/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

The nature of the stock market is such that it is never short on investing opportunities, no matter how overvalued analysts believe the broader market is. Palantir (PLTR) stock is the perfect example of this. A stock that was the darling of Wall Street throughout 2024 and 2025 now finds its value almost cut in half in less than a year. Yet nothing has changed in the company fundamentally. The company continues to be the most operationally embedded enterprise AI software player in the market today.

The above was also recently pointed out by Wolfe Research, which initiated coverage on PLTR stock with a “Peer Perform” rating. As has always been the case with Palantir’s bull thesis, Wolfe Research’s focus was also on its Ontology, a proprietary database layer that harmonizes the dependencies of a customer’s actual business workflows, allowing AI models to be integrated into the business context. This contextual layer is Palantir's moat, and the company’s growth metrics have so far justified this unique positioning.

This moat was never in doubt, though. It was always the valuation. The stock was priced for perfection over the course of the next few years, which was a turn-off for many investors. That is no longer true. While the valuation is still high, it is slowly entering into a territory where it is fully justified in the presence of a unique moat.

Simply viewing the forward P/E and P/S ratios, the company looks extremely overvalued. The forward GAAP P/E is 98.98x, nearly triple the sector median of 33.33x. The forward P/S ratio is even higher, sitting at 41.40x, more than 12 times the sector median of 3.34x and 18% above the company’s own 5-year average. However, other metrics offer some justification for this valuation. The consensus EPS growth estimate is 96% in 2026, 41-45% in 2027-28, and accelerating to 66% in 2029, signaling massive growth expectations in the coming years. The capital structure further strengthens the tech firm’s case, carrying a mere $211 million in total debt against $8 billion in cash.

The stock is still far from cheap, but bullish investors can argue that the premium is still worth it due to the exceptional earnings trajectory and healthy capital. The fact that PLTR stock has nearly halved from its all-time highs is just icing on the cake.

About Palantir Stock

Palantir Technologies is a software company that develops AI and data analytics platforms for government agencies and commercial clients. Its product portfolio includes Gotham, Foundry, Apollo, and Artificial Intelligence Platform (AIP). Founded in 2003, Palantir recently changed its headquarters to Miami, Florida. The firm is led by co-founder and CEO Alex Karp.

Over the last 12 months, PLTR stock has fallen nearly 25%, notably underperforming the S&P 500 ($SPX), which gained 21% during the same period. Despite a significant 85% revenue increase year-on-year (YoY) in the first quarter of 2026, the decline comes after the 138% rise in stock value in 2025 forced investors to question if the premium could be sustained. PLTR stock is down 47% from its all-time highs hit last year and is currently trading right around its 52-week low.

Palantir Beats Earnings Estimates Again

Palantir reported its first-quarter fiscal 2026 earnings on May 4. The firm beat analyst consensus on both key metrics. Revenue was reported at $1.63 billion, representing a significant 85% growth YoY and above the $1.54 billion consensus. The EPS was $0.33 compared to the expected $0.28. The Chief Revenue Officer referred to the quarter as the most exciting in the firm’s history, as US revenue grew 104% YoY. The rule of 40 score increased to 145%, something that, according to the CEO, had only been achieved by AI companies Nvidia (NVDA), Micron (MU), and SK Hynix. Additionally, the firm’s net income more than quadrupled, going from $214 million to $870.5 million. The CEO stated that the results demonstrate a level of strength that surpassed every software company in history at this scale.

For the next quarter, the firm expects revenue of approximately $1.8 billion compared to the $1.68 billion consensus. The strong financials have also increased Palantir’s full-year revenue guidance to $7.65 to $7.66 billion, a 71% growth and above the $7.27 billion consensus. Despite the 104% growth in US revenue, the CEO stated that Palantir’s greatest challenge is the supply constraints in the U.S. He believes that the company’s growth, while extremely promising, is still being restricted due to not being able to cope with the high demand.

What Are Analysts Saying About PLTR Stock?

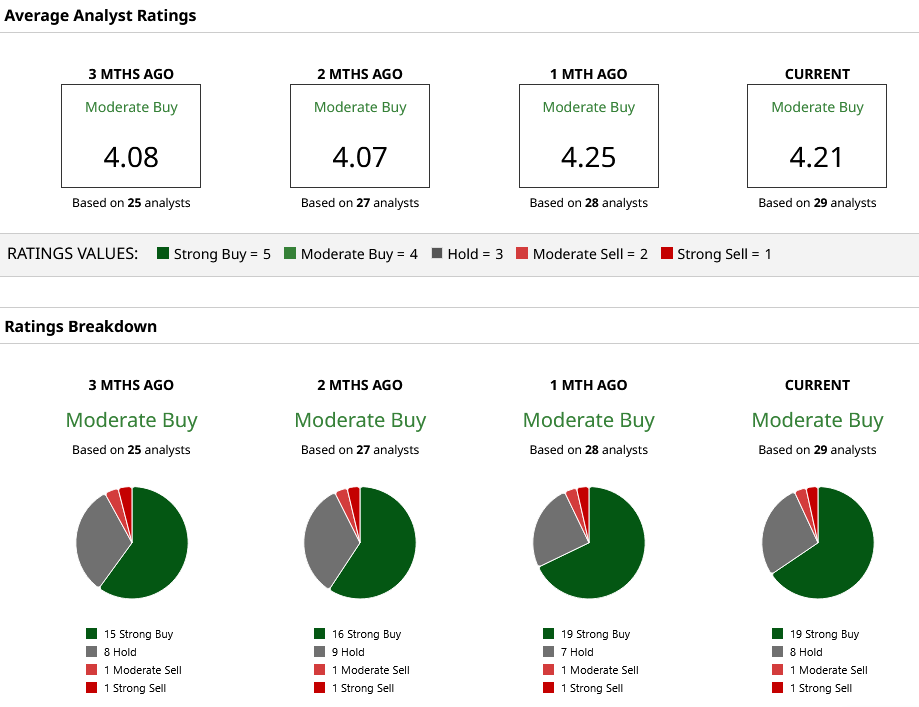

Wolfe research analyst Alex Zukin recently upgraded his PLTR price rating from “Underperform” to “Peer Perform.” The analyst believes that Palantir’s AI Platform, Ontology, and forward-deployed engineering model have proven that the company can convert AI interest into large-scale enterprise adoption. Zukin stated that Palantir is not too big to fail but is now too big to be ignored. Meanwhile, analysts from UBS and Bank of America Securities both maintained a higher “Buy” rating with price targets of $200 and $255, respectively.

Based on the 29 Wall Street analysts, PLTR stock holds a “Moderate Buy” rating, with the majority of analysts suggesting a “Strong Buy.” The mean price target is $193.63, indicating a healthy 76% upside. The analyst price targets go as high as $255 and as low as $90, which signals differing opinions on a company that has a strong balance sheet but also drastically higher P/E and P/S ratios than its peers.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Delta%20Air%20Lines%2C%20Inc_%20passanger%20plane-by%20viper-zero%20via%20iStock.jpg)