/JPMorgan%20Chase%20%26%20Co_%20operations%20center-by%20jetcityimages%20via%20iStock.jpg)

New York-based JPMorgan Chase & Co. (JPM) is the largest bank in the United States and one of the most systemically important financial institutions globally. Valued at $817.5 billion by market cap, it operates as a universal bank, combining consumer banking, corporate lending, investment banking, and asset management under one platform.

Shares of this investment banking leader have underperformed the broader market over the past year. JPM has gained 26.4% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 28.3%. In 2026, JPM’s stock fell 4%, compared to the SPX’s 4.2% rise on a YTD basis.

Narrowing the focus, JPM has outpaced the State Street SPDR S&P Bank ETF (KBE). The exchange-traded fund has gained about 24.7% over the past year.

On Apr. 14, JP Morgan released its FY2026 1Q earnings and its shares dipped 1.7% in the next trading session. Its reported revenue rose 10% year over year to $49.84 billion, and EPS surged 17.2% year over year to $5.94. Growth was supported by record market revenue and strong dealmaking, alongside higher net interest income from solid loan demand. Investment banking fees and trading volumes surged amid market volatility, while consumer spending and credit quality remained resilient.

For the current fiscal year, ending in December, analysts expect JPM’s EPS to grow 10.2% to $22.42 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

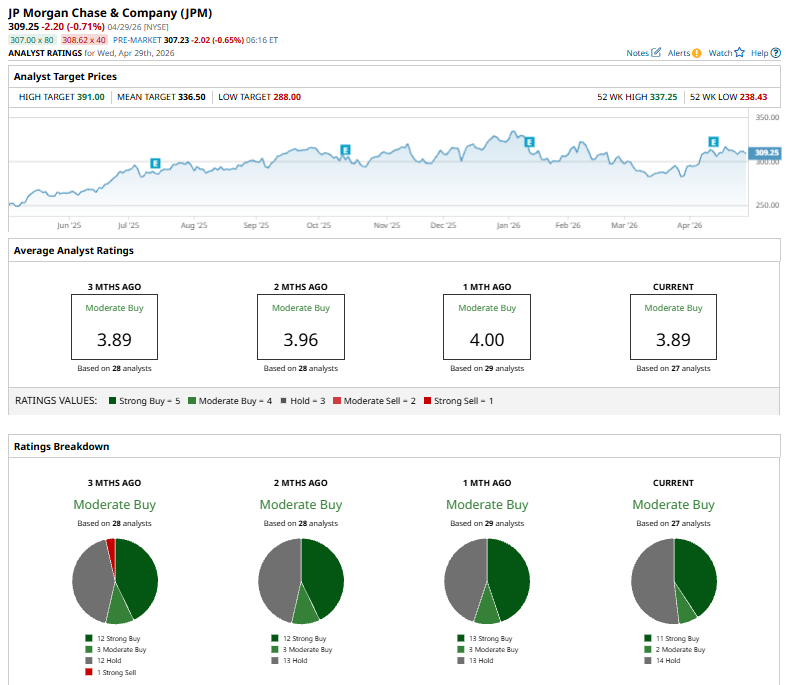

Among the 27 analysts covering JPM stock, the consensus is a “Moderate Buy.” That’s based on 11 “Strong Buy” ratings, two “Moderate Buys,” and 14 “Holds.”

This configuration is bearish than a month ago, with 13 analysts suggesting a “Strong Buy.”

On Apr. 20, Evercore ISI raised its price target on JPMorgan Chase to $340 from $320 while maintaining an “Outperform” rating, citing a standout quarter driven primarily by exceptionally strong trading performance.

The mean price target of $336.50 represents an 8.8% premium to JPM’s current price levels. The Street-high price target of $391 suggests an upside potential of 26.4%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)