/AI%20(artificial%20intelligence)/Close-%20up%20of%20computer%20chip%20with%20AI%20sign%20by%20YAKOBCHUK%20V%20via%20Shutterstock.jpg)

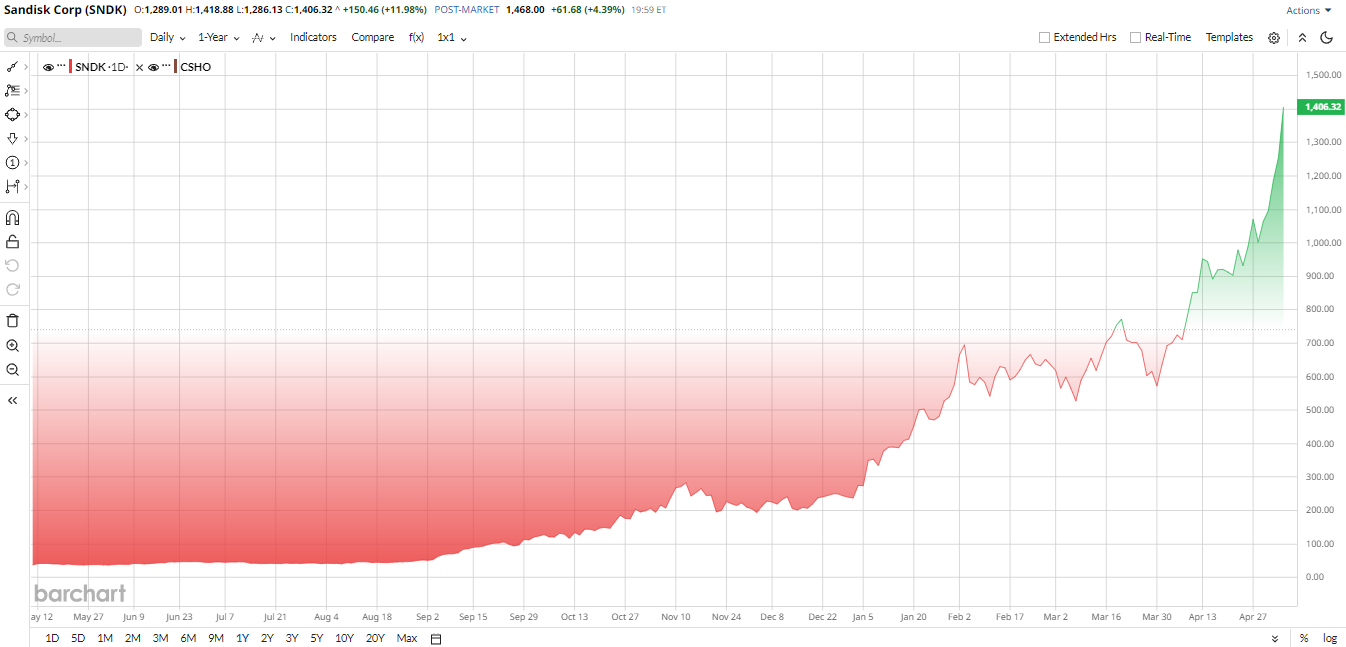

SanDisk (SNDK) has become one of the most talked about AI storage plays in 2026. Memory stocks are booming as artificial intelligence drives massive data creation. Data centers need more storage, and that demand is pushing NAND pricing higher.

Over the past few months, investors have piled into this space. Stocks have run hard. But questions remain. Is this cycle sustainable or just another peak?

That is why Susquehanna’s new call on SNDK stock is grabbing so much attention. The firm raised its price target to $2,000 after the latest earnings report. That is the highest target on Wall Street right now, and it says a lot about how bullish some analysts still are on this rally.

SanDisk's Massive Run Is Turning Heads

SanDisk is not just the old flash drive brand anymore. It is now a pure-play NAND storage story. That matters because the company sits right in the middle of the AI storage rush. More AI means more data. More data means more demand for fast, durable storage. That is the business that investors are buying now.

SanDisk is reshaping its business model as well. It has signed five long-term customer agreements worth more than $42 billion in future revenue. The company also recently approved a $6 billion share buyback, extended its Kioxia joint venture through 2034, and invested $1 billion in Nanya Technology.

SNDK stock has already run far. Shares are up 464% in 2026 and have surged more than 2,700% since the spinoff from Western Digital (WDC). Even after that move, the stock still jumped again after the latest earnings report. However, some analysts are worried that the memory business still needs a lot of capex across the industry, and that can change the mood fast.

Valuation is the tricky part. The market has already paid up for growth. Barchart data puts the forward price-to-earnings (P/E) ratio at around 27.8 times, which is relatively reasonable versus the sector median. Yet the price-to-sales (P/S) ratio is still rich. This is not a bargain-bin stock, but a growth stock priced for a very strong memory cycle.

Susquehanna Hikes SanDisk Price Target to $2,000

Just a few days ago, Susquehanna doubled its target on SNDK stock to $2,000 from $1,000 and kept a “Positive” rating after the earnings report. The argument was simple. Revenue visibility is better now, and the company has more long-term customer deals. That makes the story look less like a pure boom-and-bust trade.

Investors liked that idea, even if the stock pulled back a bit following the print. The message was still clear. If AI storage demand stays tight, SanDisk has room to run.

SanDisk Beats Q3 Earnings Estimates

The latest quarter backed up the optimism. SanDisk reported fiscal third-quarter revenue of $5.95 billion, up 251% from a year ago and well above estimates. Data-center revenue jumped 645% year-over-year (YOY) to $1.47 billion, while edge revenue climbed 295% YOY to $3.66 billion. Consumer revenue rose as well, though it remains the smallest segment.

Net income came in at $3.61 billion, a huge swing from a loss of $1.93 billion a year earlier. Not just that, free cash flow reached a record $2.99 billion, and cash and cash equivalents stood at $3.73 billion. CEO David Goeckeler called it a fundamental inflection point, and that assessment looks justified as the company shifts toward higher-value markets.

Guidance kept the bull case alive. For the current quarter, SanDisk expects revenue between $7.75 billion and $8.25 billion as well as adjusted EPS between $30 and $33. Wall Street is looking for $6.49 billion in revenue and about $22.70 in EPS, so the company is still running ahead of expectations.

On a full-year basis, analysts forecast EPS of $63.93 in fiscal 2026, followed by EPS of $182.57 in fiscal 2027. That sharp growth trajectory helps explain why SNDK stock continues to command investor confidence.

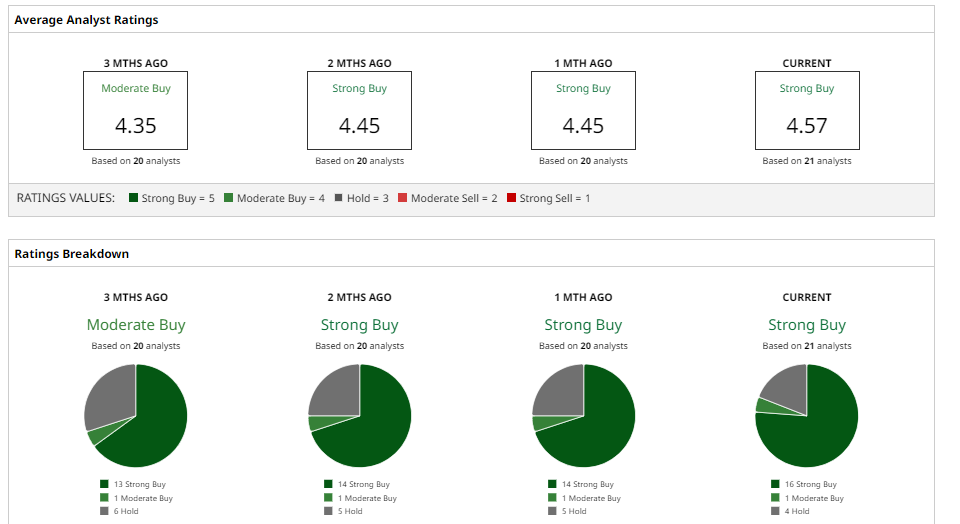

What Do Analysts Say About SanDisk Stock?

Susquehanna is the most bullish among analysts with a $2,000 price target on SanDisk. Meanwhile, Evercore initiated coverage on the stock with a $1,200 target and outlined a bull case of $2,600 per share. Citigroup also recently raised its target to $1,300 from $980, while Bank of America moved its target to $1,550. Finally, Jefferies lifted its target to $1,400 and described the latest quarter as very strong.

The consensus view remains firmly bullish. SNDK stock carries a consensus “Strong Buy” rating with a mean price target of $1,311.28 (which has already been surpassed) and a high target of $2,000 implying roughly 49% potential upside from current levels. That’s why, even after a massive run, the stock still appears to have fuel left in the tank.

The bigger question is not whether Wall Street likes SanDisk. It does. Instead, the question is whether this memory boom can stay hot long enough to justify such big targets.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)