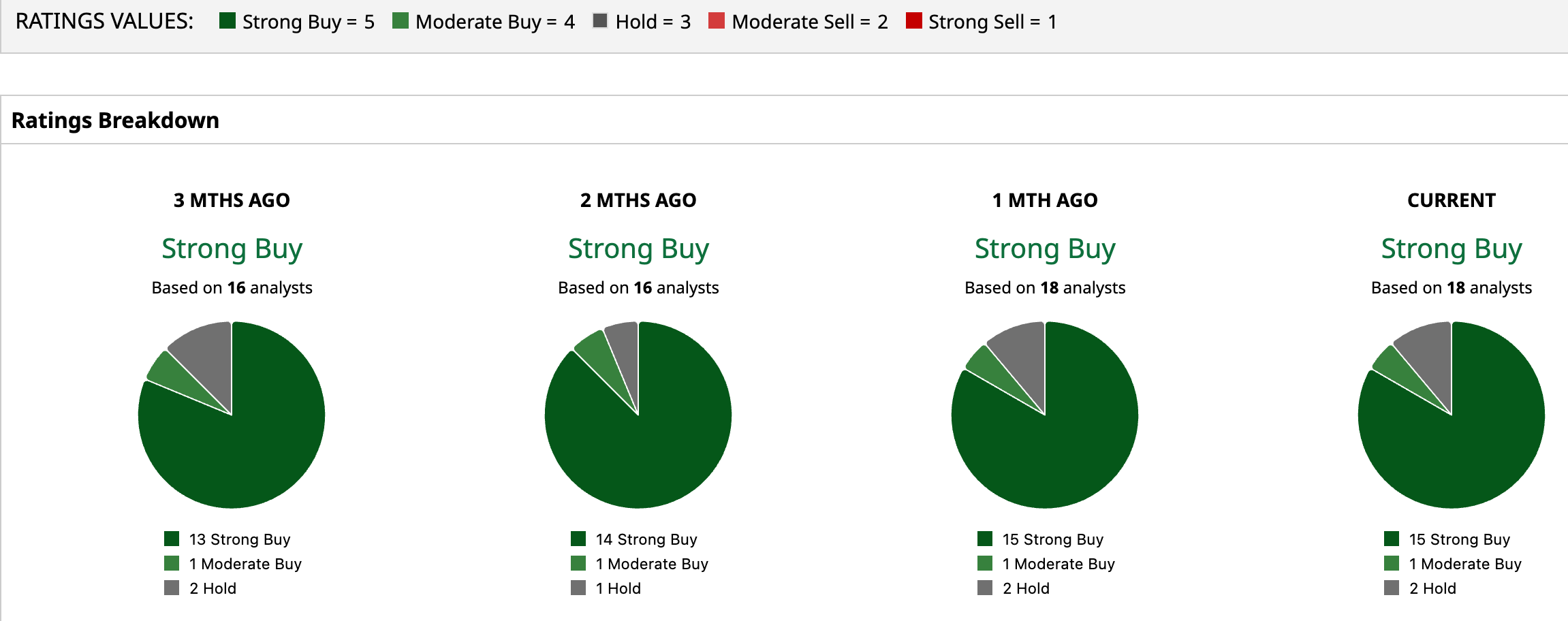

All 18 analysts surveyed rate Strategy a consensus “Strong Buy”, and the average target price of $360.81 suggests a 94% upside from current levels.

Conclusion

Strategy’s Q1 story says if you buy the stock today, you are really signing up for a leveraged call option on Bitcoin with a growing preferred-equity income layer riding shotgun. The earnings optics will keep whipsawing as long as unrealized BTC gains and losses dominate the P&L, but the STRC platform, the push toward semi-monthly payouts, and the early signs of institutional adoption all tilt the narrative toward a more income-friendly version of this Bitcoin vehicle. If BTC holds its ground or grinds higher, I think the path of least resistance for the shares is still up over the next year, even if the ride remains extremely volatile.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Advanced%20Micro%20Devices%20Inc_%20logo%20on%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

/Tesla%20charging%20station%20black%20background%20by%20Blomst%20via%20Pixabay.jpg)

/Palantir%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock.jpg)