/amazon%20holiday%20delivery%20boxes%20by%20Cineberg%20via%20iStock.jpg)

Amazon (AMZN) stock has regained momentum ahead of the first-quarter 2026 earnings scheduled for Wednesday, April 29. Shares of this e-commerce and cloud leader recently hit an all-time high of $265.50 and have risen 27.4% in the past month.

A key catalyst pushing Amazon's stock higher is its deepening push into artificial intelligence (AI). Amazon recently expanded its partnership with Anthropic. Per the agreement, Anthropic plans to invest more than $100 billion over the next decade into Amazon Web Services (AWS), securing massive computing capacity to train and operate its Claude AI models. This long-term demand not only reinforces AWS’s central role in the AI ecosystem but also provides Amazon with a highly visible growth runway.

At the same time, Amazon’s in-house chip business is turning into a significant growth engine. The company recently revealed that its custom silicon portfolio, including Graviton processors, Trainium AI chips, and Nitro networking components, has achieved an annual revenue run rate exceeding $20 billion. The chip business is growing at a solid pace, posting triple-digit year-over-year (YoY) growth. Moreover, it has doubled from the $10 billion run rate AMZN disclosed during the Q4 conference call.

All these factors provide a favorable setup for Amazon ahead of Q1 earnings.

Revenue Strength Likely to Continue Across Core Segments

Amazon is likely to deliver a solid first quarter on the revenue front, supported by sustained momentum across its core operating segments, including e-commerce, cloud computing, and digital advertising. Management has guided for Q1 net sales in the range of $173.5 billion to $178.5 billion, implying YoY growth of approximately 11% to 15% from $155.7 billion in the same period last year.

The retail segment continues to deliver steady growth. Amazon’s emphasis on competitive pricing, extensive product selection, and faster delivery continues to drive the segment’s top line. Structural improvements in logistics, particularly through its regionalized fulfillment network in the U.S., are enhancing delivery speed while lowering transportation costs. These operational efficiencies support revenue growth and help stabilize margins.

Cloud computing, led by AWS, is experiencing rapid growth. AWS reported $35.6 billion in Q4 revenue, with growth accelerating to 24% YoY. The segment’s annualized revenue run rate is $142 billion. The segment is benefitting from ongoing strength in the core cloud services and increasing adoption of AI-related solutions, as enterprises continue to modernize infrastructure and migrate workloads. AWS’s backlog stood at $244 billion at the end of Q4, up 40% YoY, indicating strong forward demand visibility and a healthy deal pipeline.

Amazon’s advertising business is another key growth driver. The segment generated $21.3 billion in Q4 revenue, growing 22% YoY. This high-margin business benefits from strong demand for sponsored product placements within Amazon’s marketplace, as well as increasing monetization of its streaming and digital content platforms.

Margins Under Pressure as Investment Cycle Intensifies

Despite the strength in the top line, Amazon’s earnings growth could slow. Higher capital expenditures, driven by investments in AI infrastructure, will likely hurt its bottom-line growth. However, the company’s focus on cost optimization, including improvements in fulfillment efficiency and automation via robotics, should partially offset these pressures.

Analysts expect AMZN to report Q1 earnings of $1.61 per share, up 1.3% YoY. This reflects a slowdown in its EPS growth rate. AMZN’s EPS increased by 5% YoY in Q4.

What’s Ahead for AMZN Stock?

Amazon is firing on multiple cylinders. Its diversified revenue streams, leadership in cloud computing, and expanding footprint in AI provide a compelling long-term growth story. However, the recent stock surge also raises the bar for execution.

Amazon’s Q1 will reflect strong revenue momentum. However, profitability may face short-term headwinds due to heavy investment. Nonetheless, AMZN’s operational discipline and focus on lowering costs will likely provide some cushion.

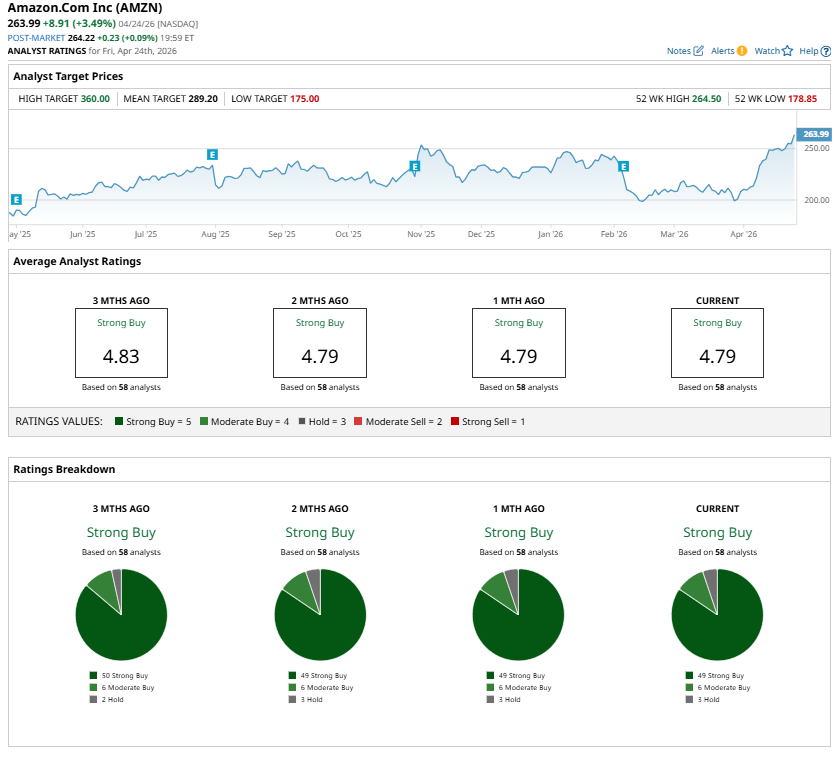

Overall, Amazon is a solid long-term bet, and Wall Street recommends a “Strong Buy.” However, any softness in cloud growth or sharper-than-expected margin compression may trigger short-term volatility in AMZN stock.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)