/AI%20(artificial%20intelligence)/AI%20Infrastructure%20by%20FOTOGRIN%20via%20Shutterstock.jpg)

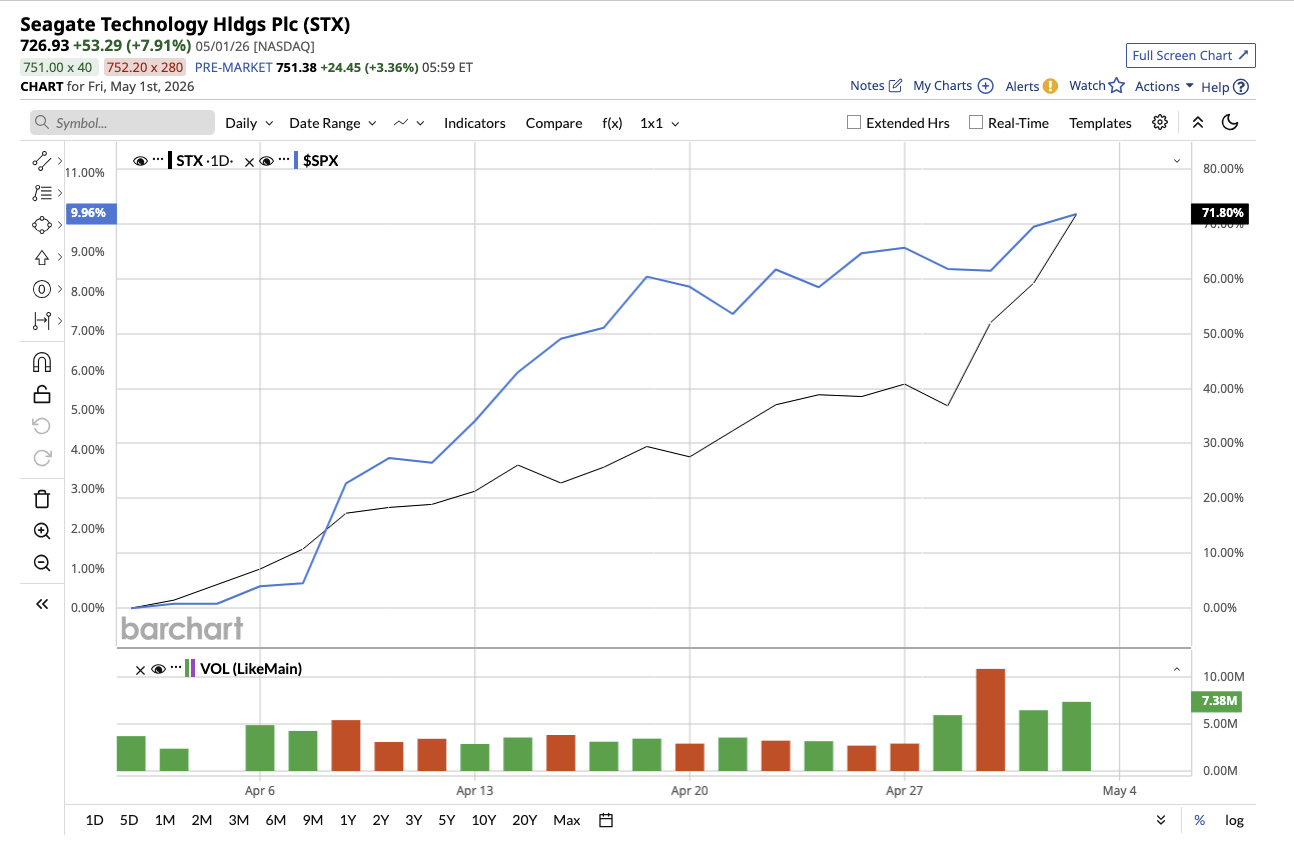

Seagate Technology (STX), a global leader in data storage solutions and hard disk drives, has emerged as one of the more unexpected winners of the AI-driven market rally in 2026. Besides some obvious hottest winners last month, Seagate closed April with 59% gain and is up 168.2% year-to-date (YTD). This spike was fueled by strong earnings and a rapidly strengthening outlook.

Seagate’s performance hasn’t gone unnoticed on Wall Street, with price estimates reaching as high as $1000, implying a 35.4% upside from current levels.

Let’s dig in to find out what has made Wall Street so optimistic about Seagate.

Reason #1: A Growth Engine Reignites

Valued at $163 billion, Seagate designs and manufactures data storage solutions, primarily hard disk drives (HDDs), used by data centers, cloud providers, businesses, and consumers. Seagate reported a tremendous third quarter of fiscal 2026 on April 29. Revenue surged 44% year-over-year (YOY) to $3.1 billion, topping guidance and consensus estimates. Data center dominance is strengthening due to continued strength from both cloud and enterprise customers. In the March quarter, Seagate shipped 199 exabytes, up 39% YOY, highlighting the scale at which data storage demand is rising. The data center business alone generated 80% of revenue, growing 55% YOY to $2.5 billion. This kind of growth signals cycle recovery along with structural demand hitting, which is why the stock is getting attention.

Reason #2: Profitability Hits Another Gear

What has truly strengthened the bull case is Seagate’s ability to convert growth into profitability at an alarming pace. Adjusted earnings per share (EPS) surged a whopping 115.7% to $4.10. Gross margin came in at 47%, with operating margin expanding to 37.5%. The company generated $953 million in free cash flow, marking one of the highest levels in over a decade. This financial strength has enabled Seagate to aggressively strengthen its balance sheet, reducing debt by $641 million in the quarter and about $1.1 billion YTD. Additionally, the company also returned $191 million to shareholders through dividends and buybacks. One of the most convincing signals for long-term investors in a growth stock is when profitability grows faster than revenue.

Reason #3: AI Demand Meets Long-Term Visibility

AI needs vast amount of data that must be stored, accessed, and retained for years. Management has specifically stressed that this demand is not only cyclical, but also long-term. Notably, the company has almost completely committed nearline storage capacity through calendar 2027, and build-to-order agreements have locked in pricing and demand with major cloud and hyperscale customers.

Additionally, Seagate’s HAMR-based Mozaic platform is enabling significant capacity gains, with drives scaling to 44 terabytes and targeting 50 terabytes by 2027, while improving cost and energy efficiency per terabyte. This technology may prove to be the company’s moat.

All in all, structural AI demand, multi-year cloud contracts, and breakthrough storage technology are positioning Seagate for a sustained period of growth. Analysts’ earnings estimates for the next two years reflects this sustained demand. Earnings are expected to increase by 94.2% in fiscal 2026, followed by 81% in fiscal 2027.

What’s the Word on the Street for Seagate Stock?

Seagate’s rally is not being driven by hype but by faster growth, expanding profitability, and long-term demand visibility. The company is now operating in an industry where data has become a critical asset, and storage is a core part of the AI value chain. This is why Wall Street is paying attention.

Following the Q1 report, Bernstein made the most drastic price target upgrade, increasing it from $620 to $1000, which is also Seagate’s high price estimate on the Street. Similarly, Barclays, JP Morgan and Mizuho Securities, among others have boosted their price targets for the stock.

Morgan Stanley boosted the price target to $767 from $582 while retaining an “Overweight” rating. The firm referred to Seagate as a “top pick” among analysts, highlighting its growing importance in the evolving AI-driven data ecosystem.

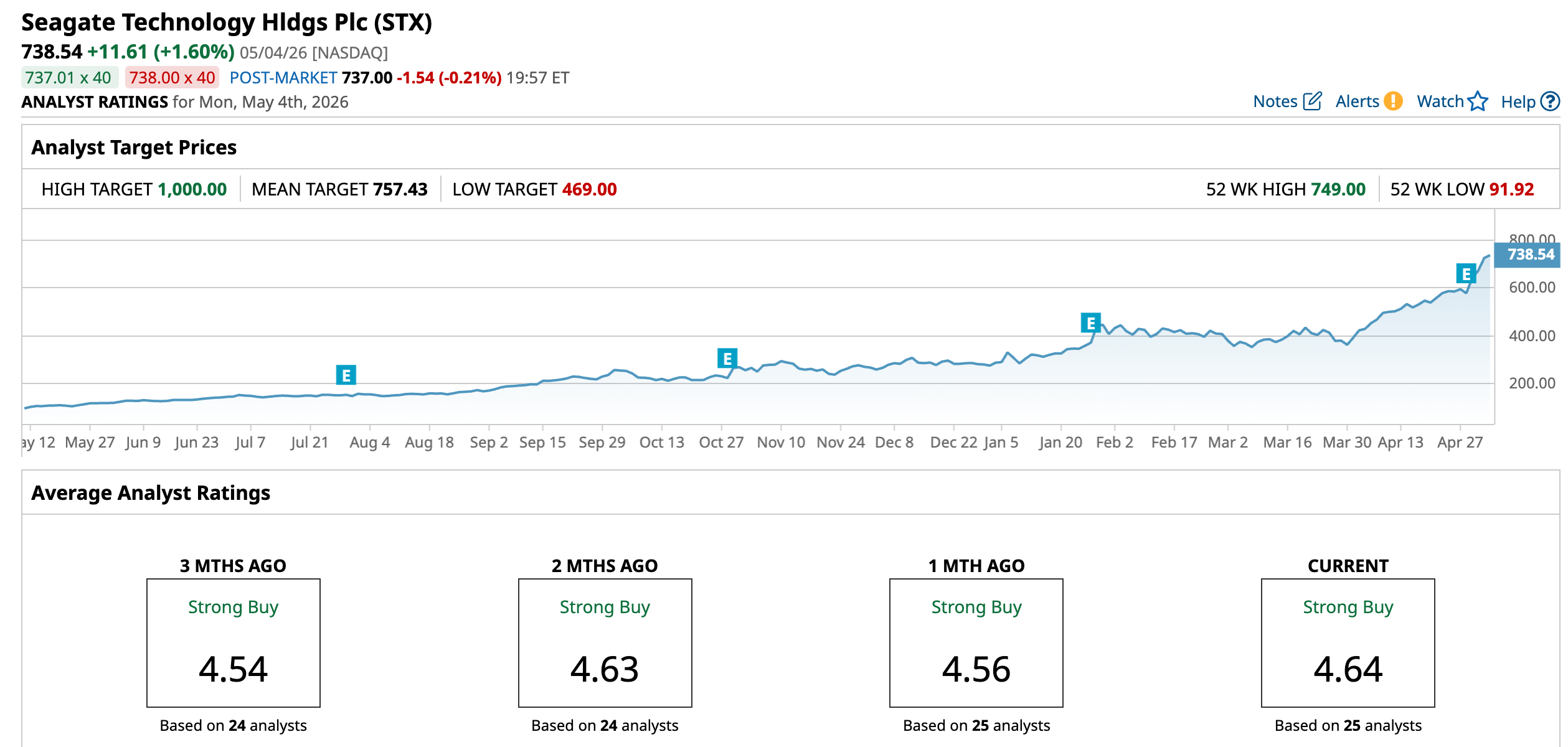

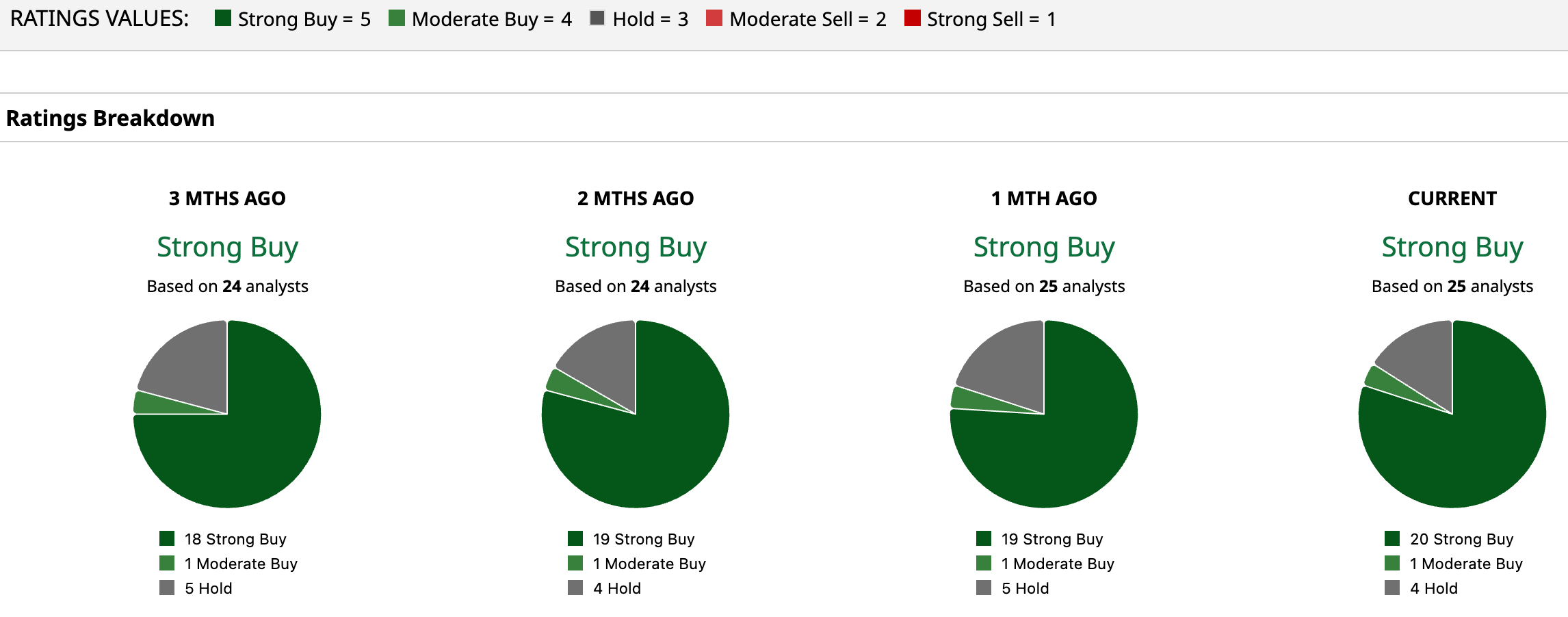

Overall, the consensus on Seagate stock is a “Strong Buy” from 20 out of 25 analysts covering the stock. Meanwhile, one rates it a “Moderate Buy,” while four say it is a “Hold.” The average target price for the stock is $757.43 which is 2.6% above current levels.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Western%20Digital%20Corp_%20logo%20on%20sign-by%20360b%20via%20Shutterstock.jpg)

/PayPal%20Holdings%20Inc%20sign%20on%20building-%20by%20Sundry%20Photography%20via%20Shutterstock.jpg)

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)