Chicago, Illinois-based Mondelez International, Inc (MDLZ) is a leading global snacking powerhouse that operates in more than 150 countries. Valued at $78.2 billion by market cap, the company offers a wide range of products such as biscuits, baked snacks, chocolates, gums, candies, cheese, and powdered beverages under brands like Oreo, Ritz, LU, CLIF Bar, Tate’s Bake Shop, Cadbury Dairy Milk, Milka, and Toblerone.

Shares of this snack powerhouse have underperformed the broader market over the past year. MDLZ has fallen 7% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 28.3%. However, in 2026, MDLZ stock is up 13.4%, surpassing the SPX’s 4.2% YTD gain.

Narrowing the focus, MDLZ has trailed the First Trust Nasdaq Food & Beverage ETF (FTXG), which has declined 3.3% over the past year.

On Apr. 28, Mondelez released its FY2026 Q1 earnings, and its shares popped 4.3% in the next trading session. Its revenue rose 8.2% year over year to $10.08 billion, supported by solid performance in Europe and emerging markets, especially India. However, its adjusted EPS dipped 14.9% to $0.67 due to higher input costs. Mondelez reaffirmed its 2026 outlook, expecting organic revenue growth of flat to 2% and adjusted EPS growth of flat to 5% on a constant currency basis, along with free cash flow of around $3 billion. Currency tailwinds are projected to provide a modest boost, adding roughly 2% to revenue growth and about $0.06 to EPS.

For the current fiscal year, ending in December 2026, analysts expect MDLZ’s EPS to improve 3.8% to $3.03 on a diluted basis. The company’s earnings surprise history is stellar. It beat the consensus estimate in each of the last four quarters.

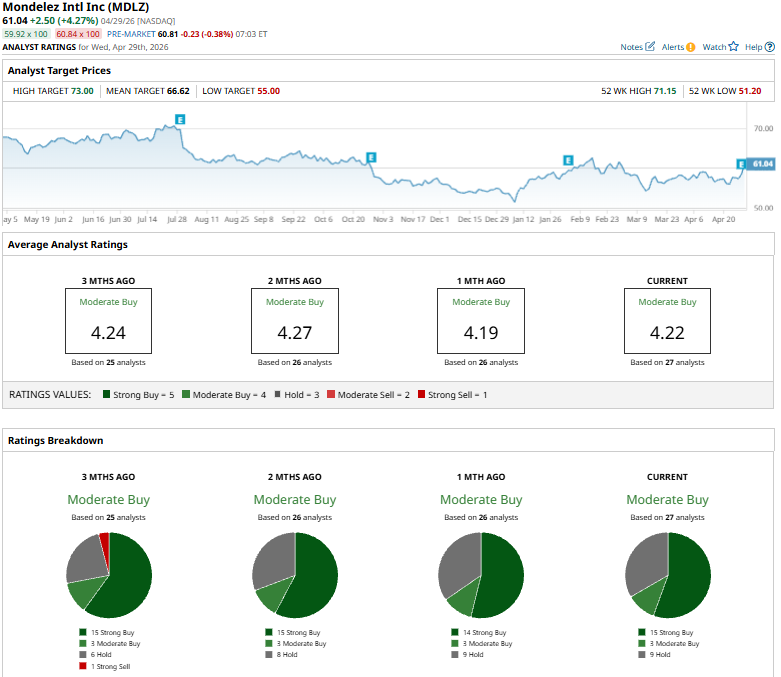

Among the 27 analysts covering MDLZ stock, the consensus is a “Moderate Buy.” That’s based on 15 “Strong Buy” ratings, three “Moderate Buys,” and nine “Holds.”

The configuration is bullish than a month ago when it had 14 “Strong Buy” suggestions.

On Apr. 29, Thomas Palmer of JPMorgan Chase maintained an “Overweight” rating on Mondelez International and raised the price target to $70 from $67.

The mean price target of $66.62 represents a 9.1% premium to MDLZ’s current price levels. The Street-high price target of $73 suggests a notable upside potential of 19.6%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)