/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

Sandisk’s (SNDK) rally is showing no signs of slowing. While SNDK stock has gained over 488.6% year-to-date (YTD), robust demand for high-performance storage solutions driven by artificial intelligence (AI) workloads, along with its solid product portfolio, support its bull case. Moreover, a higher-value customer mix and improved pricing continue to support SNDK’s upward trajectory. Adding to the positives is the company’s transition toward what it terms new business models (NBMs).

NBMs are multiyear supply partnerships. By locking in longer-term customer agreements, SanDisk is reducing earnings volatility while enhancing visibility into future cash flows. This structural shift suggests a move toward more durable margins and higher earnings, which should support SNDK stock.

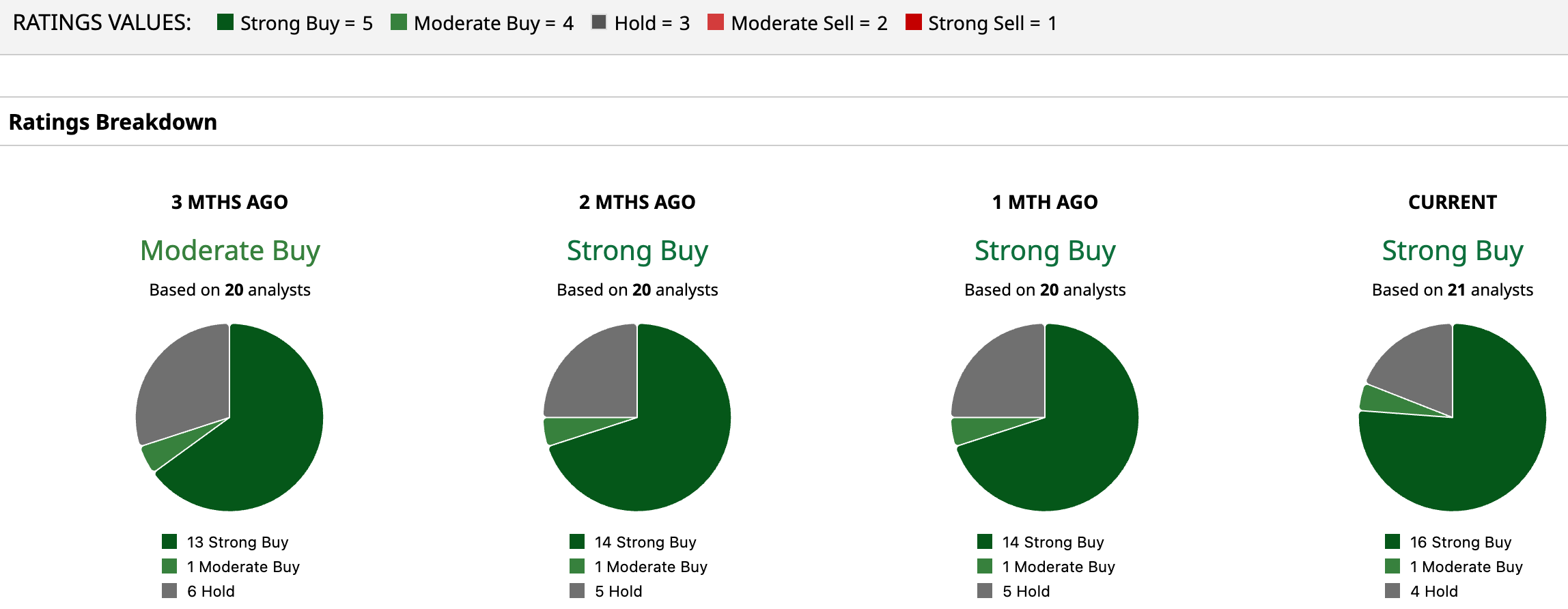

Solid demand, favorable pricing, and several newly signed multi-year supply deals have boosted confidence in Sandisk stock. As a result, at least one Wall Street analyst believes the SNDK could reach $2,000 - the highest price target on the Street—over the next 12 months. That would represent a potential gain of more than 59% from its May 4 closing price of 1,255.86.

Inside Sandisk’s Push Toward Predictable Growth

Sandisk’s NBMs represent a structural shift to better manage demand and pricing volatility. The multi-year contractual agreements provide visibility over future growth, add stability to its top line, help expand margins, and are likely to generate higher earnings.

By securing long-term agreements, five signed within a relatively short window, Sandisk has improved its revenue profile. These contracts vary in duration, with some extending up to five years, and are structured to scale over time as customer commitments increase. This built-in growth trajectory enhances capacity planning and reduces the risk of underutilization, a persistent issue in the memory industry during downturns.

Moreover, by incorporating both fixed and variable pricing elements, Sandisk achieves a balanced risk-sharing mechanism with its customers. The variable component allows the company to participate in upside scenarios when memory prices rise and provides protection when prices decline.

Further, the large scale of these agreements shows their strategic importance. The three contracts signed in the third quarter represent a minimum revenue commitment of $42 billion. Moreover, these commitments are secured through financial guarantees.

Sandisk’s management stated that these NBMs are expected to account for more than one-third of Sandisk’s bit shipments by fiscal 2027. Moreover, management signaled further expansion as additional deals are finalized.

Overall, NBMs offer greater earnings visibility and reduce volatility, which augurs well for growth.

Will SNDK Stock Hit $2,000?

Sandisk delivered exceptional growth in Q3. Revenue reached $5.95 billion, nearly doubling from the previous quarter and rising 251% compared to the same period last year. This surge was driven by a shift toward higher-value customers and stronger pricing conditions.

Growth was strong in the Data Center segment, where revenue more than tripled to about $1.5 billion. The Edge business also expanded rapidly, climbing 118% to $3.2 billion.

Thanks to the strong revenue, SNDK’s profitability improved significantly. Adjusted gross margins rose to 78.4%, a sharp increase from 51.1% in the prior quarter, supported by a favorable product mix and pricing. Earnings followed suit, with adjusted EPS jumping to $23.41 from $6.20.

Looking ahead, this strong momentum in Sandisk’s business will continue. For the fourth quarter, SNDK’s revenue is projected to land between $7.75 billion and $8.25 billion, with both sequential and year-over-year (YOY) growth remaining strong. Higher pricing and increased shipment volumes are expected to drive this expansion, while margins are forecasted to improve further. Earnings are also set to rise meaningfully, with adjusted EPS estimated at $30 to $33.

While Sandisk is set to deliver significant growth, the stock still appears reasonably priced given its growth outlook. Its forward price-to-earnings ratio of 25.02 times is compelling considering the pace of earnings expansion. Analysts anticipate SNDK’s EPS to jump 164.87% in fiscal 2027 after registering massive growth in 2026.

Overall, solid demand and pricing, shift toward NBMs, solid earnings growth, and compelling valuation suggest there’s more upside in SNDK stock, and it could hit $2,000. Analysts are bullish and maintain a “Strong Buy” stance.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.